Authored by Jeffrey Snider via Alhambra Investment Partners,

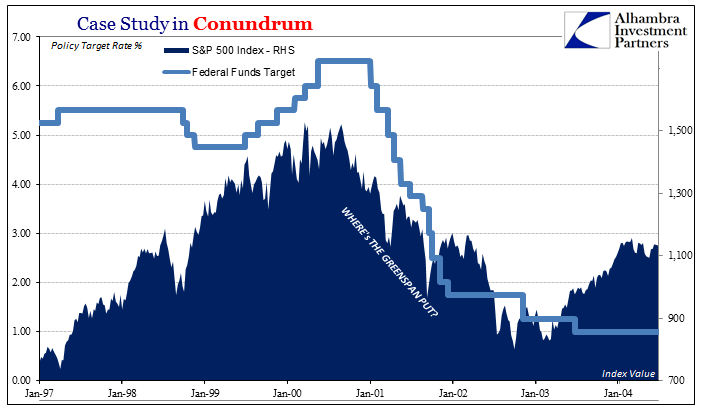

Since we are this week hypocritically obsessing over monetary policy, particularly the federal funds rate end of it, it’s as good a time as any to review the full history of 21st century “conundrum.” Janet Yellen’s Fed has run itself afoul of the bond market, just as Alan Greenspan’s Fed did in the middle 2000’s. But that latter example wasn’t truly the first conundrum for monetary policy. There remain a great many questions (in the mainstream, anyway) about the dot-coms.

If we define conundrum more broadly as I believe more appropriate, then it’s not just about UST yields long or short. It is instead the lack of (monetary) effect through federal funds rate management. In the early 2000’s this was apparent in a whole range of factors – starting with the stock market.

It had become conventional trading wisdom that, under Alan Greenspan, you don’t fight the Fed. He was the “maestro” who at his whim sat enormous monetary power. This idea of the so-called Greenspan put was born sometime in 1998 after the LTCM debacle, a fiasco that nonetheless seemed to validate the premise.

The dot-com bust, however, pushed stocks very sharply lower over an unusually lengthy period of time, taking almost three years to fully complete. During that time, the Fed was not at all idle (as you can plainly see above). In less than a year, Greenspan had reduced the federal funds target from 6.50% down all the way to 1.75%. While the rationalization for its actions was largely economic in nature, there can be no denying that under a discretionary policy regime the FOMC heavily considered the stock market.

That was supposed to be massive “stimulus” and “accommodation”, that which no stock investor should or could ignore. And yet, it clearly had no effect. The dot-com bust went on further despite what in mainstream tradition was a change to tremendously “loose” policy. Greenspan had unleashed the might of his put, and stocks tanked anyway.

But it wasn’t just the stock market that failed to be accommodated. Though the dot-com recession that began in 2001 was the mildest on record, an outcome which many were and are quick to give Greenspan credit for, the economic problem persisted instead through the first years of the recovery. In other words, the issue wasn’t its depth, but the lack of growth that followed what would otherwise have been a minor footnote in economic history.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/07/ABOOK-July-2017-Dot-Com-Conundrum-GDP.png[/image]

In terms of GDP, the recession itself was just two negative quarters spread out over the final three of 2001 (and they were non-consecutive, proving that the “technical” definition of recession isn’t one). GDP jumped to nearly 4% in the first quarter of 2002, setting up expectations for a traditional V-shaped recovery, but by the end of that year was down near zero again – as stocks kept falling.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/07/ABOOK-July-2017-Dot-Com-Conundrum-Payrolls.png[/image]

The real weakness of this first “conundrum”, however, is revealed in the labor market. It was, as had become by 2004 a campaign issue in the Presidential election that year, the second major “jobless recovery” to affect a member of the Bush family running for the White House. It’s the economy stupid somehow still resonated despite everything in the 1990’s. The final two “rate cuts” the FOMC voted (the penultimate one for 50 bps in late 2002; and the final for the last 25 bps in June 2003 to get down to a then-record low of 1%) make some orthodox sense in this context though they were executed long after the official recession end.

The Fed by that time openly worried about both stocks as well as the failure of recovery to ignite – even though by all convention “stimulus” was abundant, even enormous. The word “deflation” was used several times over the course of internal policy discussions, including the last one in June 2003, as it was brought up in the mainstream on a few occasions.

It has been Federal Reserve tradition to greatly fear a stock crash, and here was one that was as undeniable as it was lengthy. Owing to how the Crash of 1929 was viewed, stocks were given monetary importance that in this circumstance produced a puzzle. Why didn’t the Greenspan put work on stocks, while at the same time why didn’t the stock crash lead to a far greater economic calamity?

An enterprising believer in Greenspan might surmise that the federal funds “stimulus” was actually quite powerful, and that it merely counterbalanced in the real economy the building negative forces of the stock crash; a monetary standoff of sorts. The two opposing sides were largely canceled out until the natural progression of the business cycle took over. Good luck, as it was described by the economists who would later coin the phrase the Great “Moderation.”

A simpler and more consistent explanation follows the labor trail, and ends up with eurodollars.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/07/ABOOK-July-2017-Dot-Com-Conundrum-Payrolls-Manu-1.png[/image]

The primary reason for the jobless recovery was very simple – Ross Perot’s 1992 prediction had come to pass. On the surface, there was no reason whatsoever that US manufacturing would respond so harshly to what was, particularly for consumers, such a mild contraction. And yet, the level of manufacturing jobs in the US during this very crucial period, what otherwise would have been a more natural recovery, utterly collapsed. Between the peak in July 2000 and the FOMC’s last “rate cut” in June 2003, an astounding 16% of all manufacturing jobs disappeared.

And they would not stop being destroyed for years thereafter. This decimation of manufacturing would continue on until the depths of the Great “Recession”, and would be recorded by a number of economic accounts including domestic factory orders.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/07/ABOOK-July-2017-Dot-Com-Conundrum-Factory-Orders.png[/image]

Americans didn’t stop buying goods, or services for that matter, they instead stopped buying, at the margins, American goods. As would become common, throughout the period following the dot-com recession US import volumes would explode.

It was eventually and officially included in the second “conundrum” of the middle 2000’s, as well as lead to the ridiculous “global savings glut” hypothesis that “saw” these eurodollars while trying so very hard to deny their existence.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/07/ABOOK-July-2017-Dot-Com-Conundrum-China-Imports.png[/image]

In order for offshoring to occur, foreign producers needed investment in order to be able to produce. They already had the necessary (cheap) labor, what was lacking since Ross Perot was the finance and global monetary flexibility that could put it all together. The maturation of the eurodollar system in the late 1990’s, particularly after the repeal of Glass-Steagall that finally allowed depository institutions to get their balance sheets into the shadows, was the final ingredient setting the US manufacturing up for this domestic conflagration. The dot-coms were merely the spark.

And if the eurodollar system was rapidly growing through all of this, as we know that it was, that would further explain why the stock bust never created the economic catastrophe of depression. In 1929, stocks were intimately related and intertwined with money through the NYC call market and correspondence system. In 1999, that just wasn’t the case, as eurodollars were a parallel monetary system all its own, disconnected from the price or collateral nature of stocks.

Eurodollars supplied money to the real economy here and elsewhere so that the stock bust would be of limited downside in effective monetary terms, but ironically that the upside would also be limited at least in this country as it greased the wheels of US manufacturing destruction. From the perspective of various EM economies by contrast, the dot-com recovery was instead so many “miracles.” Judged instead by the whole global economy, there was no inconsistency in money that was, after all, itself global.

The Fed was largely a bystander in all of it, confused as always though at least for the first time Greenspan was openly contradicted, and by everything.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/04/ABOOK-April-2017-TIC-US-Banks-CLaims-On-Total.png[/image]

Any legitimate questions or doubts were soon forgotten, though, as the housing mania subsumed all attention – and was again attributed to monetary policy rather than the by-then exploding, parabolic eurodollar. Though Greenspan was by this time slightly tarnished by reputation, he was still held in high regard, at least until his final act produced the second conundrum disconnecting monetary policy more completely (in the opposite direction than the first) from actual and effective global money conditions.

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/01/ABOOK-Jan-2017-OCC-Derivatives-CDS-RHINO.png[/image]

[image]https://www.alhambrapartners.com/wp-content/uploads/2017/01/ABOOK-Jan-2017-OCC-Derivatives-IR-RHINO.png[/image]

The final failure of eurodollars in 2007 proved the categorical differences between money and Federal Reserve policy for good, but by then nobody much cared about the first instance(s) of Fed failure; there were, and sadly remain, bigger problems to be concerned about.

It is, however, all connected; the monetary history (including eurodollars) of the 21st century comes out very different than the monetary policy (eurodollars don’t matter) history of the same period. The latter leads to drug addicts and Baby Boomers as an eventual excuse for how QE and ZIRP performed about as well as monetary policy in 2001, 2002, and 2003. The former leads us to answers.