Submitted by Charles Hugh-Smith of OfTwoMinds blog,

The key take-away: focus on owning income-producing assets, not a primary residence.

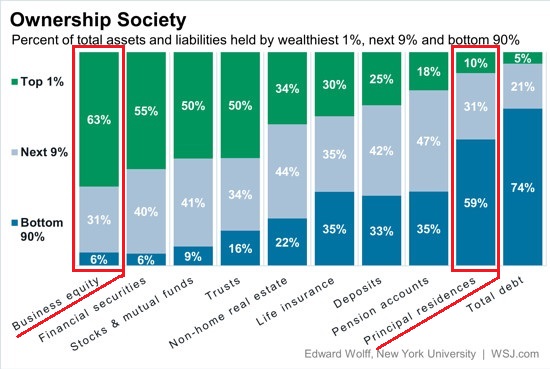

One truism of investing is to follow the lead of those who are building wealth. This chart reveals the foundation of the wealth of the top 1% and the next 9%; business equity, i.e. ownership of enterprises. Compare the assets boxed in red:

The wealthiest households' primary wealth is businesses and shares in businesses. The bottom 90% depend on the family residence as a store of wealth, and on debt as a means of funding asset purchases and consumption.

Primary residences were once a reliable store of wealth--a store that was accessible to working families who were willing to pinch pennies and save up a down payment.

But now that housing has been financialized and globalized, it is prone to boom and bust cycles like every other risk-on financialized asset. Unfortunately, recent history shows that many middle-class households bought homes at the top and rode the post-bubble burst down.

Those fortunate enough to own homes in bubble-prone regions may benefit from speculating in housing, but playing this speculative game requires cashing out at the top of the bubble--something few have the knack for.

Building a profitable business isn't easy. That's why many of the wealthy let entrepreneurs take the risk of starting businesses and then buy the business for a premium once it has proven to be profitable.

But many entrepreneurs refuse to sell out, preferring to hold their businesses as a family asset that can be passed on to the next generation.

It's also worth noting that the wealthiest 10% own over 90% of the securities and stocks, 84% of trusts (essentially tax havens) and almost 80% of non-home real estate (i.e. second homes and income-generating properties).

Primary residences represent a mere 10% of the wealthiest 1%'s assets.

The key take-away: focus on owning income-producing assets, not a primary residence. The second key take-away:

Don't finance your assets with debt; finance your income-producing assets with savings and sweat equity, not borrowed money.

It is not accidental that the wealthiest 1% hold very modest levels of debt.