Submitted by Lance Roberts via RealInvestmentAdvice.com,

Yesterday, Janet Yellen announced the first hike in the Fed Funds rate in eleven years from .25% to .50%. When asked about why the Fed decided to raise rates now, Ms. Yellen responded by suggesting that the “odds were good” the economy would have ended up overshooting the Fed’s employment, growth and inflation goals had rates remained at low levels. She then went on to state that it was a “myth” that economic growth cycles die of “old age.”

While such an optimistic outlook for economic growth was certainly welcomed by the markets, both of her statements expose the challenges that lie ahead for the Fed.

Tick-Tock, The Fed Starts The Clock

Ms. Yellen is correct in stating that economic growth cycles do not die of “old age.” It is historically the impact of an exogenous impact that ultimately slows economic growth rates into a recessionary cycle. What Ms. Yellen failed to explain is that historically it has been the “tightening” of monetary policies that have been the “exogenous impact” to the economic growth cycle.

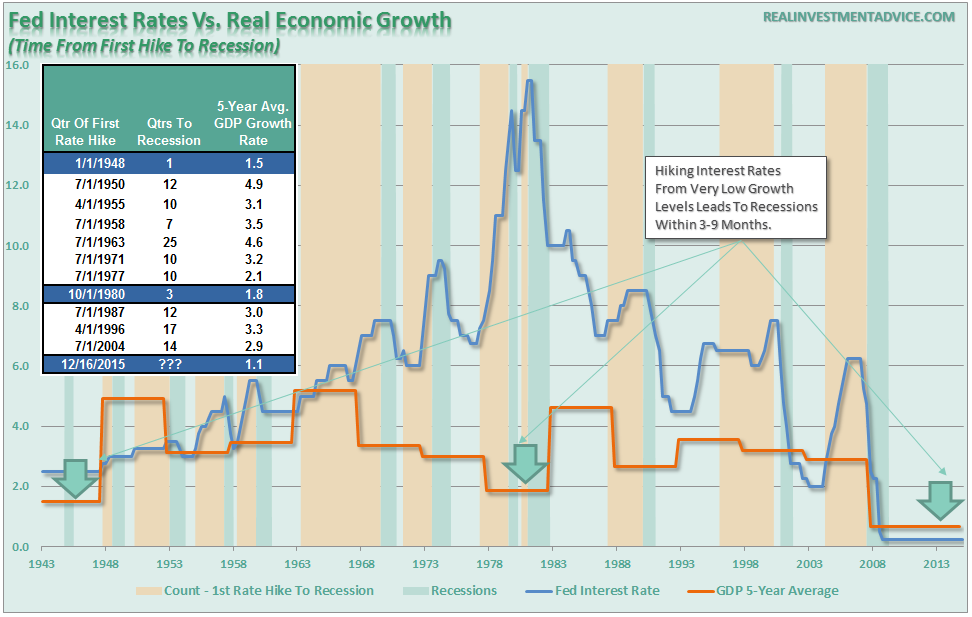

Looking back through history, the evidence is quite compelling that from the time the first rate hike is induced into the system, it has started the countdown to the next recession. However, the timing between the first rate hike and the next recession is dependent on the level of economic growth at that time. As I stated earlier this week:

“When looking at historical time frames, one must not look at averages of all rate hikes but rather what happened when a rate hiking campaign began from similar economic growth levels. Looking back in history we can only identify TWO previous times when the Fed began tightening monetary policy when economic growth rates were at 2% or less.

(There is a vast difference in timing for the economy to slide into recession from 6%, 4%, and 2% annual growth rates.)”

“With economic growth currently running at THE LOWEST average growth rate in American history, the time frame between the first rate and next recession will not be long.”

Given the reality that increases in interest rates is a monetary policy action that by its nature slows economic growth and quells inflation by raising borrowing costs, the only real issue is the timing.

As Sam Zell noted yesterday:

“I think this interest rate hike is too late, this economy is closer to falling over than it is to going up. I think there’s a high probability that we’re looking at a recession in the next twelve months.”

Looking at the historical data above, Zell’s timing appears to be just about right.

Fed Rate Hikes And Bull Markets

The other common meme this morning, following yesterday’s rate hike decision is that “stocks have nowhere to go but up.”

Again, this is a timing issue. If you have a very short-term view, history suggests that stocks do rise on average following an initial rate hike. However, as shown in the chart below, historically rate hikes have occurred when earnings growth was on the rise, not peaking and deteriorating.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/Profit-Margins-Fed-Funds-1214151.png[/image]

Furthermore, as explained by Jason Goepfert of Sentiment Trader yesterday:

“The S&P 500, gold and 10-year Treasury note yield are all up by more than 0.5% on the day. The knee-jerk assumption from that would be that traders are pricing in higher inflation.

This is occurring on a day the FOMC raised its Federal Funds target rate. If we go back to 1971 and look for every time all three rallied at least 0.5% on a day the Fed hiked rates, we get the following future performance.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/Sentiment-Trader-121615.png[/image]

However, if we step our time frame out to longer-term, since we are all supposed to be long-term investors, the outlook becomes rather grim.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/Fed-Funds-Table-121715.png[/image]

In every single instance when the Fed has started a rate hiking campaign, that campaign ended in a market correction or worse. (The Fed then began lowering rates immediately to stop the ensuing carnage.)

With corporate profits deteriorating, economic growth weak and the dollar surging, the Fed is very late to the game. This puts the time frame between now and the next recession at the very short end of the scale.

Growth So Bright, Lower Outlook

One thing that is always interesting is comparing what the Fed “says” during their press conference and then looking at the history of their own forecasts.

During yesterday’s press conference, Ms. Yellen made several references, as noted above, about the strength of the economy and that despite the surging dollar and collapsing oil prices, everything should continue to improve. The problem is that is NOT what was reflected in their forecasts released along with their announcement.

The table/chart below shows the history of the Fed’s average range of their estimates going back to 2011 when they started releasing their forecasts as compared to what actually occurred.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/FOMC-Forecasts-GDP-121715.png[/image]

Currently, economic growth forecasts for 2016 and 2017 are at their lowest rate since the Fed began predicting for those two years. Furthermore, it is worth noting that for 2015, the Fed had originally estimated growth to be 3.35% rather than the current run rate of 2.2%.

Furthermore, they lowered their long-term outlook to just 2.05% from 2.25% at the last release.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/Yellen-GrowthForecasts-121615.png[/image]

Yes, please meet the “worst economic forecasters” ever. And while the mainstream media quickly laps up the optimistic outlook of the Fed, you might want to consider their own record of forecasts when making long-term investment bets.

Based on statistical history combined with the current underpinnings in the market, the outlook really isn’t as bright as Ms. Yellen suggests.