Authored by Kevin Muir via The Macro Tourist blog,

I have often said that as traders, it is not our job to pass judgment on what should be, but, instead, to take advantage of what is. I will try to stick to that mantra when discussing the US tax “reform” package, but I must admit, it’s going to be tough for my feelings to not wiggle through.

Regardless of your ideological views, I think we can agree on a couple of points. First, this is not tax reform. There is no wholesale dramatic change to the tax code. Second, this is not a tax cut for lower and middle American workers, but instead a corporate and upper-class break of monster proportions. Now, you might think this is the best avenue to prosperity for all Americans, that’s certainly an argument I have heard from the right. Let’s not worry about the legitimacy of that theory - it is what it is, and arguing about it is like yelling at the clouds. Instead, let’s accept the fact that this is the direction Trump and Republicans are taking, and try to figure out what it means for the market.

This morning I called up my favourite European millennial hedge fund manager, Samuel Gruen to shoot the shit about how much of the tax cut was priced into the market. I am not sure where Sam’s ideas end and mine start, so let’s just say the next part was a collaborative effort.

I started with the proposition that much of the tax cut was built into the market, but expressed my worry that some smart excel crunching analysts were claiming the market was underestimating the tremendous impact of the corporate tax cut. Sam pointed out that if my theory was correct, then we should have seen those companies that would benefit most from the tax cut, rally the most over the past couple of months.

Yet when we have a look at the stocks that have risen the most, it’s not those stocks. The last couple of months have been a momentum chasing FANG craze. Not the companies that will benefit most from the tax cut.

And when I looked at yesterday’s action, it seems clear the market was not prepared for the tax bill progress. On news that the Senate had the votes to pass the bill, the S&P 500 exploded higher and they monkey-hammered the Nasdaq lower.

This certainly does not look like a market that had priced in a tax cut.

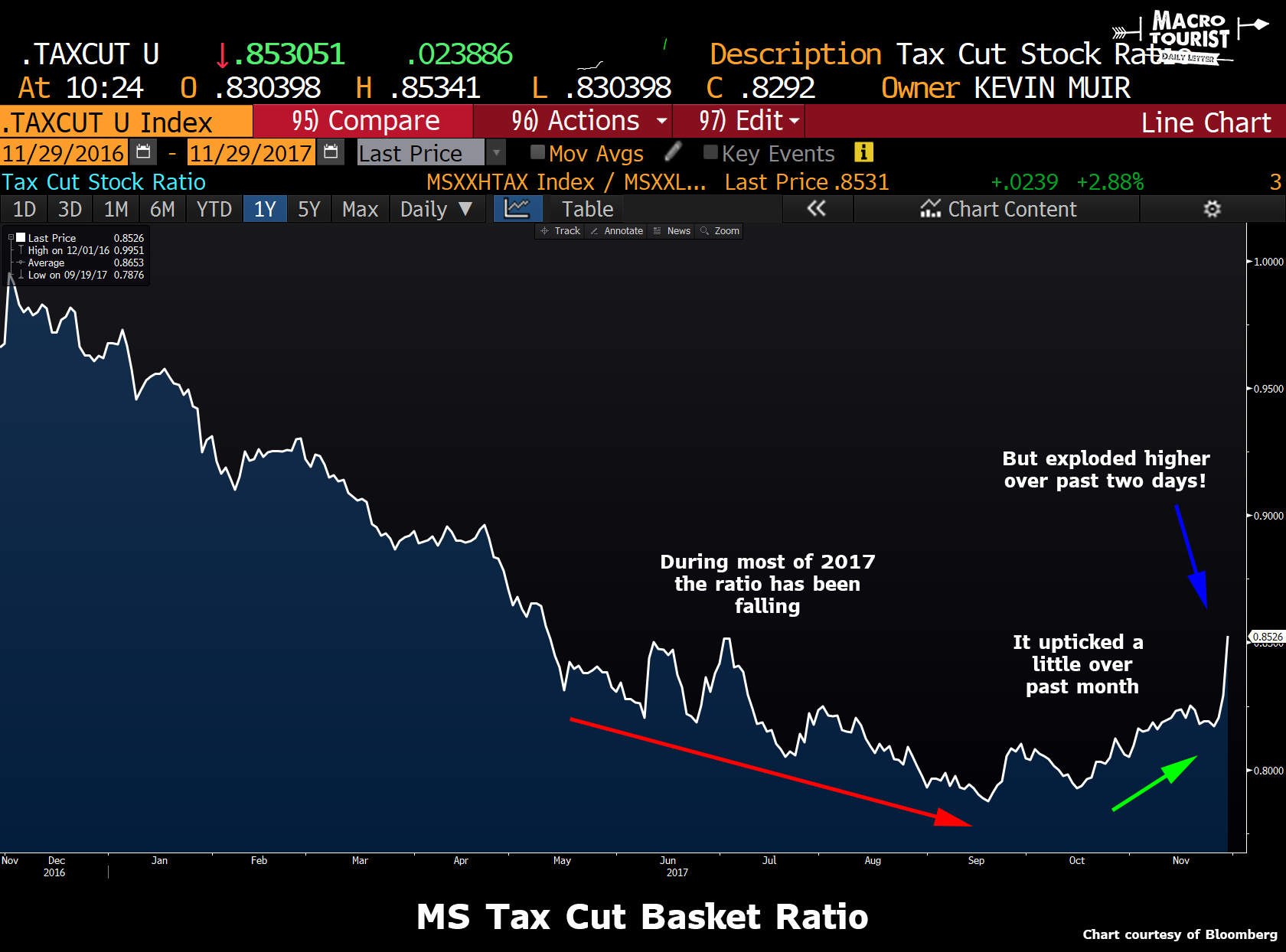

Thinking about this another way, what if we look at the basket of stocks that will benefit most from the tax cut (as compiled by Morgan Stanley), and compare that to the ones that will benefit the least?

If it was priced in, we would expect to have seen the ratio between these two baskets rising over the past couple of months.

Yet, instead, we see that during most of 2017 this ratio fell, with a minor uptick over the past month, but with an explosion higher over the last two days.

Looking at the data, it’s probably right to say that my initial feeling - that the tax cut was priced in - is most likely wrong.

But what does this mean?

Let’s assume the tax cut is not priced into the market. It certainly is behaving that way. That leaves open the next question - how to take advantage of it?

The most obvious answer is to buy the names that will benefit the most while selling those that won’t. Probably the most efficient way of doing that would be buying S&P 500 futures while shorting Nasdaq 100 futures.

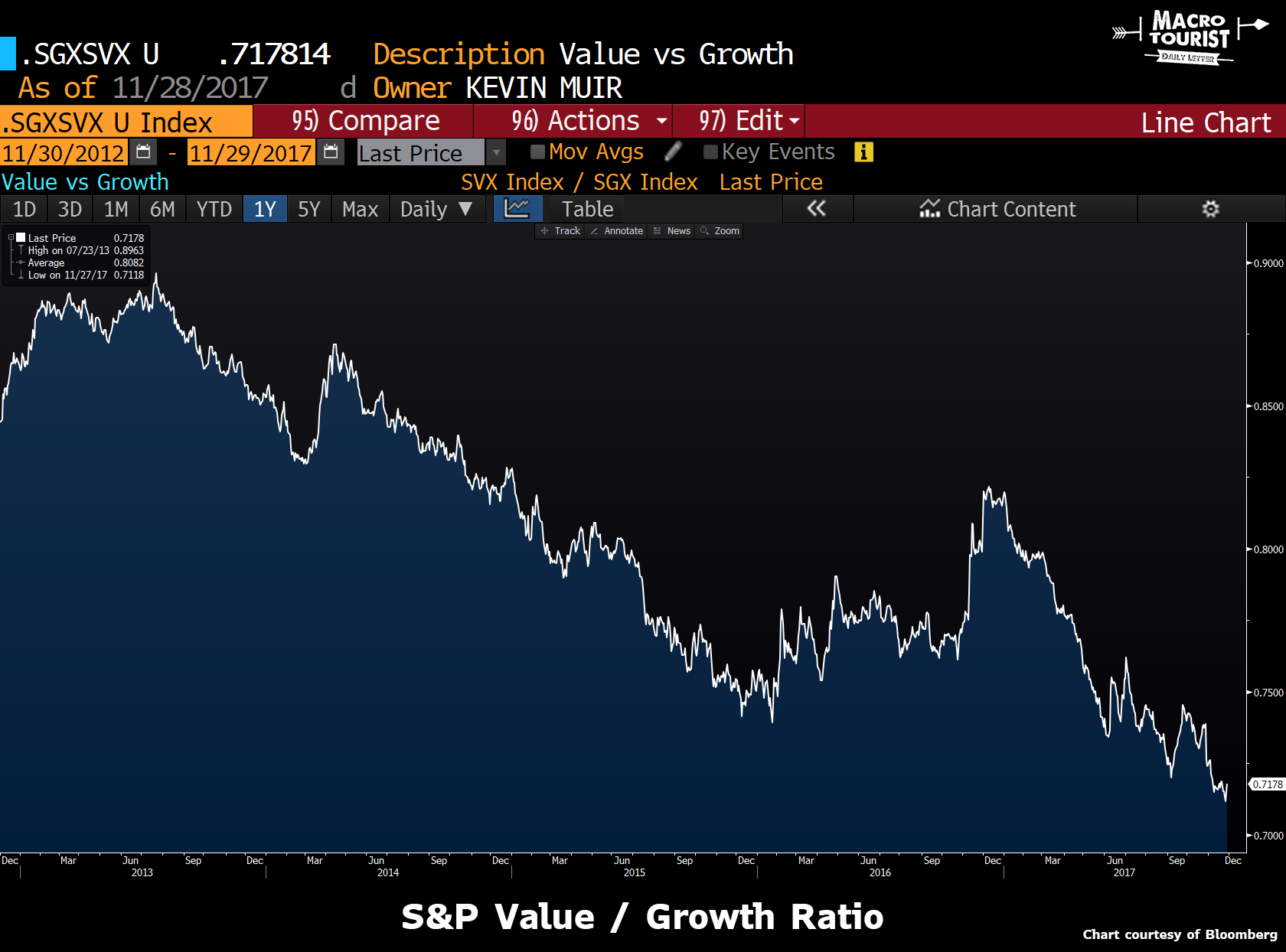

Another idea is to buy value stocks while selling your growth stocks. I have written about this previously in Value Investing Deadpool, but it’s probably all the more appropriate if the tax cut passes.

What if this is the top?

But here is another idea.

Although I agree the tax cuts are far from being priced in, what if this change causes a massive rotation out of growth and into value/financial/stocks-that-benefit-most from tax cuts, and in doing so, causes volatility to rise? If volatility rises, then for a whole host of different reasons, market participants will be forced to de-lever their stock portfolios.

I just want to get this post out there as the market is selling off hard as I write this. I know every other morning decline has been a buying opportunity. It wouldn’t be surprising if today is no different.

Yet, remember that markets top when things look best. And there can be no denying that it’s tough to imagine a better scenario for stocks than a massive corporate tax cut. It should cause a massive repricing higher in traditional-tax-paying companies. That should be insanely bullish.

But what if the trade isn’t to buy these companies, but instead to simply short the growth stocks? Don’t forget the ratio between the two different categories of stocks might correct not by the underperforming one rallying, but instead by the outperforming one finally selling off. Nah… can’t be. That would mean stocks actually going down. How stupid is that?