- CNN reports the US running out of space to store oil.

- At the same time, OPEC actually ramps up oil production...

Many "smart guys" allege that the drop in oil is bad for the ecomomy. I call BS. Oil prices are an input costs. Input costs are what strip revenues down to profits and potentially losses. The lower the input cost, the higher profit. What has occured was a decades long credit bubble that fueld a profligate binging on debt.

It is hard to get off of that drug called free money, particuarly as your dope pusher (those that push rates outside of market force bounds) continues to give you more of that smack. The problem is, eventually, it will catch up to you. The Central Banks have signaled higher rates, and have raised rates 25 bp (roughly 2% of retracement - whoo hoo!).

The market (well, the fed funds rates futures, not the market per se) is quite skeptical on the Fed raising rates any time soon. So am I, as you have seen above.

Alas, as rates scrape against the zero barrier for sometime now, and break through towards negative, the party is over and the punchbowl is being removed by the grownups, aka the natural market forces. The Financial Times reports:

The sharp drop in commodity prices and a rising expectation of defaults by highly indebted companies have shaken investors and closed the door on new debt sales. Investors say the dearth of liquidity has made it even more difficult to own paper rated triple C. Late last year several bond funds closed that held high amounts of low-rated and unrated debt.

“You are seeing a lack of appetite in the new issue market for these types of issuers,” said Matthew Mish, credit strategist with UBS. “[Funds] have outflows and the Federal Reserve is no longer printing money.

Portfolio managers are also experiencing a wave of redemptions from investors. US junk bond mutual and exchange traded funds have counted more than $20bn of withdrawals since mid-November, according to Lipper.

You know what that means. Those oil producers with higher than OPEC costs and high yield debt financing are GUARANTEED to meltdown as oil drops below their breakeven costs (I'd wager somewhere around $50 - $60/bbl if I was a betting man), and stays there. Recent financial reporting seems to corroborate this hunch...

“We expect a shakeout this year in the US oil and gas market, as highly leveraged companies will be forced to declare bankruptcy,” said Bronka Rzepkowski, an economist with Oxford Economics.

A Q&A: Using Veritaseum to take positiions in energy companies through multiple markets. Please be aware that Veritaseum is currently in beta, and the current Java client will be deprecated in lieu of a ubiquitous HTML5 client by the end of the quarter. The info below is for illustrative purposes only.

-

How do I enter the trade via Veritaseum? Am I using the web client? My own client that consumes Veritaseum APIs? Place the trade over the phone / fax with Veritaseum’s sales team?

-

If you are an advanced player you can simply go to our site and conduct the trade yourself using the system and/or your own network to find a counterparty.

-

As an institution, you can purchase Veritas (ex. $50,000 blocks) to redeem them for advisory services such as setting up trades and finding bespoke counterparties.

-

Large institutions with their own IT infrastructure can integrate Veritaseum into their system via API. This can also entail a Veritas purchase to assist in the integration, customizations and feature requests.

-

-

Where does the counterparty for the trade come from?

-

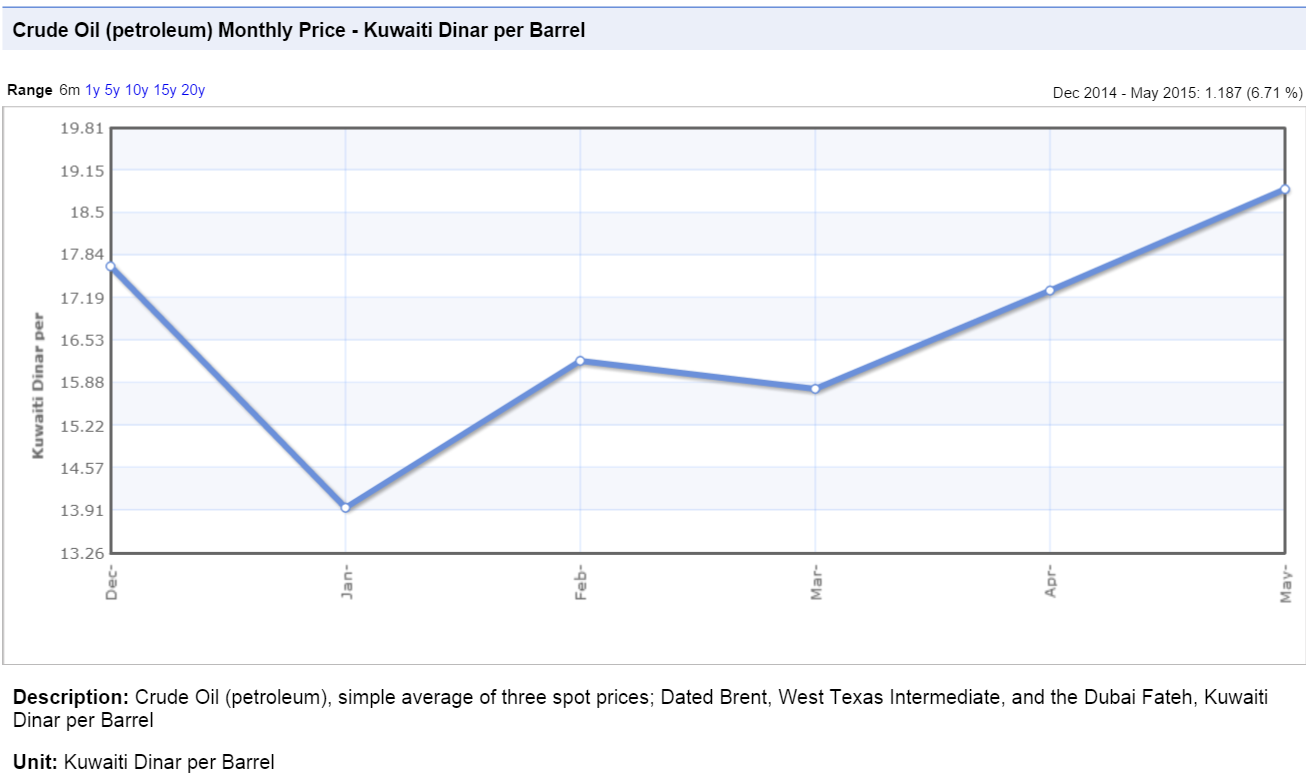

Japan is the largest consumer of Kuwaiti oil, followed by India, Singapore, and South Korea. Since Asia is such a large consumer of OPEC oil in general (and Kuwaiti oil in particular), they can be very aggressive in their purchasing terms, resulting in material concessions from the oil (and risk) producers - the most painful of which are price discounts. We can offer the oil consumers in these markets the ability to directly hedge their purchase risks - both in terms of currency and oil price fluctuation (or oil price volatility, as illustrated above) accentuating the benefits of discounts while simultaneously making discounts potentially less painful by hedging risks for the oil (risk) producers. Their (the Asian companies) purchase of said risks is the counterpart of the sale of the risk from KOC. The oil refineries of Japan, India, Singapore, and South Korea are the most likely potential counterparties but you can also include the money center banks within these countries, not not to mention the major hedge and trading funds and corporations who consume the finished product en masse. Remember, the USD component of the swap can easily be replaced with the Japanese yen, Chinese Remnibi/yuan, Indian rupee or the Korean won.

-

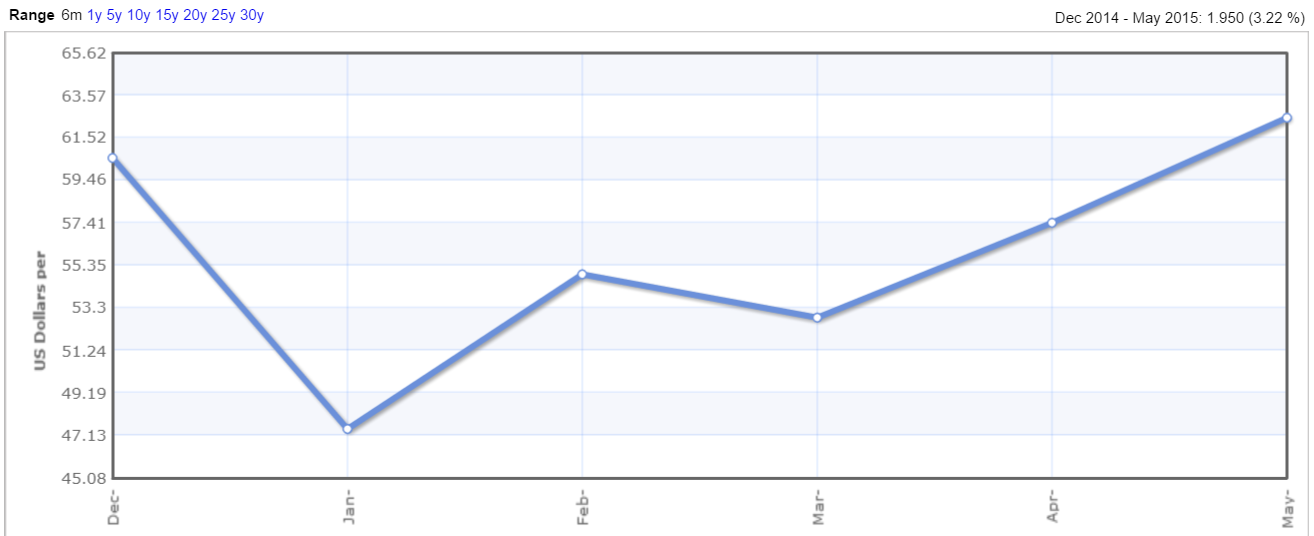

This same chart expressed in USD shows where the hedge benefits, particularly in December…

-

Who are the specific counterparties (consumers) of OPEC (producer, of which Kuwait is a major member) oil risk?

-

A joint venture between PetroChina Co. (Chinese), Aramco (Saudi Arabian) and Yunnan Yuntianhua Co. (Chinese) is currently building a 260,000 barrel-a-day refinery in the southwest of the Asian nation.

-

Aramco already manages a 280,000 barrel-a-day refinery and petrochemical complex in China’s Fujian province along with China Petroleum & Chemical Corp., known as Sinopec, and Exxon Mobil Corp.

China is the largest oil consumer after the U.S.

-

IF you are interested in finding about more about this new way of accessing exposure and laying off risk, read the Pathogenic Finance research report, then contact me at reggie AT veritaseum.com.

- Here are the highlights from the report in this most excellent interview with Max Keiser of RT's Kesier Report.