Submitted by David Stockman via Contra Corner blog,

Whatever is going on in the daily stock market, you can’t call it “price discovery” or even remotely rational.

In fact, it amounts to grinding in harms’ way, and measures the degree to which the Fed and other central banks have turned the Wall Street casino into a giant litter of sick puppies who are bent on rolling the dice until they self-destruct.

Even MarketWatch has noted that the S&P 500 has climbed above 2100 on more than 30 occasions during the last 18 months, but has retreated each and every time.

So buying the dips in that context is based on eyes wide shut speculation; it essentially implies there is no material downside, and that one of these days the market will bust loose from its 2130 top of May 2015 and soar to spectacular new highs.

Source: FactSet

Now exactly how could that possibly happen? There is no macroeconomic or profits upsurge in sight, yet the market is already trading at 24X reported S&P 500 earnings. And even a modest 5% gain from the old May 2015 high would take valuations to a hideous 26X.

By contrast, when earnings for the S&P 500 came in at $87 share for the LTM ending in March, it signaled that corporate profits remain on a slippery slope heading due south. Last quarter’s results were down 12% from prior year ($99), and fully 18% from the cycle peak recorded for the September 2014 LTM of $106 per share.

So what is happening is that every notion of economic and earnings fundamentals has now been completely suspended. The cowardly, dithering fools who run the Fed have created a horribly dangerous one-decision trade.

To wit, the robo-machines and sicko gamblers will continue to run the chart points to the top of the current range so long as the FOMC fails to put money market rates back on a convicing path toward normalization. It goes without saying, of course, that just one lone rate increase over the course of what will be 10 full years is the very opposite of that. Yet this lunatic spell of “abnormal” will be confirmed still another time when the Fed whiffs at next week’s meeting.

That the great edifice of American capitalism is imperiled by the Keynesian simpletons who run the nation’s central bank was amply demonstrated by Janet Yellen’s latest speech to the Philadelphia World Affairs Council. To say that China is getting fixed, the junk bond bounce is a sign of stabilization and that the May jobs numbers were essentially an irrelevant, transient data point is proof of complete delusion and sheer incompetence.

Indeed, Yellen’s superficial, meandering, self-contradicting speech is the final proof that the Eccles Building is utterly lost. Any day now it will loose control of the giant incendiary bubble it has enabled, thereby paving the way for the third thundering market collapse of this decade.

After all, how is it possible that the Red Ponzi has stabilized its $30 trillion pile of unsustainable debt when in the first quarter alone China incurred new credit at a record $4 trillion or 35% of GDP annual rate?

Moreover, it is also plain as day that the spectacular flash commodity bubbles and apartment price surges that resulted from this additional dose of credit heroin have already faded and are now reversing. Contrary to Yellen, there is not a shred of evidence that the global headwinds emanating from China are abating, or that the desperate suzerains of Beijing have any hope at all of preventing an eventual crash landing.

Likewise, Yellen is beyond naïve if she really believes that the modest rebound in the junk bond market since the February lows has anything at all to do with a strengthening of the $3 trillion US market for junk bonds and bank loans. For crying out loud, the whole tottering edifice of corporate junk is due to the blind scramble for yield among bond managers and home gamers triggered by the Fed’s destructive 90-month long regime of ZIRP.

The recent bounce is purely momentum driven speculation among trend-following robo-machines and day traders. The rally does not represent an “easing” of financial conditions; its just another set-up for an eventual violent sell-off of massively over-valued junk credits.

And that get us to Yellen’s absurd reassurance that the Fed’s relentless assault on sound money is working just fine, and that the US economy is nearing the nirvana of Keynesian full employment. That is risible nonsense—-even by the lights of the Fed’s own pre-occupation with “improving labor market conditions”.

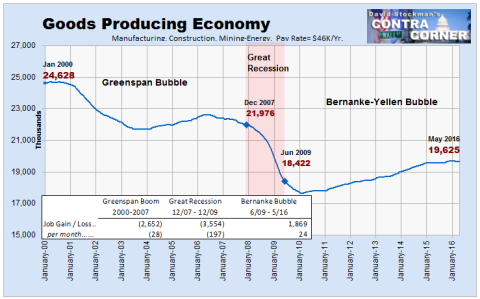

The truth is that the May report knocked the escape velocity myth dead as a doornail. Notwithstanding the trend-cycle adjusted nature of the monthly establishment survey numbers— and the fact that they are projected, not measured——there were 36,000 fewer goods producing jobs in May, and 77,000 fewer over the last four months.

Yellen can indulge in her paint-by-the-numbers delusion that the BLS’ primitive one-job-one-vote surveys measure the health of the US economy all she wants. But that doesn’t negate the fact that goods production is at the center of economic output and wealth creation even in today’s economy, and that most so-called services like shipping, warehousing, retailing, business management and contract support etc.depend upon the flow of goods production and the high incomes it generates.

As shown below, there were 19.625 million jobs in construction, mining/energy and manufacturing during May. That’s 2.2 million lower than in December 2007 and is 5 million or 20% less than the number of such core jobs posted in January 2000.

Folks, money-printing isn’t doing it in this so-called recovery cycle, which will soon be 84 months old. Nor has it since the turn of the century when the Fed’s balance sheet stood at just one-fifth of its current $4.5 trillion level.

In other words, Yellen’s Philadelphia speech was another ode to imaginary future economic gains based on the delusion that 90 months of ZIRP has actually “stimulated” the US economy. Yet the supposedly forgettable May jobs report is just one more reminder that it hasn’t.

For example, the BLS reported 71,000 new jobs in the HES Complex (health, education and social services, including state and local education jobs) during May.

That’s right. The purported number of new HES Complex jobs was actually almost double the net jobs gain of 38k for the entire nonfarm payroll!

After a few more monthly revisions and eventual re-benchmarkings, of course, that number will be significantly reduced. Yet regardless of the exact magnitude of the gain, it is just plain stupid to argue that ultra low interest rates or anything else the Fed is doing has anything to do with jobs growth in the HES complex.

That’s entirely a function of the government sector’s $3.5 trillion annual funding of medical entitlements and education, including the tax-driven provision of employer funded health benefits to 160 million Americans. These programs are all on statutory auto-pilot and their huge contribution to GDP cares not a wit whether interest rates are low, high or nothing at all.

In fact, just under 9 million or 67% of the 13 million new nonfarm payroll jobs in the US economy since the turn of the century were in the HES Complex. The mad money printers at the Fed had virtually nothing to do with them.

[image]https://davidstockmanscontracorner.com/wp-content/uploads/2016/06/HES-480x299.png[/image]

So what Yellen is counting as evidence that monetary stimulus actually works is simply the cycling of part-time leisure and hospitality, retail, temp agency and other low pay jobs. These jobs rise and fall between the serial financial booms and busts which stem from the Fed’s monetary intrusions, and are evidence that it has destabilized and impaired the main street economy, not advanced it.

Indeed, you could even call it the bread and circuses economy and not be far from wrong. While jobs in bars, restaurants, hotels, sports stadiums, theme parks and the like comprise just 11% of the 143.9 million nonfarm payroll jobs reported by the BLS they accounted for 2 million or 35% of the total jobs gain since December 2007.

[image]https://davidstockmanscontracorner.com/wp-content/uploads/2016/06/breadcircus-480x303.png[/image]

Yet even the Part-Time economy is beginning to cool by the BLS’ own reckoning. The 39.946 million jobs reported for this sector in May represented zero gain from the prior month.

And it needs be recalled that these are 40% jobs in an economic sense. They average only 26 hours per week of paid work and generate annualized earnings of less than $20,000 at the $14 per hour average wage. That compares to an average of nearly $50,000 per year for full-time “breadwinner jobs”.

[image]https://davidstockmanscontracorner.com/wp-content/uploads/2016/06/pt-480x299.png[/image]

In fact, there was a 33,000 drop in the number of full-time, full-pay “breadwinner jobs” in May. That Yellen has the audacity to insist that the labor market is strengthening and then gets away with it is surely proof that the financial commentariat is drinking the Fed’s Cool-Aid in jumbo sized gulps.

Alas, they have been doing so during this entire so-called recovery. In the real world, in fact, there are still nearly 2 million fewer breadwinner jobs than there were the day Bill Clinton packed his bags to shuffle out of the White House.

[image]https://davidstockmanscontracorner.com/wp-content/uploads/2016/06/breadwinner-480x299.png[/image]

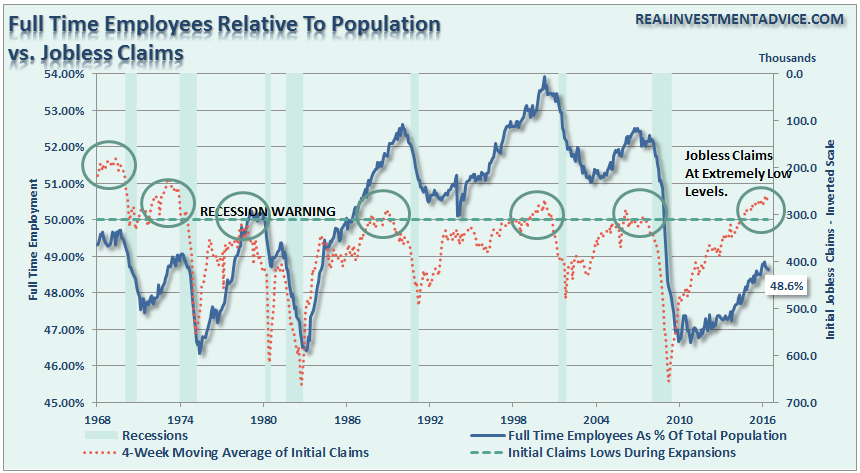

Likewise, the share of the adult population actually employed still stands at just 48.6% or at the level which prevailed way back in the early 1980’s when the female participation rate was far lower than it is today.

Yet the merry band of money printers who inhabit the Eccles Building ignore this powerful secular trend entirely. Instead, they persist in pretending they are stimulating an economic ether called “aggregate demand” when the underlying problem is self-evidently structural and unreachable with the primitive tools of central banking.

Nor is the above graph explained by the shibboleth of aging demographics among the baby-boomers. In fact, the employment-population ratio of 65 years and older persons has been steadily rising since the Great Recession.

Yet in the face of the overwhelming evidence that the nation’s stagnant economy is suffering from structural impediments and supply-side constraints, Yellen blathered on about how continued pegging of the money market rate near zero is warranted because the inflation-adjusted “neutral rate” of interest is exceedingly low.

Oh, c’mon. There is no such thing as the neutral rate of interest; it’s a completely made up construct that Keynesian economists use to justify their relentless efforts to falsify the price of money. It’s the equivalent of the parental admonition that something is valid “because I say so”.

The irony is that the only valid rate is the market rate of interest set by the demand for funds and the supply of honest savings from current household income and business cash flow. And that we most definitely do not have because the Fed says so.

So the Fed carries on with its make believe “stimulus”, assuring the sick puppies who inhabit the casino that a mythical state of “escape velocity” is just around the corner.

In the meanwhile, as Yellen made abundantly clear in today’s speech, the Fed will stand pat on the zero bound until this imaginary outcome materializes. Long before that, of course, the on-coming recession will make its appearance.

Then the casino will break into full panic upon the realization that Yellen and her posse are exactly as clueless as they sound.