Submitted by Lance Roberts via RealInvestmentAdvice.com,

In the last “Technical Update” I discussed the outlook for 2016 (you can also get the full version here) and the risks that lay ahead as we approach the end of the first half of the full market cycle.

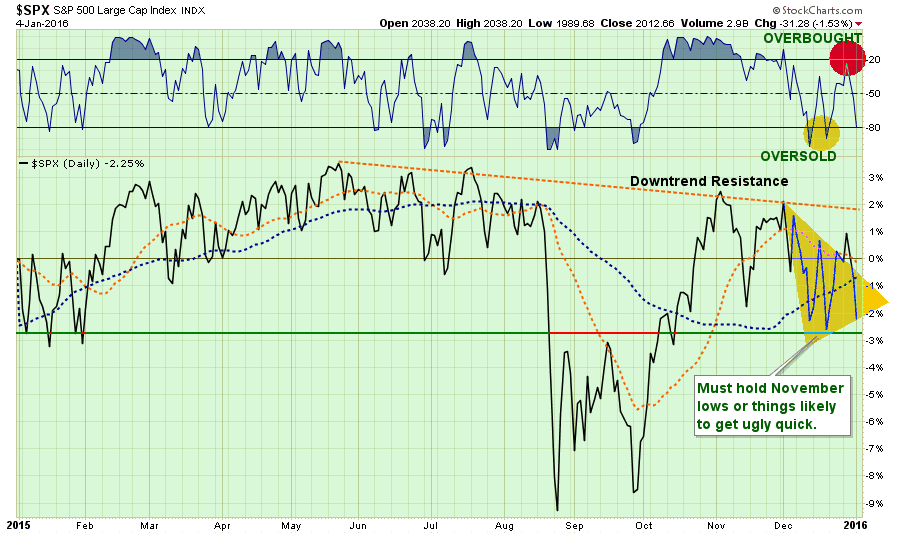

The New Year, unfortunately, started off with the wrong kind of bang. However, the sell-off was not unanticipated. As I stated previously, a lot of the selling in December was a result of capital losses being taken by institutional players for tax purposes for the 2015 tax year. Monday’s decent was the opposite. Most of the action appeared to be capital gains harvesting for the 2016 tax year where taxes will not have to be paid for 15 months.

I say this because the focus of the bloodbath on Monday was last years big winners – the FANG trade: Facebook (-2.33%), Amazon (-5.76%), NetFlix (-3.86%), and Google (-2.25%). Financials, Healthcare, Mid/Small-Cap and Emerging Markets also took a pretty healthy beating.

However, regardless of the reasoning behind the sell-off, the technical downtrend that begin in December remains firmly entrenched. As I wrote last week:

“After a second attempt at the downtrend resistance, the market has built an accelerated downtrend. If the market is unable to reverse this decline in short-order, the odds of a more substantial correction increase.”

(Chart updated through Monday’s close)

Importantly, the ongoing topping process continues in earnest. As shown in the two charts below, the current topping process is very akin to the processes witnessed at the previous two major market peaks in 2000 and 2007.

You can clearly see the topping process being made over the last 18 months in the market. Until, or unless, the market can break out of the current downward trend, the risk of lower asset prices remains elevated.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/SP500-MarketUpdate-010516-3.png[/image]

As I stated above, the chart below shows the current topping process at the peaks of the last two major bull markets. The current topping process has been extended due to ongoing global bank interventions (and a lot of exuberance) but even those interventions now appear at risk of no longer working.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/SP500-MarketUpdate-010516-2.png[/image]

A Fundamental Topping Process?

While price action certainly appears to be taking the shape of a topping process, we can also see similar issues emerging in more traditional fundamental measures of the market as well.

For example, take a look at corporate profits as a percentage of GDP. While it is widely hoped by analysts that the current slump in corporate profitability is only a transient issue due to slumping oil prices, a more historical perspective suggests the current profit cycle has come to an end. Previous peaks in corporate profits have led more severe declines in the financial markets as well as the onset of recessionary environments.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/Profit-Margins-GDP-SP500-010516.png[/image]

Valuations also suggest the current bull market may be close to completing the first half of the full market cycle. While many look at the smoothed 10-year valuation measure (CAPE), a shortened 5-year analysis has provided a better leading indicator of market cycles.

Note that peaks in the 5-year cyclically adjusted P/E ratio have typically led major peaks in the inflation-adjusted S&P 500 index.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/PE-CAPE5-010516.png[/image]

We can also see evidence of a more fundamental weakness in the markets by looking at market capitalization as a ratio to economic growth (GDP). The first chart below is the inflation adjust S&P 500 index market capitalization as compared to real GDP. There are two things of importance to note:

- The current peak in the market cap/GDP ratio is the second highest in history.

- While early in the process, the current peak has many of the same structures which led to previous major market downturns.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/SP500-MarketCap-GDP-010516.png[/image]

The same can be seen in Warren Buffet’s favorite valuation indicator. The Wilshire 5000, which is a very broad market index, provides a better measure of total market activity. Currently, as with the S&P 500, the Wilshire 5000 market cap is at levels only witnessed previously during the “dot.com” mania. While this particular indicator has not begun to peak as of yet, it remains an important reminder of the extreme valuations that current exist in the financial markets.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/Buffett-Indicator-0105161.png[/image]

From both from a technical and fundamental view, the markets appear to be in the process of forming a cyclical top. While such a view is considered “bearish” and quickly dismissed in the “hopes” of further market gains, it should be remembered that such is part of the normal full market cycles that have existed throughout the entirety of the financial markets. As shown in the chart below, the combination high prices and valuations have been the hallmark of the conclusion of the first half of the cycle.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/SP500-Full-Market-Cycles-010516.png[/image]

Lastly, as I wrote previously in “All Bubbles Are Different:”

“Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.

The chart below is an example of asymmetric bubbles.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/Asymmetric-bubbles.png[/image]

The pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market which can create a feedback loop between the markets and fundamentals.

This pattern of bubbles can be clearly seen at every bull market peak in history.The chart below utilizes Dr. Robert Shiller’s stock market data going back to 1900 on an inflation adjusted basis with an overlay of the asymmetrical bubble shape.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/Asymmetrical-Bubbles-010516.png[/image]

There is currently a strong belief that the financial markets are not in a bubble. The arguments supporting those beliefs are all based on comparisons to past market bubbles.

The inherent problem with much of the mainstream analysis is it assumes everything remains status quo. However, the question remains of what can go wrong in the markets? In a word, “much.”

Economic growth remains very elusive, corporate profits appear to have peaked, and there is an overwhelming complacency with regards to risk. Those ingredients, combined with a tightening of monetary policy by the Federal Reserve, leaves the markets more vulnerable to an exogenous event than currently believed.

It is likely that in a world where there is “little fear” of a market correction, an overwhelming sense of “urgency” to be invested and a continual drone of “bullish chatter;” markets are poised for the unexpected, unanticipated and inevitable completion of the full market cycle.

Take a step back from the media, and Wall Street commentary, for a moment and make an honest assessment of the financial markets today. If our job is to “bet” when the “odds” of winning are in our favor, then exactly how “strong” is the fundamental hand you are currently betting on?

This “time IS different” only from the standpoint that the variables are not exactly the same as they have been previously. Of course, they never are, and the result will be “…the same as it ever was.”