Authord by Lance Roberts via RealInvestmentAdvice.com,

Yes, Virgina, There Is A Santa Claus

Every year, at this time, I republish the story of 8-year Virginia O’Hanlon who asked the most important of questions. I encourage you to read it as it reminds us of the importance, meaning and the “Spirit” of the Christmas season.

* * *

Eight-year-old Virginia O’Hanlon wrote a letter to the editor of New York’s Sun, and the quick response was printed as an unsigned editorial Sept. 21, 1897. The work of veteran newsman Francis Pharcellus Church has since become history’s most reprinted newspaper editorial, appearing in part or whole in dozens of languages in books, movies, and other editorials, and on posters and stamps

THE EDITORIAL

DEAR EDITOR:

I am 8 years old.Some of my little friends say there is no Santa Claus.Papa says, ‘If you see it in THE SUN it’s so.’Please tell me the truth; is there a Santa Claus?

VIRGINIA O’HANLON.115 WEST NINETY-FIFTH STREET.

“VIRGINIA, your little friends are wrong. They have been affected by the skepticism of a skeptical age. They do not believe except they see. They think that nothing can be which is not comprehensible to their little minds. All minds, Virginia, whether they be men’s or children’s, are little. In this great universe of ours, man is a mere insect, an ant, in his intellect, as compared with the boundless world about him, as measured by the intelligence capable of grasping the whole of truth and knowledge.

Yes, VIRGINIA, there is a Santa Claus. He exists as certainly as love and generosity and devotion exist, and you know that they abound and give to your life its highest beauty and joy. Alas! how dreary would be the world if there were no Santa Claus? It would be as dreary as if there were no VIRGINIAS. There would be no childlike faith then, no poetry, no romance to make tolerable this existence. We should have no enjoyment, except in sense and sight. The eternal light with which childhood fills the world would be extinguished.

Not believe in Santa Claus! You might as well not believe in fairies! You might get your papa to hire men to watch in all the chimneys on Christmas Eve to catch Santa Claus, but even if they did not see Santa Claus coming down, what would that prove? Nobody sees Santa Claus, but that is no sign that there is no Santa Claus. The most real things in the world are those that neither children nor men can see. Did you ever see fairies dancing on the lawn? Of course not, but that’s no proof that they are not there. Nobody can conceive or imagine all the wonders there are unseen and unseeable in the world.

You may tear apart the baby’s rattle and see what makes the noise inside, but there is a veil covering the unseen world which not the strongest man, nor even the united strength of all the strongest men that ever lived, could tear apart. Only faith, fancy, poetry, love, romance, can push aside that curtain and view and picture the supernal beauty and glory beyond. Is it all real? Ah, VIRGINIA, in all this world there is nothing else real and abiding.

No Santa Claus! Thank God he lives, and he lives forever. A thousand years from now, Virginia, nay, ten times ten thousand years from now, he will continue to make glad the heart of childhood.”

Merry Christmas, and may this new year bring you joy, laughter, and prosperity.

From all of us at Real Investment Advice, Real Investment News, and Clarity Financial.

* * *

Santa Rally?

With the market now back to overbought conditions, it is now or never for the traditional “Santa Rally” between Christmas and New Year’s Day.

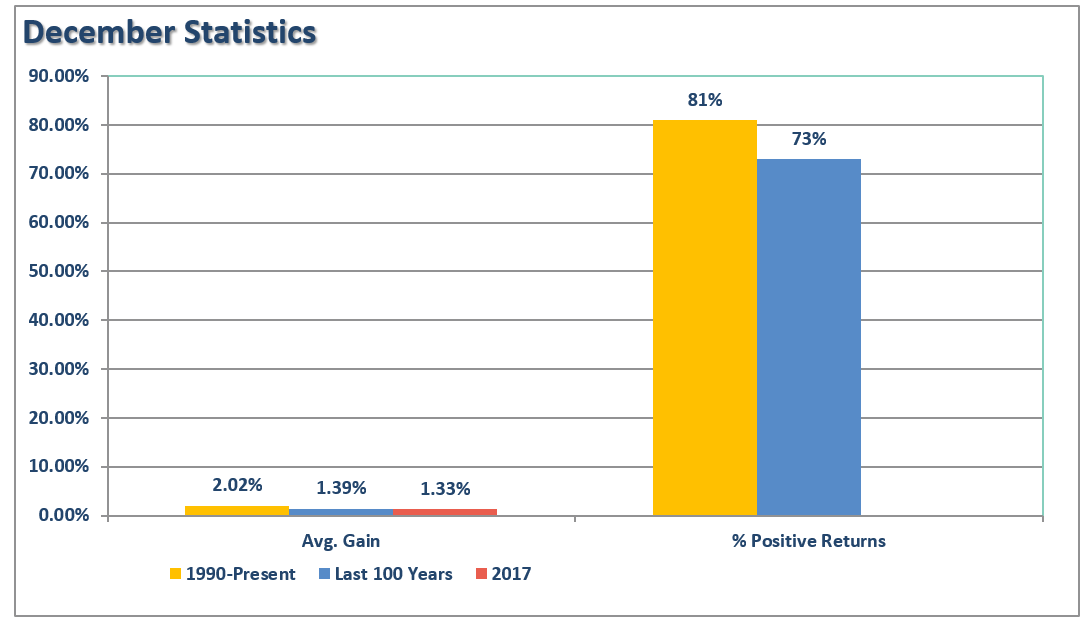

If we go back to 1990, the month of December has had average returns of 2.02% with positive returns 81% of the time. Over the past 100 years, those numbers fall slightly to a 1.39% average return with positive returns 73% of the time.

For the month of December, so far, the market has risen 1.33% which is in-line with the historical norm.

As discussed over the last couple of weeks, this is not to be unexpected as portfolio managers and hedge funds “Stuff Their Stockings” of highly visible positions to have them reflected in year-end statements.

However, come January, it is potentially a different story. As I have been laying out over the last several weeks, the “tax cut” rally may well come to an end as portfolio managers, being reluctant to sell before year-end which would put them under the 2017 tax code, will likely sell in January to lock in gains under the new tax code when they pay taxes in 2019.

While “this time” is never exactly like the “last time,” there is a reasonable precedent that a sell-off in January is a likelihood. With the outside gains this past year, and now extreme overbought conditions as discussed last week, the odds of a correction are high.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/January-SellOffs-122217.png[/image]

This next week, as close to the end of the year as possible, we will likely be adding two positions to portfolios to hedge against a potential “tax gain” related sell off. The first position will be a short-S&P 500 index combined with an intermediate-duration bond position.

Given that IF a sell-off occurs money will rotate from “risk” to “safety.” In this case, the S&P 500 should fall while bond prices rise as rates head lower. As shown below, with the stock-bond ratio at extremes, this trade is fairly low risk.

(The current stock/bond ratio is at the highest level in history. Also, note that the correlation “broke” in 2013 with QE 3. That gap will likely be filled at some point.)

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Stock-Bond-Ratio.png[/image]

If I am wrong, and the markets continue to rise, our existing long-positions, which outweigh the hedges by a large percentage, will continue to advance with the hedge only slightly inhibiting performance. If a sell-off does occur, the hedges will mitigate some of the downside risk while we evaluate our next potential moves.

We will keep you apprised of our actions next week.

Dot Com 2.0

by Michael Lebowitz, CFA

On May 20, 1999, eToys.com became a publically traded stock, offering shares to the public at a price of $20 per share. Lurching to $76 per share on the first day of trading and then over $80 a share by mid-August of that same year, investors were blindly optimistic about the prospects for this internet retailer. In early January 2001, after a weaker than expected holiday season, the company laid off half of its staff. By late February, eToys.com stock traded at meager 0.09 cents per share and filed for bankruptcy in March. The bubble had burst on eToys.com and hundreds of other tech companies selling investors on the promise of a new economic paradigm and internet fantasies.

By late 1999, when eToys.com was flourishing, the NASDAQ stock market was in the midst of a ten-year run in which it gained over 2,700%. Valuations, especially those in the tech sector but also in the broader-based markets, rose well above every prior instance. Caution and conservatism were thrown out the window in place of greed and rampant speculation. A decade of impressive market gains resulted in a high level of complacency.

We are now 18 years beyond the tech bubble, and we find ourselves in similar shoes. Most measures of equity valuation are currently higher than just about every other equity market peak including even some from 1999. The market has produced a constant stream of winners seemingly coming in waves over the last few years. Among the more popular is the FANG stocks and their valuations that assume perfection in perpetuity.

Further reminding us of the late 90’s tech bubble and the eToys.com era are Bitcoin and blockchain related stocks. Longfin Corp. (LFIN) for instance, just completed an initial public offering (IPO) at $5 per share on December 13th. On December 18th LFIN announced the purchase of Ziddu Coin a business lender dealing in crypto-currency loans. Following the announcement, the stock rose as high as $136 a share producing a 2620% gain for those investors that sold at the highs. As we pen this note, the stock trades at $41.

Instead of using “dot com,” companies like LFIN, Overstock, Riot Blockchain and other companies are seizing on investor greed by telling a grand story of Bitcoin and blockchain riches. It is, to be sure, the new-new paradigm.

Another recent example is Long Island Iced Tea Corp. which was a purveyor of bottled drinks with a stock price languishing around the $2 range. Well, that is until the company changed its name to Long “Blockchain” Corp. which sent investors into a buying frenzy running the stock price up nearly 500% in one day.

The instances where anything related to Bitcoin and blockchain is instantly deserving of massive valuations is a mirage; here today and gone tomorrow. The current era serves as a gentle reminder of the greed and wild speculation of the latest bubble. In early 2000, the markets topped with no-name (and no-profit) companies capturing the wild hopes of investors. The NASDAQ took over 16 years to re-capture the prior high water mark representing precious years that investors lost.

Whether LFIN and the like are signaling that we are in the bottom of the ninth of the latest bubble or still have a few innings to go is up for debate. What is important, however, is to retell yourself the story of the tech bubble and how investors ignored the glaring signals. Does today’s price action sound familiar? If so we recommend that you continue to remain cognizant of the patterns of prior market bubble episodes and proceed accordingly.

Rules For The Road

If you are long equities in the current market, we continue to recommend following some basic rules of portfolio management.

“It is through following these basic rules that, with the markets overbought, underlying fundamentals stretched, we continue to suggest some portfolio actions be taken to reduce, not eliminate, overall risk.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says “sell everything and go to cash.”

As I noted in last week’s missive on the current bubble, our job as investors is pretty simple – protect our investment capital from short-term destruction so we can play the long-term investment game.

In case you missed it, let me repeat for you the most important lines:

Our job as investors is actually quite simple. We must focus on:

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

With forward returns likely to be lower and more volatile than what was witnessed in the 80-90’s, the need for a more conservative approach is rising. Controlling risk, reducing emotional investment mistakes and limiting the destruction of investment capital will likely be the real formula for investment success in the decade ahead.

This brings up some very important investment guidelines that I have learned over the last 30 years.

- Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel” you should be doing.

- The ONLY investments that you can “buy and hold” are those that provide an income stream with a return of principal function.

- Market valuations (except at extremes) are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading. Knowing what type of investor you are determines the basis of your strategy.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

As an investment manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long-term capital appreciation will take of itself.