Authored by Kevin Muir via The Macro Tourist blog,

Remember the original widow maker macro trade?

More than a decade before short China positions filled hedge fund portfolios. Way before the long VIX trade. And before Australian and Canadian real estate was even worthy of consideration by global macro traders, there was the JGB short.

The Japanese Government Bond market was the first truly asinine Central Bank fueled bubble. Macro traders fell over themselves shorting it, hyperbolically venting about the un-sustainability of the Japanese government policy.

I won’t pretend I didn’t succumb to the romantic allure of the JGB short. It was a dark seductive mistress and as some pundits joke, you aren’t a real macro trader until you have lost money shorting JGBs.

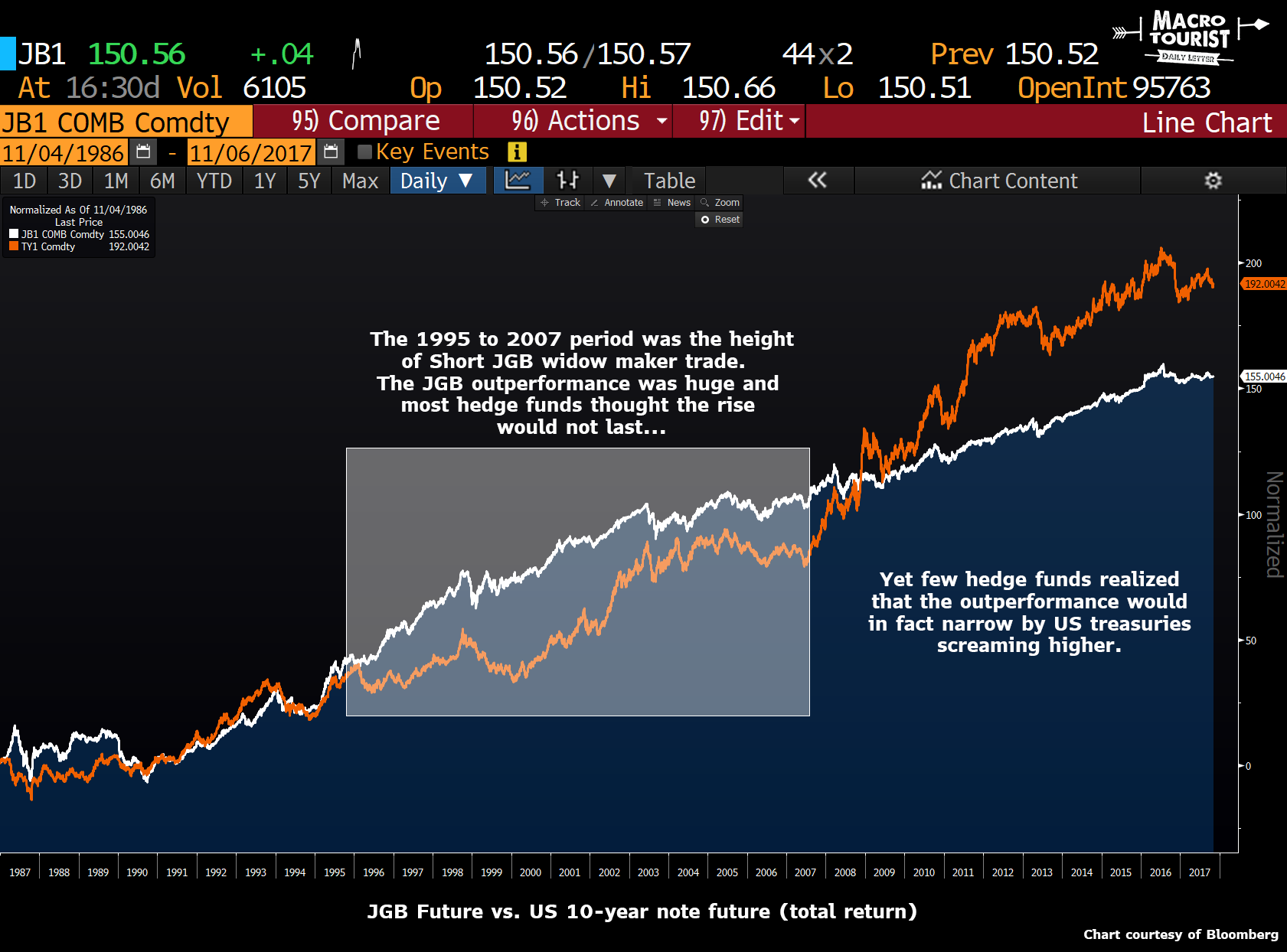

And it’s easy to see why it was such a popular trade. In 1990 the 10-year JGB yield was 8%. By 2000 it had declined all the way down to 2%. But since then, regardless of the absurd amount of debt created by the Japanese government, the yield has only fallen.

Wild, eh? And now it’s become completely farcical with the BoJ pegging the 10-year maturity to 0%.

So far this nothing new. No big revelations here.

Now if asked you what has performed better - the US 10-year note or JGBs, what would you answer? I would have said the JGBs by a long shot. After all, they have gone from 8% to 0%. During the same period, the US 10-year yield went from 9% to 2.3%, so it would make sense that JGBs have outperformed.

For a long time, this analysis was spot on correct. Right until the Great Financial Crisis of 2007, the JGBs outperformed by a long shot.

Yet instead of this relative outperformance narrowing by JGBs collapsing, the opposite occurred. US treasuries screamed higher.

I must admit I was quite surprised learning how much US treasuries have beaten JGBs over the past decade. But when you look at the yield chart it becomes obvious. JGBs have been yielding next to nothing for quite some time. So the reality is that all the capital appreciation has gone. Meanwhile, the US 10-year note has been quietly clipping a coupon of at least 2%.

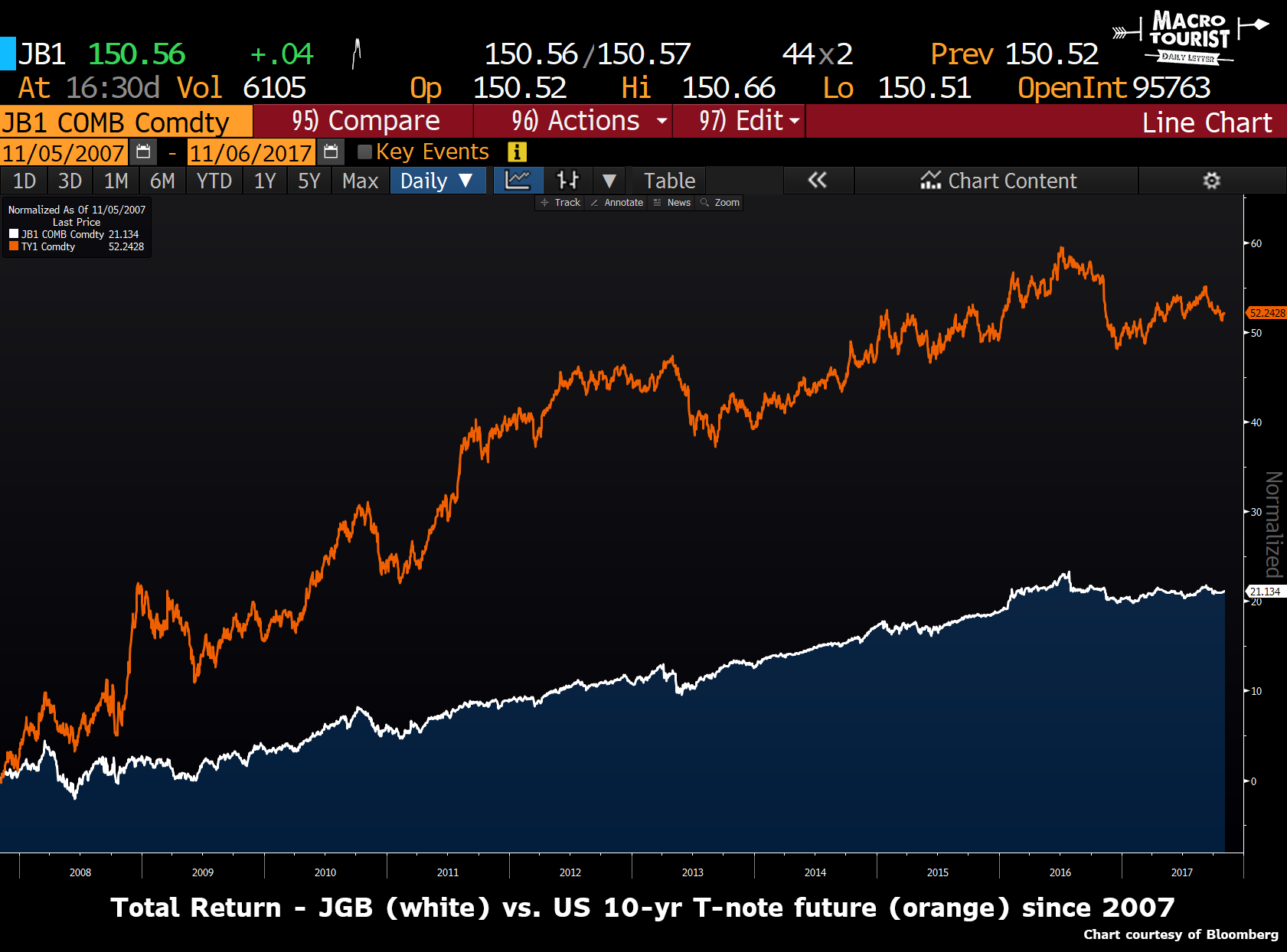

If you look at this same chart since the GFC, it becomes even more pronounced.

The total return of the JGB future is just a shade over 20%. Meanwhile, the US t-note has returned more than 50%.

Maybe the JGB short sellers can make a comeback?

Now I can already hear all the pushback. The JGB is not a real market anymore. There is no volume. Price is basically set by the BoJ. Yeah, yeah, I get it. I know all the arguments.

But here is my thought. If we assume that rates cannot go significantly negative, and I realize that is an assumption, not a given, then shorting the JGB market is much cheaper than the US. If you are a big inflationary secular bull, then finding the cheapest place to hide while you await your thesis to play out is important.

I realize the BoJ might not let 10-year rates come unglued. They might just keep the peg forever. Yeah sure. Let’s say global inflation somehow miraculously picks up to 4%. Nothing extreme, but way above Central Banks target. And yet, the BoJ tries to keep the peg. Well, that means they will be giving up control of their money supply. You can control the price or the quantity, but not both.

With the peg still in place, yen would be created in insane size. Ultimately it would create a self-reinforcing inflationary feedback loop.

You might say - but the Japanese government cannot afford to have rising rates. Yup, can’t say I disagree there. That’s why they will leave short rates low and be reluctant to allow them to rise significantly. But the long end, that’s set by the market. Or at least it used to be set by the market. And if the Japanese government doesn’t allow it to be set by the market, that will mean a crazy inflationary yen collapse. So I don’t buy that the JGB will be pegged to zero forever.

The takeaway is to be careful buying fixed income markets with no yield

Ok, so maybe you don’t buy the argument that shorting JGBs might be a good idea. I get it. It’s difficult embracing a trade that has lost so much money for so long for so many. Yet I think the risk reward is skewed towards the short making sense. Sure the chances of the trade working might not be high, but the probability of the trade hurting you in a big way is also low. The carry is so minuscule, the downside to your P&L is limited. Zero percent is probably a floor, so if I am wrong and the peg remains forever, you just lose your tiny carry.

But the real lesson is that once the coupon gets low, the ability to continue making outsized total returns is limited. I know that seems self-evident, yet sometimes I wonder.

Think about that when you are buying German 10-year yields at 0.35%. Your margin for error is small. And on the flip side, when the US 10-year is one of the highest yielding developed market bonds, and almost 2% higher than German yields, the carry of that extra coupon adds up. Just glance back up to the total return chart of JGBs versus T-notes. It’s been a while since Japan has been the best performing bond market.