Via RealInvestmentAdvice.com,

According to the June 2017 snapshot from the Social Security Administration, nearly 61.5 million people were receiving a monthly benefit check, of which 68.2% were retired workers. Of these 41.9 million retirees, more than 60% count on their Social Security to be a primary source of income.

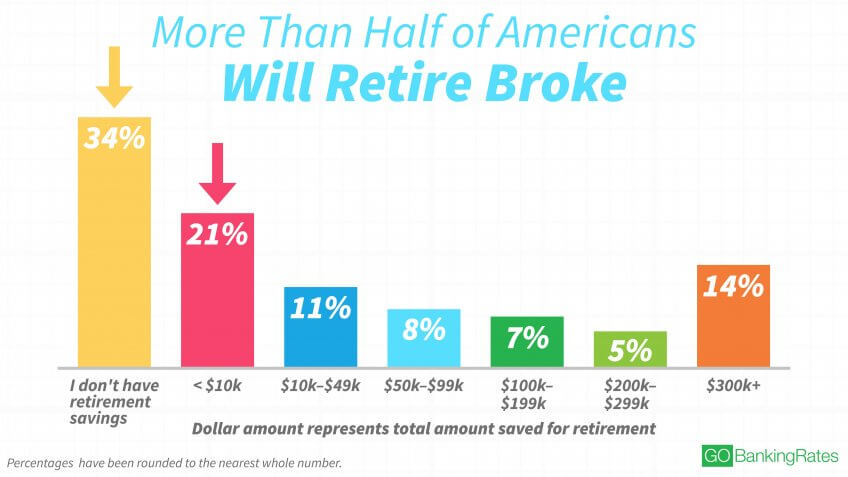

Of course, that dependency ratio is directly tied to financial insolvency of the vast majority of Americans. According to a Legg Mason Investment Survey, US baby boomers have on average $263,000 saved in defined contribution plans. But that figure is less than half of the $658,000 they say they will need to retire. As noted by GoBankingRates, more than half of Americans will retire broke.

This is a huge problem that will not only impact boomers in retirement, but also the economy and the financial markets. It also demonstrates just how important Social Security is for current and future generations of seniors.

Of course, the problem is that according to the latest Social Security Board of Trustees report issued last month, those benefits could be slashed for current and future retirees by up to 23% in 2034 should Congress fail to act. Unfortunately, given the current partisan divide in Congress, who have been at war with each other since the financial crisis, there is seemingly little ability to reach any agreement on how to put Social Security on sound footing. This puts those “baby boomers,” 78 million Americans born between 1946 and 1964 who started retiring last year, at potential risk in their retirement years.

While the Trustees report predicts that asset reserves could touch $3 trillion by 2022, implying the program is expected to remain cash flow positive through 2021, beginning in 2022, and each year thereafter through 2091, Social Security will be paying out more in benefits than it’s generating in revenue, resulting in a $12.5 trillion cash shortfall between 2034 and 2091. That is a problem that can’t be fixed without internal reforms to the pension fund due specifically to two factors: demographics and structural unemployment.

With respect to the demographic problem, it is a “one-two knock out punch” that will hit not only Social Security but also the country’s municipal and Federal pension systems. As I noted previously:

“One of the primary problems continues to be the decline in the ratio of workers per retiree as retirees are living longer (increasing the relative number of retirees), and lower birth rates (decreasing the relative number of workers.) However, this ‘support ratio’ is not only declining in the U.S. but also in much of the developed world. This is due to two demographic factors: increased life expectancy coupled with a fixed retirement age, and a decrease in the fertility rate.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/04/Old-vs-Young-Population-040417.png[/image]

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/04/Fertility-Rate-040517.png[/image]

The structural shift in employment, due to the impact of technology and automation, is an overarching problem that few give little attention to.

While the mainstream media’s focuses their attention on the daily distribution of economic data points, there is a hidden economic depression running along the underbelly of the country. While reported unemployment is hitting historically low levels, there is a swelling mass of uncounted individuals that have either given up looking for work or are working multiple part time jobs. This can be clearly seen in the chart below which is the working age population of those between the ages of 16 and 54 as a percentage of that same age group. This strips out the argument of retiring baby boomers, who ironically, aren’t retiring not because they don’t want to, but because they can’t afford to.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/08/Employment-16-54-Population-080417.png[/image]

These higher levels of under and unemployment have kept pressures on wages even as work hours have lengthened. The declines in real income are evident as the burgeoning “real” labor pool, and demand for higher wage work, is actually suppressing wages as companies opt for increasing productivity, continued outsourcing, and streamlining employment to protect corporate profit margins. However, as the cost of living is affected by the rising food, energy and health care prices without a compensatory increase in incomes – more families are forced to turn to assistance in order to survive.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/08/Social-Benefits-DPI-080717.png[/image]

Without government largesse, many individuals would literally be living on the street. The chart above shows all the government “welfare” programs and current levels to date. The black line represents the sum of the underlying sub-components. While unemployment insurance has tapered off after its sharp rise post the financial crisis, social security, Medicaid, Veterans’ benefits and other social benefits have continued to rise.

Importantly, for the average person, these social benefits are critical to their survival as they make up more than 22% of real disposable personal incomes. With 1/5 of incomes dependent on government transfers, it is not surprising that the economy continues to struggle as recycled tax dollars used for consumption purposes have virtually no impact on the overall economy.

As millions of “baby boomers” approach retirement, more strain is put on the fabric of the welfare system. The exact timing of this crunch is less important than its inevitability.

There are two critical factors driving this inevitability. The first is that the number of “real” employees, while growing, is in lower income producing and temporary jobs, and the rate of job growth is substantially lower than the growth of the population. Since social security contributions are calculated as a percentage of income – lower income levels produce lower contributions.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/08/Employment-Population-Growth-080417.png[/image]

The second factor, as shown above, is the ever larger share of personal incomes being made up of government benefits reduces social security contributions.

As stated above, the biggest problem for Social Security, and the U.S. in general, comes when Social Security begins paying out more in benefits than it receives in taxes. As the cash surplus is depleted, which is primarily government I.O.U.’s, Social Security will not be able to pay full benefits from its tax revenues alone. It will then need to consume ever-growing amounts of general revenue dollars to meet its obligations–money that now pays for everything from environmental programs to highway construction to defense. Eventually, either benefits will have to be slashed or the rest of the government will have to shrink to accommodate the “welfare state.” It is highly unlikely the latter will happen.

As millions of baby boomers begin to retire another problem emerges as well. Demographic trends are fairly easy to forecast and predict. Each year from now until 2025, we will see successive rounds of boomers reach the 62-year-old threshold. There is a twofold problem caused by these successive crops of boomers heading into retirement. The first is that each boomer has not produced enough children to replace themselves which leads to a decline in the number of taxpaying workers. It takes about 25 years to grow a new taxpayer. We can estimate, with surprising accuracy, how many people born in a particular year will live to reach retirement. The retirees of 2070 were all born in 2003, and we can see and count them today.

The second problem is the employment problem. The decline in economic prosperity, that we have discussed extensively, caused by excessive debt, reduction in savings, declining income growth due to productivity increases and the shift from a manufacturing to service based society will continue to lead to lower levels of taxable incomes in the future.

This employment conundrum is critical. Back in 1950, as the baby boom was just beginning to start, each retiree’s benefit was divided among 16 workers. Taxes could be kept low. Today, that number has dropped to 3-workers per retiree, and by 2025, it will reach–and remain at–about two workers per retiree. In other words, each married couple will have to pay, along with their own family’s expenses, Social Security retirement benefits for one retiree. In order to pay promised benefits, either taxes of some kind must rise or other government services must be cut. Back in 1966, each employee shouldered $555 dollars of social benefits. Today, each employee has to support roughly $18,000 of benefits. The trend is obviously unsustainable unless wages or employment begins to increase dramatically and based on current trends that seems highly unlikely.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/08/Social-Benefits-Per-Employee-080717-2.png[/image]

The entire social support framework faces an inevitable conclusion where no amount of wishful thinking will change that outcome. The question is whether our elected leaders will start making the changes necessary sooner, while they can be done by choice, or later when they are forced upon us.