Authored by Lance Roberts via RealInvestmentAdvice.com,

Melt-Up Gains Traction

Back in November, just following the election of President Trump, I wrote about the market entering into potentially the final “melt-up” phase of the cyclical bull market.

However, while economic and fundamental realities HAVE NOT changed since the election, markets are pricing in expected impacts of changes to fiscal policy expecting a massive boost to earnings from tax rate reductions and repatriated offshore cash to be used directly for stock buybacks.

To wit:

“We expect tax reform legislation under the Trump administration will encourage firms to repatriate $200 billion of overseas cash next year. A significant portion of returning funds will be directed to buybacks based on the pattern of the tax holiday in 2004.” – Goldman Sachs

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/11/Share-Buybacks-112116.png[/image]

“But it is not just the repatriation but lower tax rates that will miraculously boost bottom line earnings. This time from Deutsche Bank:

‘Every 5pt cut in the US corporate tax rate from 35% boosts S&P EPS by $5. Assuming that the US adopts a new corporate tax rate between 20-30%, we expect S&P EPS of $130-140 in 2017 and $140-150 in 2018. We raise our 2017E S&P EPS to $130.'”

Of course, since then it has been a “fast and furious” push to buy stocks regardless of what geopolitical or economic event was taking place.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/SP500-MarketUpdate-100617-2.png[/image]

Of course, the advance is stock prices has been based purely on “hope” as nothing legislatively has actually occurred towards passing tax cuts. While no bill has been written as of yet, all of the net benefits of tax cuts has been likely priced in by the markets.

I am not discounting the rush by companies to buy back shares at the greatest clip in the last 20-years to offset the impact to earnings weak revenue growth. However, none of the actions above go to solving the two things currently plaguing the economy – real jobs and real wages.

“This is also why Trump’s recent tax cut policy will fail to fuel the economic prosperity he is hoping for. With the bottom 80% of the population still earning below $50,000 on average, a tax cut will do little to increase their consumption in the economy. Those in the top 20% may well see a tax-savings from the reform but they are already consuming at a level that will likely not change to any great degree.” – The Bottom 90% & The Failure Of Prosperity

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Fed-Survey-Top20-vs-Bottom80-Incomes-093017.png[/image]

Furthermore, from an economic standpoint, most of the indicators suggest we are in a very late stage cycle relative to the markets and are acting in similar manners as have been seen prior to the last two recessions.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/SP500-EconData-100617.png[/image]

As I stated back in November:

“The rush by Wall Street to price in fiscal policy, which may or may not arrive in a timely manner, will likely push the markets higher in the short-term completing the final leg of the current bull market cycle. This was a point I addressed back in October on the potential for a rise to 2400 in the markets. With the breakout of the market to new highs, the bullish spirits have emboldened investors to rush into the most speculative areas of the market.

For now, it is all about the ‘Trump’ trade. Which is interesting considering that just before the election we were all told how horrible a Trump election would be for the world economy.”

However, it should be noted that despite the “hope” of fiscal support for the markets, longer-term conditions are currently present that have led to rather sharp market reversions in the past.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/SP500-MarketUpdate-100617-4.png[/image]

As I addressed this past week, the current environment is diametrically opposed to that of the Reagan era “tax cuts.” Therefore, the “hopes” being built into the market may ultimately be met with rather severe disappointment.

Regardless, the market is currently ignoring such realities as the belief “this time is different” has become overwhelming pervasive. As noted last week, we increased equity exposure in portfolios with the breakout above 2500. However, with the sharp rise over the last two weeks, we are beginning to look to take some profits out of small and mid-capitalization exposure and have been aggressively buying bonds this past week.

While we remain bullishly allocated currently, we are also keenly aware of the risk. As an example, the current deviation above the long-term trend line has reached more extreme levels. There is also the issue of deviations above the long-term trend line. Trend lines and moving averages are like “gravity.” Prices can only deviate so far from their underlying trends before eventually “reverting to the mean.” However, as we saw in 2013-14, given enough liquidity prices can remain deviated far longer than would normally be expected. But even that advance finally gave way.

Currently, the deviation above the long-term trend and the first major level of support are a good bit lower. A decline to the bullish trend would be roughly a -7% decline, whereas a decline to the first major level of support would entail a -17.6% decline.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/SP500-TrendLinei-Retracement-100617.png[/image]

Given the length of time the market hasn’t even seen a 1%, much less a 3%, decline, a drop of these magnitudes will “feel” substantially worse than they are.

Most Hated Bull Market Ever?

This past week, my friend and colleague, Dana Lyons, penned the following note:

“Perma-bulls like to label this bull market the ‘most hated’ in history. While the rally is historic by some metrics, the ‘most hated’ status, to the degree that it was ever applicable, has certainly fallen by the wayside by now. To be sure, there are plenty of vocal and visible perma-bears that have been spewing copious amounts of ‘hate’ at this rally for years now. However, if one steps away from the confines of financial social media and guru-dom, evidence shows that public sentiment has grown to now reflect among the most bullish conditions in recorded history.”

I agree. As I noted in Friday’s post entitled “A Bull Market In Complacency,” both our indicator of investor exuberance and equity allocations concur with Dana’s point.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/Market-Greed-Fear-Index-100517-2.png[/image]

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/AAII-Stocks-Cash-091217.png[/image]

Dana also denotes another indicator hitting excessively bullish highs.

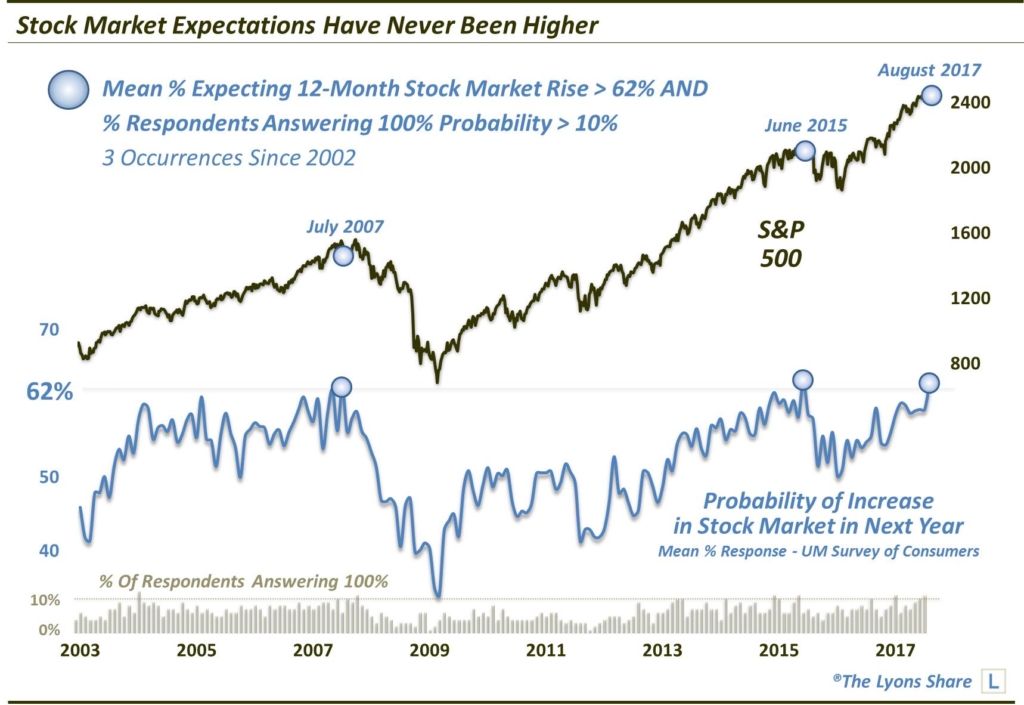

“One example comes from our Chart Of The Day based on the University of Michigan’s Survey of Consumers. One of the questions asked of respondents in the survey is their estimation of the ‘probability of an increase in the stock market in the next year’. Among the various ways that UM breaks down the data is by taking the mean response to that question. And in August’s survey, the mean response came in at 62.7%.

That trails only June 2015‘s 63.1% and joins July 2007‘s 62.2% as the only 3 readings above 62% in the history of the survey.”

And, as Jesse Felder noted this past week, the long-term return outlook is exceedingly poor.

“As Mr. Buffett has famously said, “the price you pay determines your rate of return.” Because investors are paying one of the highest prices in history, according to this measure, they are likely to experience some of the lowest future returns on record. In fact, this measure now suggests they will experience an average annual loss of 2.8% per year over the coming decade.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/Screen-Shot-2017-10-04-at-11.42.35-AM-1024x469.png[/image]

Oh, just in case you didn’t notice those charts just busted some of the most commonly held beliefs:

- There is NO CASH on sidelines

- Markets DON’T return 8% a year, and;

- Investors are all in.

This Won’t End Well

Here are some interesting stats from Adam Taggart via Peak Prosperity:

- It has been over 100 months (more than 8.5 years) since the current bull market began in April of 2009

- It has been 15 months since the last (and very brief) drop of 5% in the S&P 500

- This past September saw record low volatility, including a stretch now claimed to be “the most peaceful days in the history of the markets”

- Since last year’s presidential election, at which point the markets were already considered dangerously overvalued, the Dow Jones Industrial Average is up over 20%

- As of this article’s publishing, the Dow, the S&P, and the NASDAQ are all trading at record highs

Or visually:

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/SP500-MarketUpdate-100617-5.png[/image]

Adam goes on to state:

“The stock market is now 70% higher than it was at the previous bubble peak immediately preceding the 2008 Great Financial Crisis.

Reflect for a moment how painful the crash from Oct 2008-March 2009 was. How much more painful will a crash from today’s much dizzier heights be?

Prudent investors have asked themselves that very same question as the markets have become increasingly overvalued over the past 8+ years. Many of them — myself included — concluded that the future risks greatly outweigh the prospect of future returns, and pulled much of their capital out of the markets onto the sidelines. And since doing so, many of them — again, myself included — have watched prices climb higher and still higher again.

It’s understandable to feel great frustration both at the irrationality of today’s market prices and at the emotional sting of missing out on the gains they’ve been delivering to those who have blithely remained long.

But it’s very important to remember we’ve been here before many times throughout history (and pretty recently when reflecting back on the Tech and Housing bubbles). While today’s levels are at a historic extreme, markets have always swung from periods of overvaluation to undervaluation — and then back again.

During the peaking process, the siren call to join the party is incredibly hard to resist. Waiting out the irrational exuberance leading up to a market top is painful. Profitable returns are everywhere. How can you turn down making such easy money?

As Tom Petty sympathized: The waiting is the hardest part.”

The “siren’s song” of tax cuts and tax reforms will likely turn out to be the very rocks this ship cracks up on. The potential for disappointment dramatically outweighs the potential of Congress meeting the current expectations of the market participants.

As I noted in the 80/20 rule of investing:

“Importantly, as a portfolio manager, I am buying the breakout because I have to. If I don’t, I suffer career risk, plain and simple.

However, you don’t have to. If you are truly a long-term investor, you have to question the risk being undertaken to achieve further returns in the market.”

While we remain long the market currently, we are doing it with a very keen eye towards the risk we are taking. We continue to carry tight stop-loss levels and are de-risking portfolios by trimming exposures as needed and being opportunistic with our fixed income exposure.

As I concluded previously:

“However, the longer-term dynamics are turning more bearish. When those negative price dynamics are combined with the fundamental and economic backdrop, the “risk” of having excessive exposure to the markets greatly outweighs the potential “reward. “

While it is certainly advisable to be more “bullish” currently, like picking up a “porcupine,” do so carefully.

Investing is not a competition.

It is a game of long-term survival.”