![]()

See this visualization first on the Voronoi app.

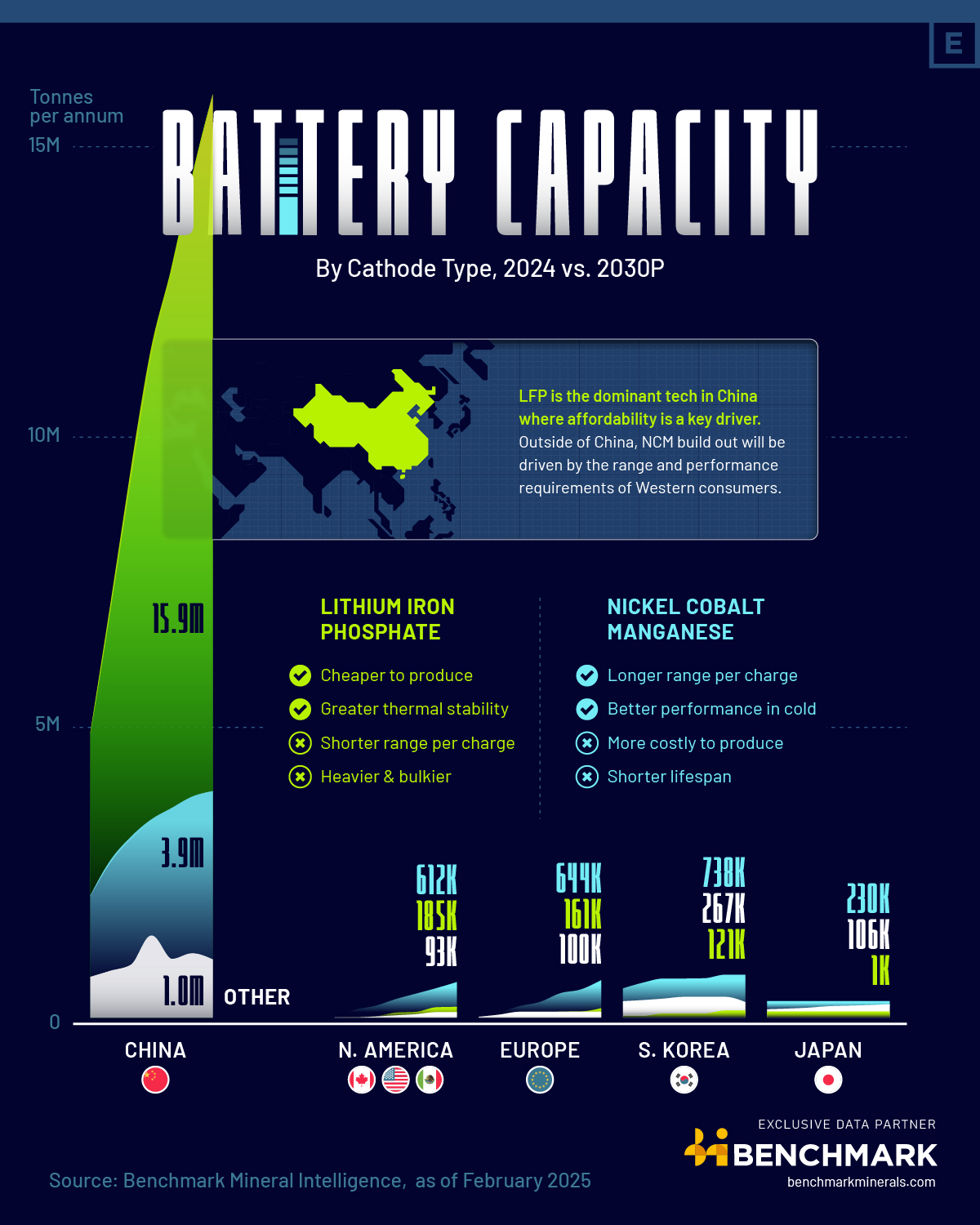

Charted: Battery Capacity by Country (2024-2030)

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

As the global energy transition accelerates, battery demand continues to soar—along with competition between battery chemistries.

According to the International Energy Agency, in 2024, electric vehicle sales rose by 25% to 17 million, pushing annual battery demand past 1 terawatt-hour (TWh)—a historic milestone.

This graphic, using exclusive data from Benchmark Mineral Intelligence (as of February 2025), compares battery capacity by cathode type across major countries. It focuses on the two dominant chemistries: Nickel Cobalt Manganese (NCM) and Lithium Iron Phosphate (LFP).

Understanding Cathode Chemistries

Batteries store and release energy through the movement of lithium ions. The cathode—a key electrode—determines a battery’s cost, range, and thermal performance.

NCM

- Offers higher energy density and better performance in cold climates, but is more expensive and has a shorter lifespan.

LFP

- Known for its lower cost and improved thermal stability, though it delivers a shorter driving range and adds weight.

As of now, LFP cathodes make up 40% of the EV market in terms of gigawatt-hours (GWh).

Beyond passenger vehicles, LFP batteries are widely used in systems that undergo frequent charging and discharging—like residential and grid-scale energy storage—where added weight isn’t a major concern. They’re also ideal for daily-use applications such as buses and delivery fleets.

Regional Market Trends

In China, LFP is already dominant, accounting for 64% of the market in 2024. By 2030, that figure is projected to grow to 76%, driven by a focus on affordability in the world’s largest EV market. Notably, over 70% of all EV batteries ever manufactured have been produced in China, contributing to deep manufacturing expertise.

| Region/Country | Year | % NCM | % LFP | % Other |

|---|---|---|---|---|

| China | 2024 | 27% | 64% | 8% |

| North America | 2024 | 71% | 7% | 22% |

| Europe | 2024 | 69% | 8% | 24% |

| South Korea | 2024 | 62% | 4% | 35% |

| Japan | 2024 | 58% | 0% | 42% |

Outside of China, NCM remains the leading chemistry due to consumer demand for longer range and premium performance.

North America – NCM holds a 71% share in 2024, with a slight decline to 69% forecasted for 2030.

Europe – NCM’s share is expected to grow from 69% in 2024 to 71% by 2030.

South Korea and Japan – Both countries show similar trends, with NCM gaining share as LFP remains limited or absent.

Learn More on the Voronoi App ![]()

If you enjoyed this post, be sure to check out this graphic, which visualizes EU’s critical minerals gap by 2030.