Submitted by Lance Roberts via RealInvestmentAdvice.com,

“Trump saves jobs in Indiana before even being President. This is how you make ‘America Great Again.”

Between promises to cut corporate taxes from 35% to 15%, reduce regulatory burdens and penalize companies who leave the U.S., markets, economists and analysts are all trying to figure out what it means. As I noted on Tuesday, the always bullish analysts are already pushing up corporate earnings to record levels while the mainstream media is fostering the idea of an economic resurgence to levels last seen during the Reagan Administration. In turn, this will result in higher inflation, higher interest rates and an end to the stagflationary environment that has gripped the economy over the last 8-years.

Well, that is what is hoped for.

I thought it might be useful to take a look at the specifics of the deal struck with Carrier and the reality of the current economic backdrop as it relates to fostering future job growth, higher wages and the avoidance of a recessionary outcome.

The Art Of The Deal

Supporters of Donald Trump have praised the president-elect for working out a deal to keep jobs at a manufacturing plant in Indiana from being moved to Mexico.

The deal with Carrier, which makes heating, air conditioning, and refrigerator parts, meant that roughly 1,000 workers will keep their jobs in Indiana. However, in exchange for keeping those jobs in Indiana, Carrier will receive $7 million in tax credits and other incentives which will ultimately be picked up by the taxpayers of Indiana. Carrier also said it will invest $16 million in its Indianapolis plant.

According to Carrier, they would have saved $65 million a year by moving operations to Mexico which begs the question of how tax credits and a company investment of $16 million will equalize the disparity of costs.

For that answer let’s go to Greg Hayes, the CEO of Carrier, who appeared on Monday’s edition of “Mad Money” with Jim Cramer. (Transcript courtesy of Business Insider)

JIM CRAMER: What’s good about Mexico? What’s good about going there? And obviously what’s good about staying here?

GREG HAYES: So what’s good about Mexico? We have a very talented workforce in Mexico. Wages are obviously significantly lower. About 80% lower on average. But absenteeism runs about 1%. Turnover runs about 2%. Very, very dedicated workforce.

JIM CRAMER: Versus America?

GREG HAYES: Much higher.

JIM CRAMER: Much higher.

GREG HAYES: Much higher. And I think that’s just part of these — the jobs, again, are not jobs on an assembly line that people really find all that attractive over the long term. Now I’ve got some very long service employees who do a wonderful job for us. And we like the fact that they’re dedicated to UTC, but I would tell you the key here, Jim, is not to be trained for the job today. Our focus is how do you train people for the jobs of tomorrow?

As I have discussed on the “Lance Roberts Show” in the past, and this is important, while foreign countries have cheaper labor (not demanding $15/hr minimum wages to flip burgers) they also have a more dedicated workforce willing to work the kind of low-skilled jobs American’s do not find attractive. To wit:

GREG HAYES: The assembly lines in Indiana — I mean, great people, great people. But the skill set to do those jobs is very different than what it takes to assemble a jet engine.

So, why did Hayes actually decide to cancel the move to Mexico?

GREG HAYES: So, there was a cost as we thought about keeping the Indiana plant open. At the same time, and I’ll tell you this because you and I, we know each other, but I was born at night but not last night. I also know that about 10% of our revenue comes from the US government. And I know that a better regulatory environment, a lower tax rate can eventually help UTC in the long run.

Offsetting Higher Costs

So, as I asked earlier, how to do you equalize the cost of saving $65 million annually by moving to Mexico in exchange for $7 million in one-time tax credit and incentives.

That is where the $16 million investment comes in.

In order to justify keeping the Indiana plant open, the company will inject $16 million to drive down the cost of production to reduce the operating gap between the US and Mexico.

GREG HAYES: Right. Well, and again, if you think about what we talked about last week, we’re going to make a $16 million investment in that factory in Indianapolis to automate to drive the cost down so that we can continue to be competitive. Now is it as cheap as moving to Mexico with a lower cost of labor? No. But we will make that plant competitive just because we’ll make the capital investments there.

JIM CRAMER: Right.

GREG HAYES: But what that ultimately means is there will be fewer jobs.

The deal may have saved 1,000 jobs in Indiana today, but that doesn’t solve the structural employment dynamics of a 21st-century economy.

The Broken Window

The interesting thing about the Carrier deal is it is the very essence of the “broken window” narrative of economic creation. A window is destroyed, therefore the window has to be replaced which leads to economic activity throughout the economy.

However, the fallacy of the “broken window” narrative is that economic activity is only changed and not increased. The dollars used to pay for the window can no longer be used for their original intended purpose.

With the Carrier deal, while jobs may be retained, the dollars that would have belonged to the taxpayers are now diverted from their original use into assisting Carrier to keep existing jobs.

In reality, the effect of the Carrier deal is a net negative for Indiana as dollars are diverted from taxpayers which would have created activity elsewhere in the economy. The jobs are still going to be lost at some point as they are displaced by advances in productivity.

The issues surrounding the “Carrier” deal are problematic going forward as well.

On Wednesday, in an interview with Time magazine’s Michael Scherer after being named Time’s Person of the Year, Trump said he wants to speak with the CEO of any company considering shipping jobs overseas. Trump told Reince Priebus, the next White House chief of staff:

“‘Hey, Reince, I want to get a list of companies that have announced they’re leaving,’ he called out. ‘I can call them myself. Five minutes apiece. They won’t be leaving. OK?'”

What deals will have to cut in order to keep these companies from leaving or simply automating their workforces? Who is going to pay for those deals? What is the true economic cost and benefit?

There is no free lunch.

It’s Structural

Yes, reducing taxes, easing regulations and repatriating dollars held offshore which will increase corporate profitability and liquidity. But, will such increase employment, expand production and raise wages?

Let’s use a simple example.

- Company A manufactures and sells a “widget.”

- They sell 10,000 units a year with a domestic manufacturing cost of $15/hr and a net profit of $5 per unit AFTER taxes.

- Trump reduces taxes from $35 to $15 which increases the net profit per unit to $5.73 per unit.

- Net profit for the company rises from $50,000 to $57,300 annually.

- They able to repatriate $10,000 held in offshore facilities.

- A specific regulation is eliminated which now reduces operational costs by $5000 annually.

What does the company do with their new found sources of profits and liquidity?

While the company owners will experience a greater income annually from the tax savings, reduced regulatory costs and repatriation of dollars, there was no increase in the annual demand for their widgets. Since the demand for widgets has not risen in our example, there is no need to expand the production of widgets or increase employment.

Yes, the owners of the company may opt to keep their employees in the U.S. for now because of increased income currently, but eventually, those $15/hr wages will be reduced to $5/hr through outsourcing as competition reduces the profit margins on “widgets.”

Since there was no increase in actual demand from consumers, the best use of capital will return back to shareholder benefits. As Goldman Sachs recently noted about the use of repatriated dollars:

“Buybacks will rise by 30% as companies repatriate cash held overseas. Dividends will rise by 6% in 2017, above the 4% growth rate currently implied by the dividend swap market.”

Last time I checked, stock buybacks do not create jobs.

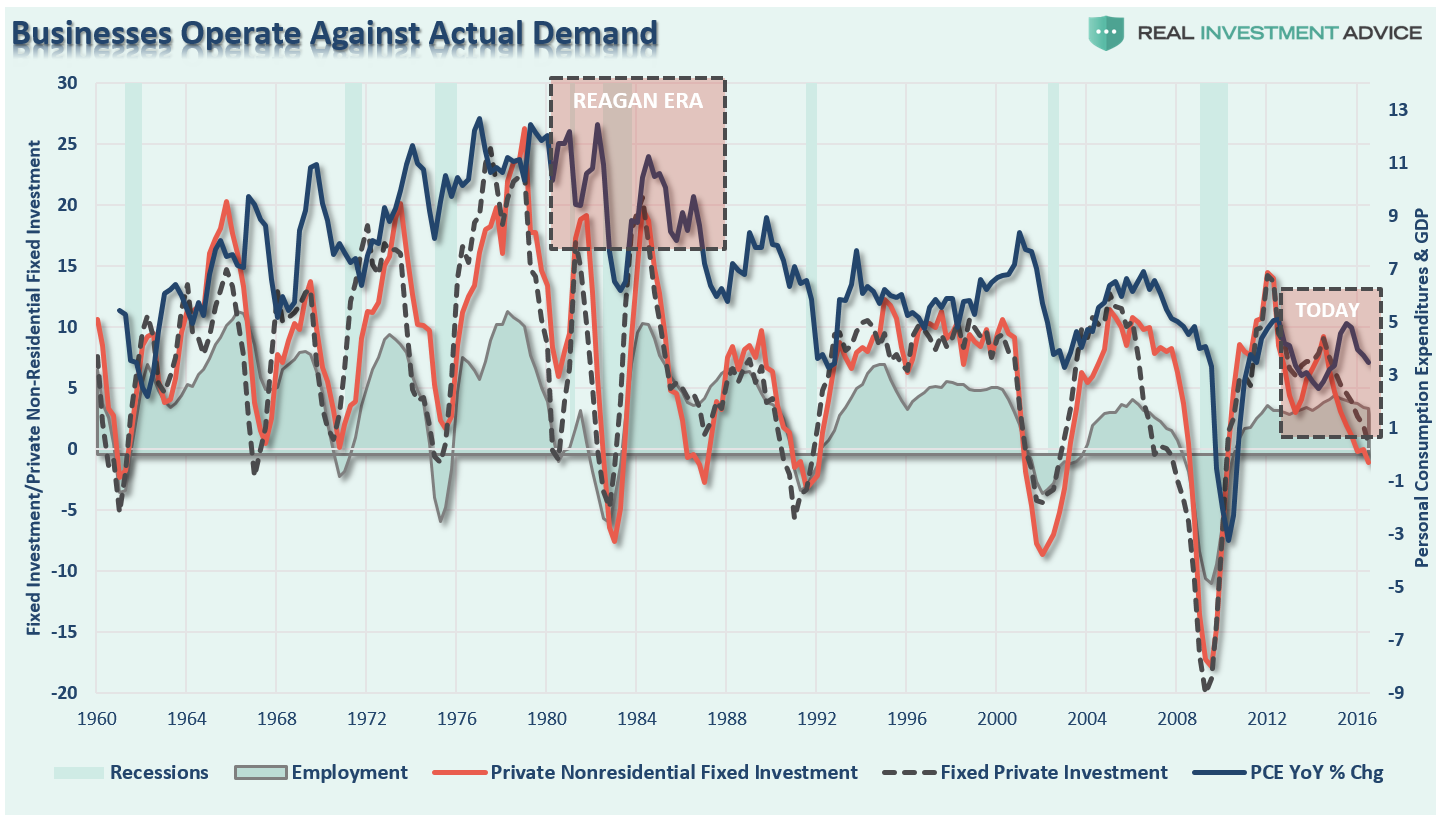

Without an increase in demand, there is little reason to invest dollars into capacity which has been evident over the last few years. As shown in the chart below, personal consumption expenditures during the Reagan administration were 300% higher than today.

Furthermore, consumer indebtedness was low and just beginning to rise allowing consumption to expand at faster rates versus the high levels of debt today.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/12/Debt-GDP-Incomes-120716-2.png[/image]

It is an interesting conundrum since rising production (jobs) leads to higher levels of consumption. However, it is the demand, real or perceived, for a company’s products or services which drives the need for employment and increased production. With consumers effectively “running on empty,” the ability for a further ramp in consumption to create the needed demand is simply lacking.

While the Carrier deal did save jobs, for now, what was missed is the need to focus on the structural employment shifts that have occurred since the turn of the century and will continue to occur in the future.

As noted by Scott Sumner:

“The FRED series shows total manufacturing output rising from 69.789 in 1987 to 129.129 in the most recent quarter. That’s an 85% gain.

At the same time, manufacturing employment has fallen, from 17.499 million to 12.275 million. This represents a decline from 17.3% of total employment to only 8.5% of total employment. That’s the figure that has people so upset. But the cause is not trade; it’s automation.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/12/Manufacturing-Output-Jobs-120816.png[/image]

Think about all of the disruptive technologies currently in play from Amazon, to Uber, to robotics and more. Every industry, business, and employee is under attack from increases in productivity, the drive for lower costs and higher profit margins.

“When people say they are upset about trade, I think that what really bothers them is that automation is allowing us to produce 85% more manufactured goods with far fewer workers. That transition has been painful for many workers, but it’s not about trade—except in one respect.

Trade allows the US to concentrate in industries where we have a comparative advantage (aircraft, chemicals, agricultural products, high tech goods, movies, pharmaceuticals, coal, etc.) We then import cars, toys, sneakers, TVs, clothing, furniture and lots of other goods. It’s likely that our productivity is higher in the industries where we export as compared to the industries where we import. So in that sense, trade may be speeding up the pace by which automation costs jobs. But probably only slightly; in previous posts I’ve shown that even within a given industry, such as steel, the job loss is overwhelmingly about automation, not trade.“

There are certain low-skilled jobs being lost to other countries which have lower labor costs. They are also being lost to technology due to the lack of specific skill sets and a work ethic. Technological developments are a bigger threat to American workers than trade which is the trend of the future and the crux of the structural employment change.

As Greg Hayes noted in the interview with Jim Cramer, companies like United Technologies are focused on how to “train people for the jobs of tomorrow.”

The “Carrier” deal, and future deals like it, only succeed in temporarily keeping the jobs of yesterday with a cost to taxpayers today.