Submitted by Mike Krieger via Liberty Blitzkrieg blog,

It appears the music may have finally stopped for one of the world’s largest luxury real estate bubbles: London.

It’s well known that foreign oligarchs love London real estate as a means to launder funds, typically “earned” by soaking their host countries dry via corruption and fraud. This has caused absurd and irrational spikes in high-end residential real estate in the English capital, as well as a flood of new construction.

With emerging markets now completely collapsing, the seemingly endless flood of foreign money is drying up, and with it, London real estate.

So has the London real estate bubble popped? Probably.

– From the September 9, 2015 article: Luxury London Home Sales Plunge 26% – Has this Mega Real Estate Bubble Finally Burst?

The first real signs that the global luxury home price bubble had popped emerged last fall in the world’s capital of oligarch money laundering: London.

Since then, we have seen weakness in high end Manhattan real estate, but the trend has now spread and is starting to make itself apparent all over the place.

Yesterday’s Bloomberg article titled,The Surge in U.S. Mansion Prices Is Now Over, is really interesting. Here are a few choice excerpts:

The six-bedroom mansion in the shadow of Southern California’s Sierra Madre Mountains has lime trees and a swimming pool, tennis courts and a sauna — the kind of place that would have sold quickly just a year ago, according to real estate agent Kanney Zhang.

Not now.

Zhang is shopping it for a discounted $3.68 million, but nobody’s biting. Her clients, a couple from China, are getting anxious. They’re the kind of well-heeled international investors who fueled a four-year luxury real estate boom that helped pull America out of its worst housing slump since the 1930s. Now the couple is reeling from the selloff in the Chinese stock market and looking to raise cash to shore up finances.

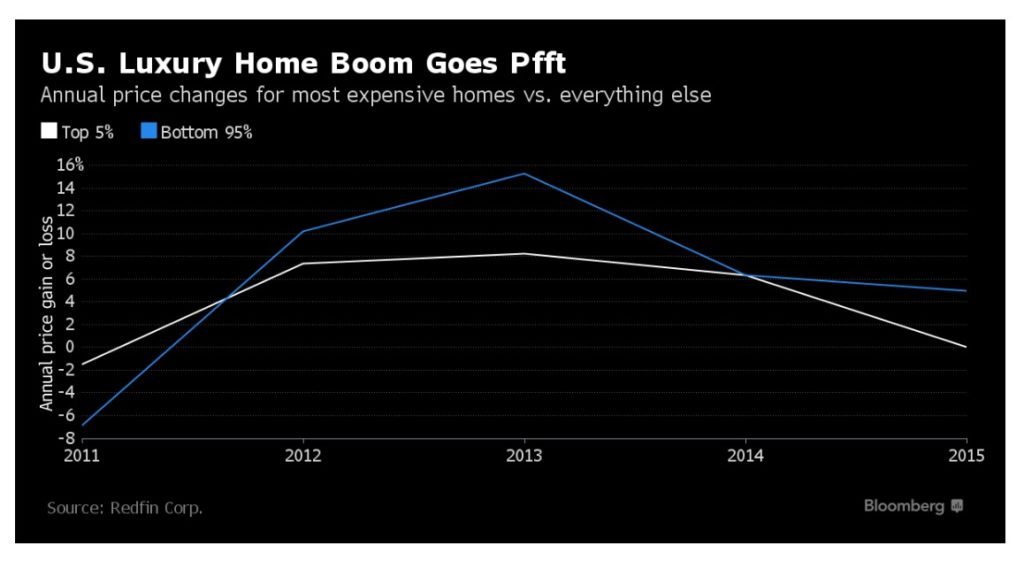

Prices for the top 5 percent of U.S. real estate transactions remained flat in 2015 while all other houses gained 4.9 percent, according to data from Redfin Corp., a real estate brokerage and data provider.

Pretty powerful chart:

In the Los Angeles suburb of Arcadia, where Zhang is struggling to sell the six-bedroom home, dozens of aging ranch houses were demolished to make way for 38 mansions built with Chinese buyers in mind. They have manicured lawns and wok kitchens and are priced as high as $12 million. Many of them sit empty because the prices are out of the range of most domestic buyers, said Re/Max broker Rudy Kusuma, who blames a crackdown by the Chinese on large sums leaving the country.

Arcadia…where have we heard that before. Oh yeah: Welcome to Arcadia – The California Suburb Where Wealthy Chinese Criminals are Building Mansions to Stash Cash

The stronger dollar is driving South American buyers away from the 23,000 condos in the pipeline for Miami’s downtown area, said Peter Zalewski, owner of South Florida development tracker CraneSpotters.com. Buyers signed about one-fourth fewer pre-construction contracts last year than in 2014, according to Anthony M. Graziano, senior managing director at Integra Realty Resources Inc., which tracks condo data for the Miami Downtown Development Authority.

In nearby Sunny Isles, Florida, faraway currency fluctuations are endangering the sale of a $3.7 million condominium. A Colombian woman who put down a 50 percent deposit is fretting over how she’ll cover the other half over the next year, said her agent, Mauricio Rojas. The Colombian peso, dragged down by the commodity slump, has lost about 30 percent of its value since she signed the contract in December 2014.

In Houston, the plunge in oil prices to a 12-year low is killing the luxury boom. Sales for homes priced at $500,000 or more dropped 17 percent in December from a year earlier, according to the Houston Association of Realtors.

Manhattan resale prices for the top 20 percent of the market peaked in February and have fallen every month since, according to an analysis through October by listings website StreetEasy.

I covered the emerging weakness in Manhattan a couple of weeks ago.

See: Manhattan Luxury Real Estate Peaked Last February – Prices Now Down 8 Months in a Row.

The economic turmoil, along with new regulations, slowed demand around the world. In London, the market weakened after the government increased a stamp-duty sales tax and Russians and Chinese buyers began pulling back. Luxury prices in London rose only 1 percent last year after jumping 5.1 percent in 2014, according to Knight Frank research.

Here are three previously published articles on London:

Tens of Thousands of Properties to Be “Dumped” on London Real Estate Market by 2017

Luxury London Real Estate Prices Plunge 11.5% Year-Over-Year

Luxury London Home Sales Plunge 26% – Has this Mega Real Estate Bubble Finally Burst?

Considering the global luxury real estate market is one of the most inflated asset bubbles on earth, current weakness could pretty quickly turn into a crash.