With The Fed definitely off the table, China promising nothing but daily liquidity drips, and Europe unable to do anything but jawbone, the world's bullish equity market investors are anxiously trawling for a central bank to save the world. Tonight's BoJ meeting could well be it - though judging by their past epic failures - it will be anything but successful as QE23 looms in Japan. “The need for a Kuroda bazooka is increasing,” said Yuji Shimanaka, an economist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo. “This is decision time for Kuroda” as additional stimulus can stop the trend of yen gains and falling stocks.

Market participants’ views on the BOJ are mixed, but leaning increasingly toward more stimulus as Japan’s growth is sputtering and inflation, at 0.3% year on year as of November, is way below the BOJ’s 2% target.

Weak exports, production and stagnant consumption weighed on growth in the fourth quarter. Despite a negative month-on-month reading for Japan’s industrial output in November, production still may have expanded in the fourth quarter, though likely not enough to offset a 1.2% drop in the third quarter. Companies’ production plans signal that the outlook for a stronger first quarter remain.

However, just as wih The Fed, despite uninspiring growth data, positive dynamics in the labor market -- the basis for the BOJ’s optimism on the price outlook -- remain in place.

Given Kuroda’s history of surprising observers, the spectrum of potential outcomes is very broad. As Bloomberg reports,

While only six of 42 economists surveyed by Bloomberg are predicting that Kuroda’s board will expand already-record stimulus this time, others didn’t rule that out. Twenty-nine expect further easing by mid-year. Citigroup Inc., JPMorgan Chase & Co. and UBS Group AG economists are among those giving additional stimulus at this meeting a more than 30 percent chance.

Since the BOJ’s last meeting in December, oil prices fell to a 13-year low, the yen touched a one-year high, stocks have tumbled about 10 percent this year and the outlook for faster wage growth has waned.

All of these things are obstacles to the BOJ hitting the 2 percent inflation target by its goal of around the six months through March 2017. The bank could announce a change to the timing of the target Friday.

And one possible wild card: If stimulus isn’t expanded, look for language that hints at the potential for an unscheduled policy move ahead of the next meeting, which won’t be until March 14-15. The BOJ has a new schedule for 2016, and no longer has a February meeting.

Friday’s meeting is the first at which the board will release the outlook report at the same time as the policy decision, which could delay the release past the typical window of between noon and 12:30 p.m. in Tokyo. Later decisions in the past were often associated with policy shifts, but that may not be the case this time.

If the board stands pat, observers would expect the yen to climb and Japanese stocks to tumble in the immediate reaction.

But that could shift, if the BOJ signals it will be watching financial markets continuously for signs of damage to the domestic outlook and will be ready to act at any time. Kuroda could emphasize that message in his 3:30 p.m. press conference -- though that would be after the close of stock trading in Tokyo.

“The need for a Kuroda bazooka is increasing,” said Yuji Shimanaka, an economist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo. “This is decision time for Kuroda” as additional stimulus can stop the trend of yen gains and falling stocks.

Whether the BOJ pushes back the timing of reaching the 2 percent price target and if so by how much will be a key gauge to assess BOJ’s optimism or pessimism.

The BOJ now forecasts hitting the inflation target around the six months through March 2017. People familiar with discussions at the BOJ told Bloomberg last week that they are considering a delay in the schedule for a third time in less than a year.

If the target is postponed to some time in fiscal 2017, that points to an increasing risk for not achieving it by the end of Kuroda’s term in April 2018, according to Hideo Hayakawa, a former BOJ chief economist. If the inflation target holds firm without further stimulus, that will be an indication that Kuroda remains more optimistic than most.

The key is how Kuroda views the impact of the recent moves in the yen and Japanese stocks, along with concerns about China’s slowdown on Japan’s inflation expectations and corporate investment and wage plans. The economy is growing at about its potential, so it comes down to assessing confidence and whether he thinks a move Friday would strengthen sentiment.

The BOJ also will update its forecasts for economic growth and prices for the first time since October. Hayakawa forecast that the bank will cut the inflation projection to about 1 percent for the year starting in April from 1.4 percent.

The big question though, as Bloomberg notes, is Will Kuroda Adopt Draghi-Style Communication?

Masaaki Kanno, the chief Japan economist at JPMorgan, and UBS’s Daiju Aoki say Kuroda may indicate further easing is coming soon as European Central Bank President Mario Draghi did last week. Also, the Fed added a line in its statement this week to say it’s closely monitoring global economic and financial developments.

By adopting the Draghi style, Kuroda could avoid disappointing the markets and buy some time as he examines the impact of stock and yen turbulence on Japan’s economy.

However, given the market's lackluster response to Draghi's promise, it appears markets are demanding action not words.

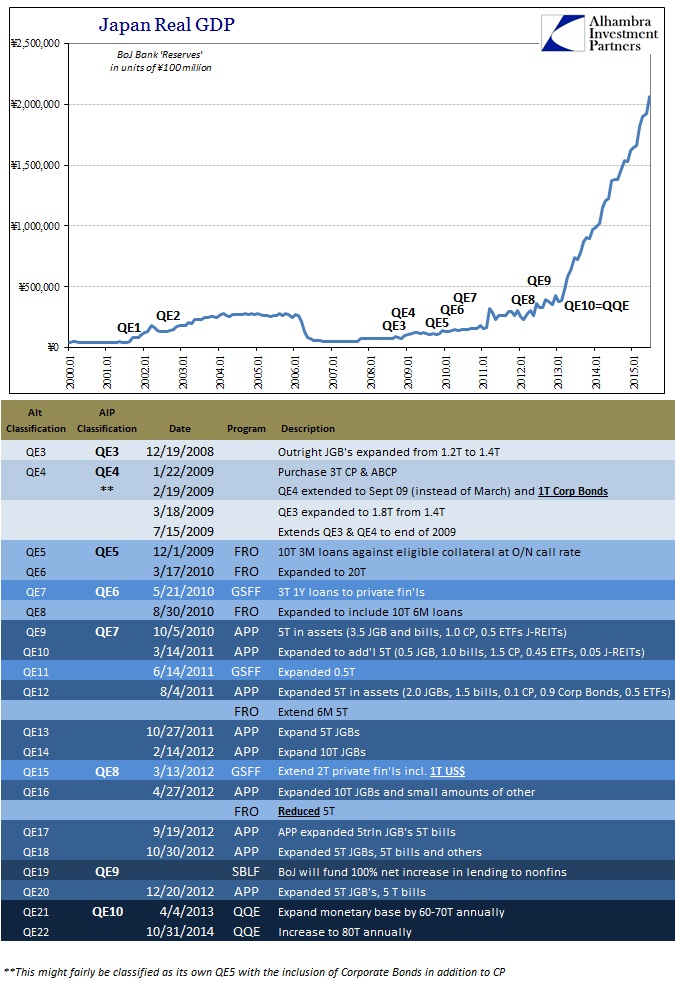

But even actions have not helped, as Alhambra's Jeff Snider previously noted, there is scarcely a block of the calendar since the “impossible” global panic in 2008 that hasn’t seen any of them doing something to expand their balance sheet or impress the “time-axis.”

By my more conservative count, qualified as the BoJ doing something different rather than purely expanding or extending something already in progress, there have been 10 QE’s in Japan but using the numerical standard which has been applied to the Federal Reserve there may have been as many as 22 or more.

This is not so much investing or even finance as it is a cult (calling it a religion or even ideology is unjustifiably too charitable). That is the usefulness of “deflationary mindset” not so much as a matter of actual economic pathology but as a built-in, squishy appeal to “we’ll get it right next time.” And there is always, always a next time which doesn’t seem to count for much inside the cult when, in fact, it is everything.

* * *

But still investors await tonight's BoJ statement for any buying opportunity because this is the farce that the new normal has become.