Authored by Kevin Muir via The Macro Tourist blog,

In 1992, the CBOE hired Robert Whaley to develop a tradeable volatility product on equity index option prices. A year later, in 1993, the VIX was born when the CBOE started publishing real-time quotes on the implied volatility of the calculated S&P 500 index options. In those early days, I very much doubt Robert ever imagined his volatility index would someday be the cornerstone of some of the world’s most actively traded ETFs. In fact, for the next decade, no VIX instruments traded at all, and it wasn’t until 2004 that the VIX future was listed. And then, it took another five years before the first ETF based on those futures hit the exchanges. But what a ride it’s been.

Nowadays, everyone knows the VIX index. It’s no longer some arcane index reserved for derivative traders, but instead a highly liquid, easily traded way to bet on future implied volatility. And I doubt most participants realize that last part. They are not betting on current volatility. They are not betting on future volatility. They are betting on future implied volatility. Remember that point. It’s important. We’ll come back to it later.

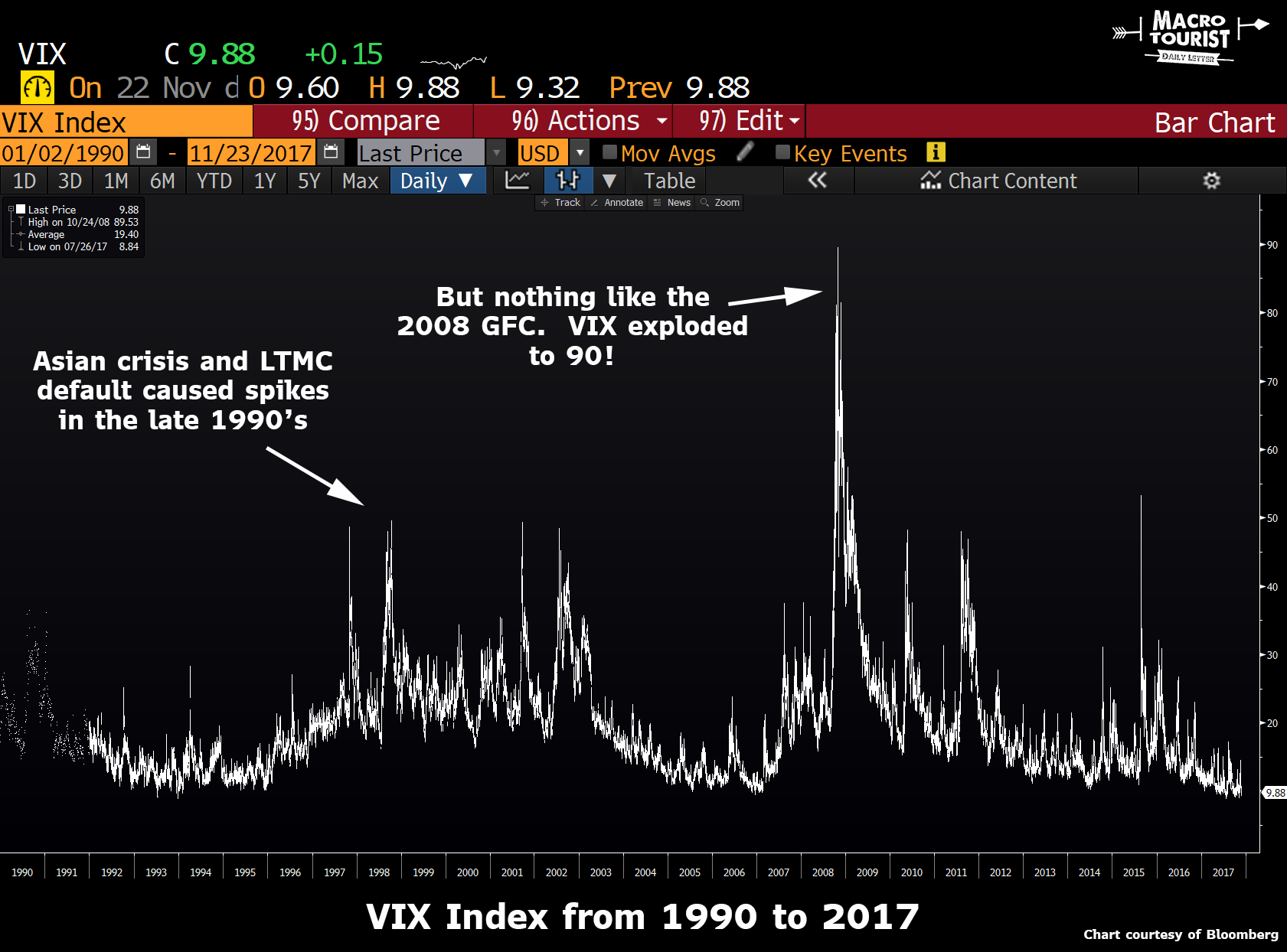

During the 2008 Great Financial Crisis, implied volatility went through the roof.

It had spiked during other crises, like Long Term Capital Management and the Asian crisis, but nothing like 2008.

The Great Financial Crisis saw VIX explode to over 90. It was truly mind boggling. The amount of future volatility the market was pricing in was unprecedented. No one trusted anyone, the financial system was imploding, and everyone was desperate to buy insurance.

And then, just like that, like all crises, it passed. But in the ensuing years, the panic might have been over, but it wasn’t forgotten. And since buying VIX had been the home run trade of the last crash, investors kept going back to VIX long positions like Lindsay Lohan goes back to the bar. So even though the actual volatility of the stock market had declined to normal levels, investors kept paying too much for the insurance, betting that future volatility would once again rocket higher.

This chronic overpricing led to one of the greatest trades of the past few decades. Sure, buying VIX before the 2008 spike was profitable. But you needed to be nimble and get the timing right. After all, it wasn’t up there for long. Yet, shorting VIX - that was the trade that kept giving. For the past 7 years, it has consistently been one of the most outstanding trades the financial world has ever seen.

Don’t believe me? Look at this chart of the VXX ETF. The VXX has split countless times, so this chart reflects those splits. From 2009, when it was trading at a split adjust level of almost $120,000 per share (yup - you read that right - 120k), it is now trading at $32.

Just for kicks, I figured out the Sharpe Ratio of the VXX over the past year. It is -5.3! This means shorting VXX has been a consistent, and hugely profitable strategy, with surprisingly low draw-downs.

Hedge fund managers do terrible unspeakable things for Sharpe Ratios of 2.5 or 3, so finding an asset with 5+ is probably awfully demoralizing.

It’s no wonder everyone is shorting VXX.

Which brings me to present day. For the longest time, I felt the concerns from the VIX were overblown.

For years, market pundits have been bandying about charts meant to scare investors about the potential dislocation in the VIX market. I even wrote a piece called, The VIX Article no one will like.

Yet the frenetic pace of VIX shorting has intensified to a level that frightens me. There is now $1.2 billion of market cap of the inverse VIX ETF XIV, with another $1.3 billion of SVXY (another inverse ETF). This is insanity. Robert Whaley never expected his little VIX product to be the epi-centre of a multi-billion dollar casino. To me, this just reeks of the old Warren Buffett quote - “what the wise do in the beginning, the fool does in the end.”

I wonder how many of these short VIX investors understand the products they are buying? With VIX currently at 10, a simple move back to 20, the longer term average, would mean a doubling of the index, and if it was quick enough, could wipe out these two inverse ETFs. For example, the XIV has a provision to wind down if the NAV declines by 80%. Think about that. One missile from Little Rocket Man aimed at Guam or Hawaii, what do you think VIX trades at? My guess is that opens at 25 and gets uglier from there. Or how about a simple flash crash? It’s not as if these markets are deep and liquid. If Central Banks step back (or heaven forbid pull out some pink tickets), it could easily cascade. Regardless, at these VIX levels, 80% moves are by no means unrealistic.

What about the VIX futures? ETF managers use them to hedge their products, but there are also outright speculators. What’s the margin required on these instruments? The exchange minimum is $6,200 for the front month - representing 53% of the underlying, $4,000 for the next month - which works out to 31% and the far months are $2,500 - at just 17% of the total value of the contract. Again, this is not nearly enough. And shrewd brokers that understand risk, like Interactive Brokers, are adjusting for this reality. IB has decided to require margin for a 10% overnight move in the S&P 500. Harsh, but not out of the realm of possibilities. They have calculated that this would translate into a VIX level of 37. That means, IB clients need to put up more than 300% of the underlying value of the contract if they want to short VIX futures. Probably overkill, but given that few other brokers understand this risk, maybe justified.

If we get a sharp move higher in VIX, there will be snowball effect. If it is big enough, monster positions, like $2.5 billion of short VIX ETFs will have to be bought back in a hurry. And let me break it to you, there is no one large enough to take the other side of that trade. At least no one willing to do it without extracting many pounds of flesh first.

Don’t forget, VIX futures are the forward levels of implied volatility, not actual volatility. VIX can trade at 50 while the S&P 500 index has an actual volatility of 15. There is nothing but arbitrageurs keeping this in line. Yet in a crisis, stupid shit happens all the time. How many new sellers will be there ready to takeover an upward spiraling VIX position? Let me break it to you, it’s going to be a lot higher than the current quote.

Now there really isn’t anything new in my concerns. Yet another wanna-be-wise guy warning about the over popularity of the short VIX trade. Take a number and join the queue.

But recently I was talking with MacroVoices’ Erik Townsend about my worries. After letting me stumble around citing my reasoning, Erik said, “you know Kevin, it’s actually much worse than that,” and here is where Erik’s deduction outshone my own, “in that unwind scenario you are describing, there is a high likelihood that some market participants will find they do not have adequate margin, and will find themselves in a negative equity position.” I instantly understood the brilliance of Erik’s comment. Let’s say VIX rises 80%, and the XIV gives notice that they are closing the fund. They have another 20% of equity to buy back their short, but what if it skids through that? What if it costs them an extra billion dollars to get their short back in? Who is on the hook? Chances are, it’s the clearing houses.

A VIX spike is dangerous not only for everyone that is playing in the VIX square, but for all market participants. Given the size of the VIX complex, it has the potential to destabilize the entire financial system on its own. If the move is abrupt and large enough, it will not only bankrupt many different parties, but will cause a ripple effect in other markets. Not only that, but chances are that a VIX spike will be the result of some other factor that markets will need to deal with, so the threat to the clearinghouse system from a VIX debacle will only exacerbate the problem.

Erik instantly grasped the real worry. It’s not that a bunch of target managers will lose their fortunes that they have accumulated over the past half decade shorting VIX. No, the real worry is that they lose a whole lot more.

Erik gets it. Interactive Brokers gets it. Guys like Jesse Felder who have been warning on this for a while get it.

I finally get it. Shorting VIX, at these low levels, in the size they are doing, is not only dumb, but crazily dangerous, not only to the parties trading it, but also to the stability of the entire financial system.

I always emphasize that the next crisis won’t look anything like the past one. And when hedge fund managers make fancy presentations of the coming collapse in high yield credit or real estate, I usually just ignore them. After all, that’s what happened last time. It won’t be the same. But how ironic would it be, if the instrument that was the hands-down winner during the last crisis (VIX), ended up causing the next crisis because too many people were short it?

* * *

PS: As Erik outlined in the recent MacroVoices podcast, if there is a situation where short VIX players find themselves in a negative equity position, the authorities will go looking for someone to share that cost. It might not be fair, it might not be right, but there is a chance they will arbitrarily decide to take away profits from those that were long. They could do this many ways, but an easy solution would be to fix the VIX level at a lower level than where the market was trading. They would cite “disruptive” conditions or some other BS like that. But make no mistake, in a crisis situation, the authorities will do whatever it takes to keep the system solvent. That might include “fixing” the VIX. Be aware if you are trading from the long side, counting on the profits to protect your portfolio. There is simply so much risk in this VIX complex, I would be wary. And if you insist on giving it a whirl on the long side, my advice - get out before the shit really hits the fan.