Authored by Kevin Muir via The Macro Tourist blog,

I haven’t written about it much, but I have long been a closet uranium bull. Yeah, maybe I wrote one piece - Somewhere Cheap to Hide, but it’s not like I have been pounding the table on the idea.

Although it has been obvious for everyone to see that the industry could not continue operating with the price of the commodity trading below the cost of production, the problem has been that no one wanted to cut. So even though it was illogical, everyone kept producing at negative cash flows, desperately hoping the other guy would tap out first. In the meantime, the price of the commodity, and by extension, uranium producers’ stock prices, kept sagging.

And why buy the stock of some negative cash flowing uranium company when the FANG stocks were ripping higher a couple of percent every day? So investors have continued to ignore these dirt cheap uranium names.

But their negligence will be our gain. Take the time to read my piece linked above. All the arguments still apply, the only thing we have been missing is a catalyst.

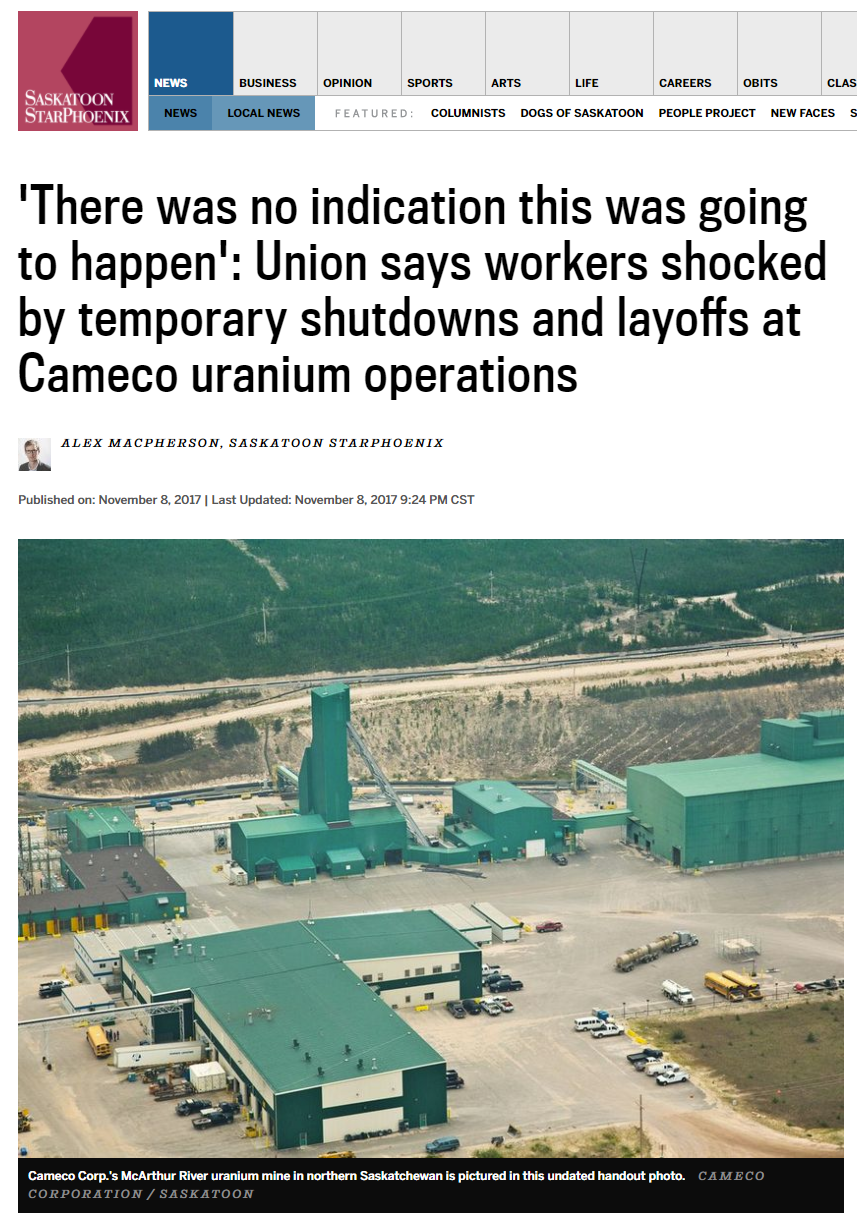

Well, guess what happened last night? Cameco finally cried Uncle. Although it is sad for the workers, Cameco took a giant step towards bringing the uranium market back into balance with the shutting down of two of their northern Saskatchewan mines. From the Saskatoon StarPhoenix:

Cameco Corp.’s decision to temporarily shut down two uranium operations in northern Saskatchewan, leaving around 845 people without work for at least 10 months, is shocking, according to the head of the union representing the company’s employees.

The Saskatoon-based company attributed its decision to stop production at the McArthur River mine and Key Lake mill to “unsustainably” low prices, but United Steelworkers Local 8914 interim president Denis O’Hara said workers were blindsided.

“Employees on site would be in total shock as well, because there was no indication that this was going to happen, especially to the extent of 10 months,” O’Hara said, adding that the two facilities 550 kilometres north of Saskatoon spent much of the summer shut down.

Cameco told its employees late Wednesday afternoon that 210 workers will be retained once the mine and mill are in a “safe shutdown state” by the end of January, but additional temporary layoffs could follow as it reviews corporate support for the idled operations.

“There’s just today too much uranium out there,” Cameco President and CEO Tim Gitzel said in an interview Wednesday evening, hours after what he described as “sombre” meetings at the two affected sites.

“We didn’t think adding to that was helpful. We have a good inventory of uranium at Cameco that can sustain us that we can put into profitable contracts… We can actually buy uranium cheaper than we can produce it.”

Stop and read that last quote again. “We can actually buy uranium cheaper than we can produce it.” That’s the sort of Graham-Dodd deep value play that has been so unbelievably difficult to find since the advent of worldwide quantitative easing. Yet, here it is, lying right in front of us. Yeah, it’s an ugly industry, with terrible looking fundamentals - but that’s why it is SO CHEAP. If it wasn’t scary looking, it wouldn’t be an opportunity.

I want to get today’s post out before the open, so I am going to rely on some other people to make the rest of my point for me.

Let’s start with my mysterious uranium mine owning pal who I referenced in my previous article. When this news hit last night, I sent him a note to ask his opinion.

If there is not already an acronym called BUTT (…back up the truck…) then this is certainly an opportune time to introduce it. Imagine OPEC saying we decided to take 15 million BOP off the table - and could actually do it! It’s funny because all of that stuff I wrote you a few months back is probably pretty accurate but you get more cautious as the pain goes on.

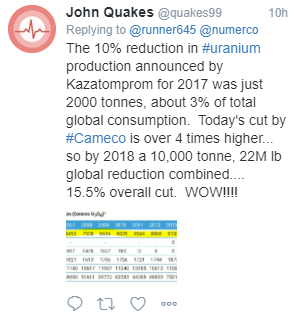

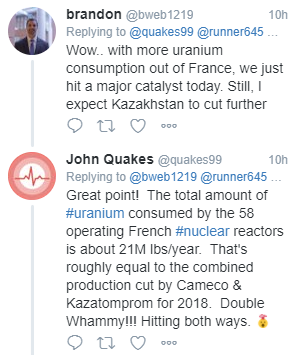

To get a sense of the extent of these cuts, I have started following John Quakes who describes himself as a “retired earth science researcher, professor, analyst, writer, trekker, and explorer. Investing now in imminent uranium bull market.” John has posted some terrific data, and for those who want to know more about uranium, I highly suggest you give him a follow. Here’s some of his quality posts:

It’s obvious that those who really understand the uranium industry view this Cameco announcement as a BIG DEAL. We are going to rip higher on the open, but it might be one of those situations where you have to bite your lip and buy it anyway.

How to play it

The go-to instrument for most uranium bulls is the Global X Uranium ETF - symbol URA.

After a brief period of excitement following Trump’s election where the ETF rallied 50% in a heartbeat, it has since sagged back down the lows.

With this new supply development, we could easily follow the same sort of rally. It wouldn’t surprise me at all to see this ETF pushing back up to $20 in the coming months.

Personally, I also like owning the actual commodity. Spot uranium is trading at a wicked discount to the forward swap contracts, so in my mind, I am buying an asset for cents on the dollar. Now you can’t just run out and buy uranium (remember all the problems Doc Brown had securing his supply), so I prefer the Uranium Participation Closed End Fund (U CN Equity):

Either way, the mistake will be to sell too soon.

Longer term picture

A couple of months back, my uranium mine owning pal sent me this long note sketching out his thoughts about the industry. I had been keeping it in reserve, waiting for the technical situation to change in the uranium market before publishing this piece. Well, the time is here, so I am including his thoughts from earlier in the summer:

In addition to the positives regarding Kazahk supply and the Paladin Energy denouement that we already touched on earlier, you can see from the tenor of the articles that growth is still ongoing in nuclear with China going gangbusters and the US turning at least neutral, if not actually cheerleading. The U price rally we had earlier this year was, in my mind, a result of the supply side of the equation having done its bit to restore balance to the market. This included the big players like Cameco and the Kazahks. The market (ie the equity market) liked this because it’s sort of Economics 101 in the free market playbook and, as you noted in the previous piece, it seems irrational and unsustainable when even the lowest cost guys in a market cannot make any money.

It would also seem short sighted in an industry where security of supply should be at least a medium term concern and where vertical integration would not be an illogical strategy that the users of uranium (ie the utilities) would not be at least a little interested in the health of the production base. However, this has really never been the case - at least for the last 35 or so years - and the reason for that is that during most of this period it has been a buyer’s market punctuated only by short spikes (like 1996-7 and 2005-7) where supply and price concerns were hot button topics. Abundant secondary supplies played a huge role in this as did the proliferation of potential supply when these concerns surfaced (…to whit, we went from under ten U companies in 2003 to over 700 in 2007…). Capitalism seemed to work and there seemed to be lots of future projects if required in the longer term buffered by the view that governments would help if need be in the interim with stockpiles.

This continues to be the thinking of the western utilities today and for now you cannot fault them for pursuing a strategy that is working. If you are a nuclear fuel buyer for a capitalist or western world utility, you do not earn your annual bonus for visionary thinking about security of supply or “buying low” but you could face job insecurity if you are out of whack with the herd. Think mutual fund managers and closet indexing and it’s the same phenomena.

The new factor in the market now - and I have included a number of articles that are on point - is that the demand side is now part of the industry’s price problem with the commitment to nuclear of stalwart countries Korea and France being called into question. This follows the Germans, Swiss etc where the optics are all that somehow nuclear is a sunset industry post Fukushima and with the rise of renewables. Forget the fact that even if countries like Korea can ‘phase out’ nuclear, they own plants with multi decade lives and they will have significant demand for uranium for long after an iconic mine like Cigar Lake will be exhausted (which is 2027 according to its owners). So you essentially have a lot of bad branding and headline risk because all of the good news is in places like China, Russia, India, and the UAE and all of the bad news (or apparent bad news) is in places in the comfort zone of coverage for western media. That same media has also fully embraced Climate Change and our EV future so in places like Ontario you don’t read much about how we actually keep the lights on or, if you do, you get a bit of a distorted view.

I am a big fan of the Gridwatch site (and their app) which shows you power generation and sources in virtual real time (see attached). There is no editorial bias in this as it’s just data. So this afternoon, as happens on most days, almost all of our power here in Ontario is from baseload nuclear and hydro with solar making a diminimus contribution as usual. However, if we tracked media coverage or spin from politicians, my guess is the coverage ratio would be reversed with 90% devoted to solar, renewables, Elon Musk etc. The politicians in western countries have by and large fully drunk the Kool-Aid so maybe the inflection point for all of this will happen when there are actual political consequences for bad energy policy decision making. I think we are close to seeing this in Australia as energy is a huge hot button issue there right now and likely will be front and center in the next Federal election.

The epicenter though may be the Aussie State of South Australia (home of the huge Olympic Dam copper-uranium mine) where the lights actually did go out for days recently due to dumb green energy targets that saw the backup coal generation permanently closed. It’s a left-leaning State though so their solution was double down on stuff that wasn’t working and call Elon who is going to build them a big giant back-up battery in 100 days or it’s supposedly free. The contrarian in me says we could be approaching Peak Musk / Tesla but we’ll know soon enough. Maybe it will also mark the bottom in nuclear as industry sentiment is as poor as I have ever seen it with most of us in that Don Coxe place where we are not sure if it will ever turn.

Kazatomprom and Cameco team up?

And even before that note, one of my readers asked what my pal thought about the rumours surrounding Kazatomprom’s managing of supply. He responded:

He is right on the money there and perceptive as to what the rumblings from Kazatomprom will do if implemented. These moves are not secret - for example, they spoke at a Toronto conference in April on this topic, albeit a bit vaguely - . and they have initiated moves to make this happen on the marketing side beginning next year so that they just don’t sell everything spot. This was apparently legislatively required until now.

This is part of a bigger plan whereby Kazatomprom will either IPO or have some public visibility next year. Unlike Aramco or OPEC, the Kazahks could create a meaningful cartel with the tacit assistance from a couple of other real players - say Cameco - so the bet would be that U prices won’t be $20/lb when this happens. They are the 800 pound gorilla on the supply side at the moment and have been overproducing into a market that was oversupplied.

A bull story that is not reliant on QE

Add all of this together, and for me, I get a bull story that is not reliant on every increasing liquidity from Central Bank quantitative easing programs. This is an honest to goodness cheap asset that finally has a catalyst. Call me naive to believe the market will finally appreciate this sort of play.

* * *

Japanese Nikkei ominious price action

Quick note to highlight last night’s Japanese Nikkei stock market action. When I went to bed, the Nikkei futures were screaming higher, ticking up 2%. When I woke up, the rally had collapsed and the stocks closed on the lows.

I have been a big Japanese Nikkei bull, but this is OMINOUS price action. Time to head to the sidelines…

I have to wonder, did the BoJ finally run out of blue tickets?