To be sure, the rumors have been there for a while.

As we first wrote in March of 2015 when it became a topic of conversation, speculation that Cushing may fill, and even overflow, has been around for nearly 10 months.

As we reported then, there were floating predictions that Cushing may top out as soon as the summer of 2015.

In retrospect, these forecasts underestimated just how "stretchy" US commercial storage can be; they also ignored how many millions of barrels could and would be stored at sea even though the contango in recent months had made such storage virtually unprofitable; the recent change in the US oil exporting law helped, and much of the excess inventories were carted off toward Europe which allegedly has more oil excess capacity than the US.

However, as overproduction continues, even the highly adaptive US storage system appears to be reaching its limits. Recall that the primary reason why Goldman envisions $20 oil as a possibility is because US storage capacity will be reached.

Then yesterday, the EIA itself in a blog post took on the topic of soaring inventories.

This is what it said:

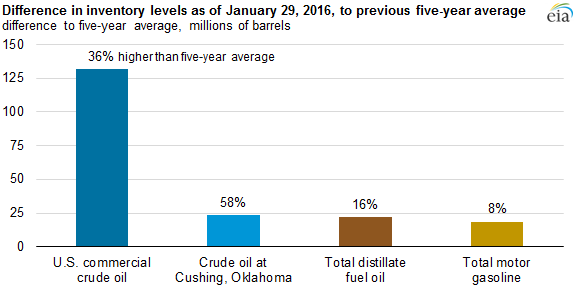

Several factors have played a part in pushing U.S. crude oil prices below $30 per barrel (b), including high inventory levels of crude oil, uncertainty about global economic growth, volatility in equity and nonenergy commodity markets, and the potential for additional crude oil supply to enter the market. Crude oil and petroleum product inventories, both domestically and internationally, have been growing since mid-2014 and are above five-year averages for this date.

Although there is still traditional, on-land storage space available, higher inventory levels and expectations for global inventories to continue building in 2016 are lowering crude oil and petroleum product prices for near-term delivery:

- Total U.S. commercial crude oil inventories as of January 29 were 503 million barrels, 132 million barrels above the 2011-15 January average. This marks the first time that U.S. inventories exceeded 500 million barrels.

- Crude oil inventories at Cushing, Oklahoma, the delivery point for the West Texas Intermediate (WTI) futures contract traded on the New York Mercantile Exchange (Nymex), are 23 million barrels above the five-year average as of January 29.

- Total U.S. distillate inventories (which include heating oil and diesel fuel) are 22 million barrels above the five-year average, and motor gasoline inventories in the United States also recently moved above historical averages.

But it was only today that we got the loudest alarm bell yet, suggesting that an "overflow" of Cushing may all too real in the not too distant future.

According to Reuters, the unprecedented build-up of surplus crude oil supplies in Cushing, Oklahoma, is beginning to cause logistical headaches for companies moving crude between thousands of steel tanks in the nation's most important storage hub.

For one company, Enterprise Products Partners, which is a large participant in the Cushing market, this means telling at least some counterparties that it is experiencing delays in delivering crude from its tanks, Reuters said citing three sources who were informed of unspecified "terminalling and pump" issues.

Alarm bell #1:

"The sources attributed the disruptions to the unusually high level of oil collecting in Cushing, the delivery point of the CME Group's U.S. oil futures contract. Stockpiles have risen to a record 62.4 million barrels as of last week, according to the U.S. Energy Information Administration, just 9 million barrels shy of their theoretical limit."

"It's hard to move barrels around right now because there's so much oil (in Cushing)," said one trader.

And if it's hard now, imagine what will happen in a few weeks let alone months, when 1-2 million barrels in excess production is dumped in Cushing courtesy of the relentless Saudis and Iranians.

For now at least, it's not a panic: "The delivery delays are unusual but not severe enough to trigger contractual disputes, one source said. Oil traders routinely pump crude in and out of tanks in Cushing in order to settle futures contracts or create particular blends for refiners. Most trades are usually completed within a month's time."

However, that is about to change:

The hiccups may be a sign of things to come as traders fear a further increase in stocks at Cushing would test the upper limits of tanks and cause the next leg of an 18-month rout.

Alarm bell #2:

Enterprise owns just 3.3 million barrels of storage capacity in Cushing, small relative to operators like Enbridge Energy Partners with over 20 million barrels. It is not clear how much space the firm may have leased from other owners. But traders say they remain one of the larger players in that market, and first noticed that something was awry when Enterprise began bidding to buy the Feb/March WTI cash roll earlier on Thursday, indicating that they were potentially short barrels for immediate delivery.

The cash roll, which allows traders to roll their long positions forward, traded at larger volumes at negative $1.00 a barrel on Thursday. Those deals raised questions among market participants as the roll does not actively trade outside of the three-day window after the settlement of the front-month futures contract.

To be sure, this is not the first time the roll was negative: a few weeks ago, during the official roll period, it traded at negative $1.95 a barrel.

However, it is becoming increasingly recurring and certainly more acute.

The problem, the sources say, appears to be related to oil volumes being so high in Cushing that there is not enough room to drain existing tanks to blend oil to West Texas Intermediate specifications.

For now, only the smaller firms are affected which is a useful warning sign. Because if and when the large guys like Enbridge get in trouble and are no longer able to store the millions of barrels on location, we won't learn about it in advance. Instead what we will see is the price of oil suddenly plunging by 5%, 10% or more percent, as attempts to clear and dump excess inventory spread like wildfire across the market.

So for those who are still long oil on hopes of some major supply disruption, or some miraculous surge in demand, consider this a fair warning that very soon things may change.