Authored by Lance Roberts via RealInvestmentAdvice.com,

Review & Update

In last week’s “Technically Speaking” post I discussed the S&P 500 hitting 2700 by Christmas. To wit:

“As stated in the title, the current push higher puts 2700 in sight by the time Santa fills the ‘stockings hung by the chimney with care.’

As shown below, price momentum triggered a short-term “buy” signal following Thanksgiving, and after the brief ‘AMT Tax Debacle’ in the Senate Tax Bill, momentum again has turned up as prices continue to press higher.”

As noted above, this “momentum” keeps portfolios allocated towards equity risk, but we continue to be prudent about the risk we are taking and continue to hedge risk as necessary.

After discussing that “dip” in the market caused by concerns over the current “tax reform” proposal, I followed up with an analysis of the Federal Reserve’s balance sheet manipulations. Unsurprisingly, I discovered the following:

“With global Central Banks still flooding the system with liquidity, the Fed has yet to begin rolling off their reinvestments as expected. In fact, the Fed made a timely reinvestment during the “Senate Tax Bill” debacle earlier this month.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Fed-Balance-Sheet-Changes-121117.png[/image]

Of course, that bump of liquidity sent asset prices rocketing higher.

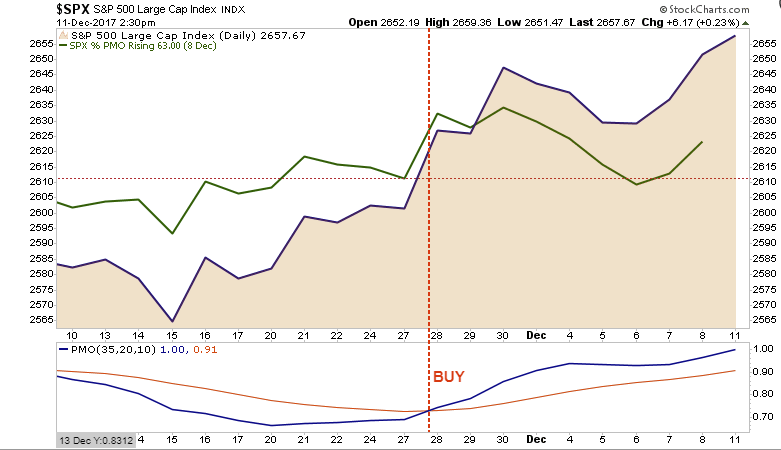

Then on Thursday, we saw a brief slide in equities as concerns once again rose over the potential for the tax reform legislation to be blocked by several Senators who were leaning towards voting “no” on the bill. However, those concerns lasted only momentarily and stocks rocketed higher on Friday ending the week on a positive note. With concerns over tax reform fading, equities are sitting at all-time highs and within striking distance of 2700 by Christmas.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/SP500-Chart1-121517.png[/image]

The current technical underpinnings remain bullish currently, but as shown below, are pushing into extremely overbought conditions. The chart below shows the 1 and 2-year moving averages with 2 and 3-standard deviations of the 1-year moving average. That deviation, combined with the most overbought readings on both RSI and MACD, suggest risk has risen markedly in recent weeks.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/SP500-Chart2-121517.png[/image]

While the conditions are very bullish heading into the end of the year, it is advisable that individuals take some actions in re-balancing risk in portfolios. As I noted last week in “The Exit Problem,” it is time to start considering sitting a little closer to the “exit.” To wit:

“Am I sounding an ‘alarm bell’ and calling for the end of the known world? Should you be buying ammo and food? Of course, not.

However, I am suggesting that remaining fully invested in the financial markets without a thorough understanding of your ‘risk exposure’ will likely not have the desired end result you have been promised.

As I stated often, my job is to participate in the markets while keeping a measured approach to capital preservation. Since it is considered ‘bearish’ to point out the potential ‘risks’ that could lead to rapid capital destruction; then I guess you can call me a ‘bear.’

Just make sure you understand I am still in ‘theater,’ I am just moving much closer to the ‘exit.’”

What does that mean? Here are the rules once again which guide the investment process in our shop. It is through following these basic rules that, with the markets overbought, underlying fundamentals stretched, we continue to suggest some portfolio actions be taken to reduce, not eliminate, overall risk.

-

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says “sell everything and go to cash.”

However, being a bit more cautious at this juncture will likely pay dividends. As I have stated over the past several weeks, if tax reform does pass, it now looks likely that it will become effective in February, 2018. If that is the case, the setup for an early January/February sell-off in the markets is likely as portfolio managers lock in gains. While I have NOT added a short-position to portfolios as of yet, the setup by year-end is becoming much better with the excessive price extension in the market.

Final Tax Bill Details

On Friday, Kevin Brady of the House Ways and Means Committee was on my radio program discussing the bill which was released later that day.

https://w.soundcloud.com/player/??

Here are the details of the release he referenced in the interview.

- Seven rates, starting at 10 percent and reaching 37 percent for incomes above $500,000 for singles and $600,000 for married, joint filers. ALL EXPIRE IN 2025.For joint filers:

- 10 percent: $0 to $19,050

- 12 percent: $19,050 to $77,400

- 22 percent: $77,400 to $165,000

- 24 percent: $165,000 to $315,000

- 32 percent: $315,000 to $400,000

- 35 percent: $400,000 to $600,000

- 37 percent: $600,000 and above

For single filers:

- 10 percent: $0 to $9,525

- 12 percent: $9,525 to $38,700

- 22 percent: $38,700 to $70,000

- 24 percent: $70,000 to $160,000

- 32 percent: $160,000 to $200,000

- 35 percent: $200,000 to $500,000

- 37 percent: $500,000 and above

- Corporate Tax Rate – 21 percent, beginning in 2018.

- Pass-Through Deduction – Owners could apply a 20 percent deduction to their business income, subject to limits that would begin at $315,000 for married couples (or half that for single taxpayers).

- Individual State and Local Tax Deductions – Individuals can deduct no more than $10,000 worth of the deductions, which could include a combination of property taxes and either sales or income taxes.

- Obamacare Individual Mandate – Repeal the penalties.

- Mortgage Interest Deduction – Deductible mortgage interest for new purchases of homes would be capped at loans of $750,000.

- Medical Expense Deduction – Reduce the threshold to 7.5 percent of AGI for the tax years 2017 and 2018.

- Child Tax Credit – Double the credit to $2,000 and provide it for each child under 18 through 2024. Raise the phase-out amount to $500,000, and cap the refundable portion at $1,400 in 2018.

- Estate Tax – Double the thresholds so the levy applies to fewer estates. The higher thresholds would sunset in 2026.

Of course, the real question is how are you going to “pay for it?”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Federal-Debt-Deficit-Projections-121517.png[/image]

Even as Kevin Brady noted in our interview, when I discussed the “fiscal” side of the tax reform bill, without achieving accelerated rates of economic growth – “the debt will balloon.”

The reality, of course, is that is exactly what will happen because there is absolutely NO historical evidence that cutting taxes, without offsetting cuts to spending, leads to stronger economic growth.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/Tax-Rates-GDP-Growth-5-YearAvg-110317.png[/image]

Those, of course, are the long-term concerns that will lead to lower rates of returns for equity-based investors and will continue to suppress interest rates for the next decade as the “Japanification” of the U.S. continues.

However, in the short-run investors have thrown caution to the wind. Not only are individual investors fully allocated to stocks as noted on Thursday, but professionals have gone “all-in” to chase returns into year-end as noted by my friend Dana Lyons on Friday. To wit:

“The National Association of Active Investment Managers, or NAAIM, is made up of Registered Investment Advisors and other money managers who employ active or tactical investment strategies as opposed to buy-&-hold and passive asset allocation. For the most part, the goal of such strategies is to reduce investment risk by applying processes to mitigate losses when they view markets as high-risk. Apparently, this group sees very little risk in the market at this time — or else they see Santa’s sleigh headed this way — because they’re currently throwing all caution to the wind.

That interpretation is according to the NAAIM Exposure Index, a survey of the group’s collective equity allocation. Based on the latest reading of the Index, these active managers have an average of 109% exposure to the stock market. Yes, 109%, meaning the average manager is leveraged long. That is the highest reading in the survey’s 11-year history, and the 12th reading over 100%.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/NAAIM-Dec-2017-1170x772.jpg[/image]

As I stated previously, there was no catalyst that we know of that burst the dot-com bubble in 2000. There was no catalyst that started the slide in the markets in 2008 until it triggered the Lehman bankruptcy and “all hell broke loose.”

Today, we once again have exuberance present and there is a widespread belief that nothing will stop this runaway train.

But eventually, for whatever reason, the market will top. It is impossible to predict when, or how it will happen. It just most assuredly will, and will do so just as everything seems to be its brightest.

“It will be the rudest of awakenings for the slumbering bulls.”