Authored by Richard Rosso via RealInvestmentAdvice.com,

The financial terrain is strewn with robust fables cleverly disguised as facts.

The setbacks to financial security due to stock market returns never realized, the precious time and human capital necessary to make up for market losses, the ingenious data-mining undertaken by populist gurus that want you to believe that stocks are a panacea; talking heads at big-box brokerage firms disguised as fiduciaries who make fortunes convincing investors to feel silly for being cautious.

The deck is stacked against the retail investor.

Now more than ever.

As the majority, this marketing force cranks out stories and grinds down the painful past of market events into the mist of averages. They so want investors to forget the past.

And like the destruction of so many pebbles on this road, your retirement and other financial life benchmarks are left as rubble.

The tenacious nature of outdated financial tenets is never questioned.

These rules of thumb, words that should weigh a thousand pounds each, roll off the tongues of financial pros and layman alike as lightly today as they did generations ago.

Rancid bits of wisdom preached as gospel.

Thank goodness this isn’t medicine.

Sickness would still be drained by leeches.

Let’s bust open the stories and myths that place your efforts to build wealth in danger.

Myth #1 – Compound interest will make you rich.

Compound interest is the coolest story ever, but that’s about it.

You so want to believe it.

And there was a time you could.

But not so much today.

Albert Einstein is credited with saying “compound interest is the eighth wonder of the world.” ?Well, that’s not the entire quote.

Here’s the rest: “He who understands it, earns it; he who doesn’t pays it.”

I’m not going to argue the brilliance of Einstein although I think when it comes down to today’s interest-rate environment he would be quite skeptical (and he was known for his skepticism) of the real-world application of this “wonder.”

First, Mr. Einstein must have been considering an interest rate with enough “fire power” to make a dent in your account balance.

Over the last eight years, short-term interest rates have remained at close to zero, long term rates are deep below historical averages and are expected to remain that way for some time.

Indeed, compounding can occur as long as the rate of reinvestment is greater than zero, but there’s nothing magical about the “snowballing” effect of compounding in today’s rate environment.

Most important: Compounding only works when there is NO CHANCE of principal loss. It’s a linear wealth-building perspective that no longer has the same effectiveness considering two devastating stock market collapses which have inflicted long-term damage on household wealth.

What good is compounding when the foundation of what I invested in is crumbling?

Perhaps you should focus on the “he who understands it, earns it; he who doesn’t pays it.”

What does that adage mean to you?

Empowerment comes from living simply, avoiding credit card debt, and searching out deals on big ticket items like automobiles and appliances.

Don’t?give compound interest another precious thought.

If it comes along, consider it a great gift. A bounty.

Fine tune what you?can control and that primarily has to do with outflow or household expenses.

I believe the eighth wonder of the world is human resolve in the face of economic reality post-Great Recession.

Not compound interest.

Myth #2 – Ditch that latte and energize your wealth.

This advice is as bitter as the gas station brew that languishes in stained pots poised hot burners way too long.

Mega-money celebs like Suze Orman and Dave Ramsey fall all over themselves with wisdom that attempts to make you feel guilty for waiting in the coffee line at Starbucks. Listeners and readers of these two customarily are served swill like this on a regular basis.

A sweet topping on the sentiment is the tempting promise of consistent, annual investment returns of 10 to 11% in the market which is as far from reality as a broker without a sales quota.

Re-directing $2.50 from simple, daily enjoyment into risk assets is not going to move your wealth needle but you may wind up with a heck of a headache from caffeine withdrawals.

Sorry.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-145Yrs-Nominal-vs-Real-Return-011717.png[/image]

In the book, “Pound Foolish” author and financial blogger Helaine Olen investigates and busts open the myths of personal finance in an entertaining yet thorough tell-all. Helaine discovered the latte factor surfaced as far back as 1994 in a Money Magazine article.

Touted by Suze Orman in her 1999 bestseller “The Courage To Be Rich” the perky, blonde-top advocate for savvy personal financial choices was downright polemic about the subject (perhaps from overloading on caffeinated beverages whilst writing).

There’s no doubt your uptown caffeine addiction is under siege by pundits who take themselves so seriously they believe they can peddle trivial watered-down financial Pablum and you’ll take it in, bask in epiphany, see a white light. Frankly, the only thing high-octane about this wisdom is the egos it took to deliver it.

With close to three decades of financial services industry experience under my belt, I have yet to witness anyone pump an arm in victory over the wealth they’ve accumulated by reducing coffee intake.

To place it in perspective, $2.50 a day, invested for 30 years at 4% will provide a whopping $1,691 “windfall” not adjusted for inflation, investment fees and charges.

What’s your return on satisfaction for $2.50 a day? I think it’s a bargain if a small purchase provides a big breather, peace of mind, and a recharge to carry on with important tasks.

Purchase the coffee. Buy a cup for me while you’re at it.

Deprivation of simple pleasures is not a path to financial fulfillment. While you’re partaking, place the time aside with pen and paper (put the smartphone away), and in a sentence, describe your ongoing relationship with money.

In simple sentence number two, identify a single financial action that achieves three-digit success each month. In other words, if you’re going to make a change, do it with gusto. Consider how can you cut $100 a month in expenses and direct the funds into an emergency savings account first, investments after you’ve accumulated three to six months of living expenses in financial cushion.

Last, create a rule for the big stuff. This could be tough (and ostensibly may require that brain boost from that make-or-break-your-finances latte).

A tenet I created is featured in a new book titled “WORTH IT,” by Amanda Steinberg a friend and fintech thought leader with a passion to help girls and women begin, improve and prosper in their relationships with money and debt:

“Never take on a mortgage that exceeds twice your gross income.”

Or:

“House Mortgage = 2X Gross Salary.”

It’s simple. To the point. If you earn $50,000 a year, the mortgage you obtain cannot exceed $100,000. This is not house price. It’s the mortgage. For most it’s going to mean a much greater down payment or smaller dwelling.

Obey and respect your personal formula. You’re going to hate the boundaries and that means they’ll be uncomfortable and successful if consistently followed.

Avoiding house-poor will super-charge your ability to build wealth. Now, that end result I have indeed witnessed from people I’ve been grateful to counsel over the last three decades.

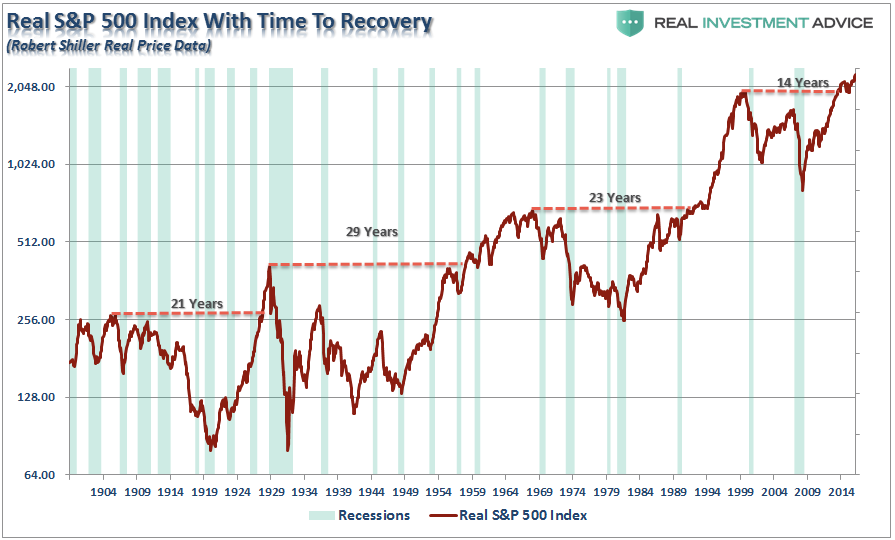

Myth #3 – The Rule of 72.

Where do I begin with this rule after I’m done hemorrhaging from disappointment?

Recently, a well-known financial showman was lamenting, stretching the meaning (again) and hitting sound effect buzzers over this pearl.

As a reminder, the Rule of 72 is a method to determine how long an investment will take to double given a fixed annual rate of interest. Just divide 72 by an annual rate of return.

When working with low rates of return, interestingly, the rule is precise. As returns increase, the rule gets less precise per Investopedia.

Yet, this rule is bandied about when it comes to stock investing where rates of return are anything but fixed.

As of the morning of this writing I had met with two couples who still maintain carryforward losses from the tech bubble that popped in 2000.

Perhaps, the Rule of 72 should be reworked to consider how long it may take to recover from investment setbacks.

Could it be plausible that it may take 72 years to fully utilize losses incurred during the tech bubble and the financial crisis?

Hey, that’s nowhere near as farfetched as applying the Rule of 72 to volatile investments.

When you come across this rule again (and if you haven’t yet, you will), I need you to remember that it only holds water for fixed, low rates of return which clearly rules out stocks.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Promised-Actual-Returns-011817.png[/image]

Myth #4 – I read somewhere that I should use the formula 100 minus my age to determine how much of my money needs to be invested in stocks.

I abhor this creation.

What does age have to do with how much of a portfolio is allocated to riskier investments like stocks?

I’m not willing to believe those who are younger should be more exposed or increasingly vulnerable to market risk than anybody else, when the reward from stocks is less for every investor going forward.

This rule is a clear disadvantage for all including beginners.

An investment allocation must be customized for your life, needs, and your sheer will to withstand volatility. Most important, it should be based on the valuation conditions that exist at the time you’re looking to place dollars into the market.

I witness cookie-cutter dogma blindly followed and money invested immediately regardless of where stocks are valued. Ultimately, the forward returns are anemic or wealth destroyed altogether.

Financial consultants and brokers have needles deep stuck in thought grooves. It’s not just this rule per se. It’s the belief that younger people must, MUST be more aggressive because they have time to weather through disaster.

Risk couldn’t care less about how old you are. When the environment is favorable to take on greater risk for higher returns, then why be so focused on age?

How would you perceive my advice if I explained that you should fasten your seatbelt before driving however, your 18-year-old child doesn’t need to be concerned about doing the same?

I mean, after all, if there’s an accident and injuries suffered, common sense tells me you may require a longer convalescence period, correct?

Not to be flippant, but I can make a formidable case that based on savings accumulated, earning power, and driver (investment) experience, that the older, wiser navigator may forgo the seat belt but the novice cannot. Never.

Think about it.

Myth #5 – Stocks always outperform bonds.

They do?

I heard this gem from an industry pro on CNBC the early morning of 3/17.

Hey if a financial guru proclaims it, and a powerhouse backs it up, it must be truth.

Over the long term, stocks do better. Since 1926, large stocks have returned an average of 10 % per year; long-term government bonds have returned between 5% and 6%, according to investment researcher Morningstar.

Don’t ask me why 1926 is so magical a launching pad for the formation of those colorful charts every broker whips out at every meeting. You’ve seen them.

Perhaps, it’s because there’s limited data set and deciding to preach from an arbitrary point in time just feels right?

Seems plausible.

The gatekeepers of finance who make rules for investors and professionals to follow like lemmings, create pretty pictures that we’re never to question.

Frankly, I don’t care why 1926 is so special. Neither should you.

It’s irrelevant to your situation and the cycle you’re either accumulating or distributing wealth through.

The coolest tidbits of 1926 involve increased gangster warfare and bloodshed employed to establish territory for illegal alcohol distribution.

Depending on how I slice and dice the data, I can show a magnificent run for bonds when compared to stocks.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/03/PTTRX-vs-SP500.jpg[/image]

The chart above outlines the performance of the PIMCO Total Return Bond fund, an intermediate duration bond fund offering (and one of the most popular), compared to S&P 500 beginning in 1999.

Why 1999?

Because I wanted to, that’s why.

Appears to me that stocks don’t always outperform bonds.

What do you see?

Silly myths, misused snippets of information, creative data mining.

They’re all not so silly when your wealth is on the line.

Are they?

Things get serious.

And so many myths and stories need to die away.

Never to return.