Submitted by Lance Roberts via RealInvestmentAdvice.com,

“Data Dependent Fed” Ignores Data

I wrote on Tuesday of this week:

“The Fed currently finds itself in a tough spot from a “data dependent” standpoint. Last December, when the Fed Funds rate was increased, the Fed discussed the potential for further rate hikes in 2016 as inflation and employment data strengthened. With that data improving, along with the strong rebound in the financial markets, the Fed runs the risk of losing credibility if they DO NOT hike rates again on Wednesday OR give a very strong indication they will do so at the next meeting.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/Employment-Trends-031516.png[/image]

“My personal take is that the Fed will likely NOT hike rates tomorrow, however, stronger language about further rate hikes this year will be included.

The question is whether the market likes the outlook for stronger economic growth more than a further reduction in monetary accommodation?”

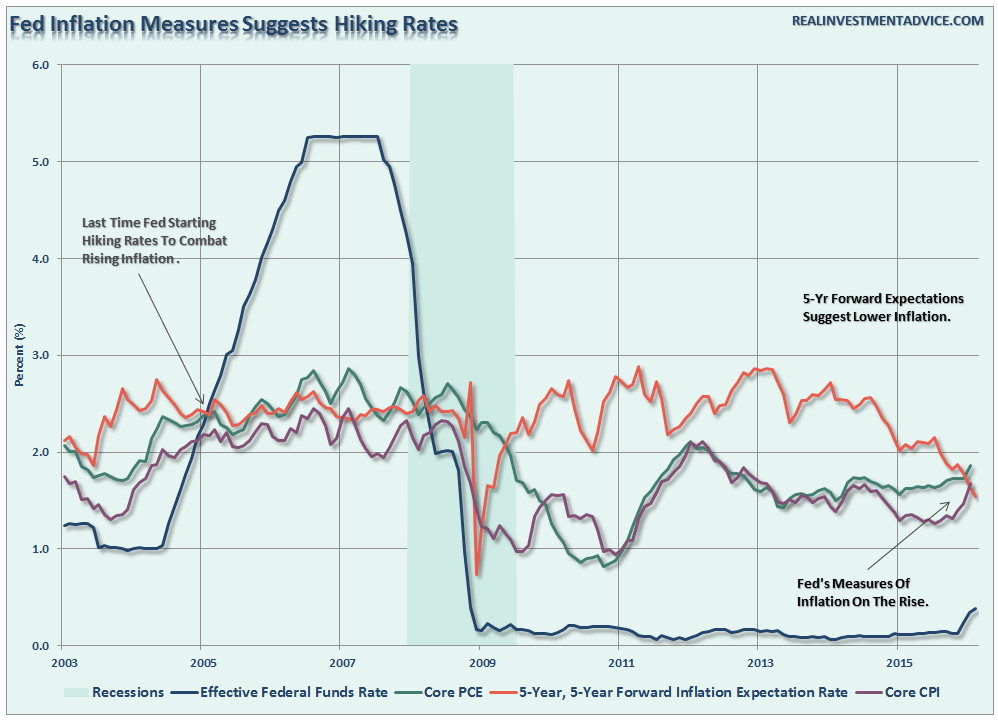

Given the “data” the Federal Reserve is supposed to be looking at, I have to admit I was more than a bit stunned by the lack of action given the more “hawkish” revisions to the Fed’s statement.

The Fed noted that economic strength had expanded in recent months, household spending has picked up and housing had improved further. Employment gains remained strong and indicators point to further job gains ahead. Inflation had also picked up but continues to run below the Fed’s 2.0% target level. All of this suggests that the Fed should have hiked rates at this meeting. However, it was ongoing global risk that kept them at bay

But was it really just “global risk?” The answer was found in the Fed’s “forward guidance,” as their projections explained why they didn’t increase rates. As shown in the chart below, once again the Fed lowered expectations further for economic growth and reduced the number of rate hikes this year from 4 to 2. Yep, “accommodative policy” is here to stay for a while longer which lifted stocks yesterday’s close.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/FOMC-Economic-Forecasts-031616.png[/image]

Besides being absolutely the worst economic forecasters on the planet, the Fed’s real problem is contained within the table and chart above. Despite the rhetoric of stronger employment and economic growth – plunging imports and exports, falling corporate profits, collapsing manufacturing and falling wages all suggest the economy is in no shape to withstand tighter monetary policy at this juncture.

Of course, if the Fed openly suggested a “recession” could well be in the cards, the markets would sell off sharply, consumer confidence would drop and a recession would be pulled forward to the present. This is why “what the Fed says” is much less important than what they do.

The question is whether the market will buy into the “forward guidance” and push higher, or “call their bluff.”

With the ECB and the Fed policy meetings now behind us, all eyes will turn back to economics and earnings. Unfortunately, neither one of those are particularly supportive at this juncture.

Valuations Matter A Lot

On Monday, I wrote an article about the problems “long-term, buy-and-hold” investment advice. To wit:

“There are two primary reasons Millennials aren’t saving like they should. The first is the lack of money to save, the second is the lack of trust in Wall Street.

What Millennial’s, and everyone else, is starting to figure out is that Wall Street is not there to help you, but only to help themselves. “Long-term” and “buy-and-hold” investment strategies are good for Wall Street’s bottom lines as the annuitized revenue stream accrues each year. Unfortunately, for individuals, the results between what is promised and what actually occurs continues to be two entirely different things and generally not for the better. “

Of course, there is always plenty of push back when I lash out against the Wall Street proletariat with such heresy.

Let me be clear, I believe in long-term investing. I do think that you should buy quality investments and hold them long-term. However, what Wall Street, and many financial advisors miss, is the most important point of this argument which is “at the right valuation.”

Valuation, what you pay for an investment, is the single biggest determinant of future returns. In other words, it is not “IF” you should invest but “WHEN” you invest that is the differentiator between achieving your investment goals or not. Let me show you.

According to Dr. Roberts Shiller’s data, the Cyclically Adjusted P/E Ratio is currently hovering around 24x earnings. It is here that the problem for long-term investors currently resides. The first chart below shows the average real (inflation-adjusted) 20-year returns of a $1000 investment made when P/E ratios first hit 20x or 10x earnings.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/20-Yr-Returns-Start-20x-10x-Earnings-031616.png[/image]

As you can see, valuations make a huge difference. The following two charts show the 4-secular bear and bull market investment periods defined by 20x (bear) or 10x (bull) valuation levels and the subsequent return of a $1000 investment.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/20-Yr-Returns-Start-10x-Earnings-031616.png[/image]

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/20-Yr-Returns-Start-20x-Earnings-031616.png[/image]

With the exceptions of 1932, during the “Great Depression,” and the 1993 “Tech Bubble,” investors fared much better by investing when valuations were at 10x earnings or less. Even with the series of bubbles from 1993 to present, returns were eroded by repeated valuation reversions. The psychological impact of those bear markets made the “buy and hold” approach much less profitable and unrealistic for most.

While I have simplified the analysis above to a great degree, a look at all 20-year annual forward returns since 1900, from all valuation levels, shows the same story.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/20-Year-Returns-From-All-Valuation-Levels-031616.png[/image]

Given current valuations near 24x earnings, returns are likely to be closer to 2% over the next 20-years versus the promises of annualized 6%, 8% or 10%.

Of course, this does not mean that every year will be 2%. It does, however, imply that the “bull market” that yielded a roughly 200% return from the March 9th lows will revert back to its long-term mean taking a bulk of those gains away. This is just how markets throughout history have worked, and this time will likely be no different.

This is why managing your money to avoid major drawdowns, especially at high valuation levels, is especially important. The one thing you can’t regain is the “time” lost trying to get back to even.

You can do better.

Proof Why Chasing Returns Is Bad For You

One of the biggest mistakes that investors continually make is chasing last year’s “hot” performers. “Hindsight” bias is a dangerous psychological issue that drives individuals to abandon their investment discipline the fear of “missing out” on returns overrides logic.

Simply put, it is “greed” rearing its ugly head which remains one of the 7-deadly investment sins. As shown in the Callan table of periodic returns, chasing last year’s “winners” has repeatedly led to this year’s “losers.”

The chart below shows major asset classes. I have drawn lines through the S&P 500, Emerging Markets, Bonds and S&P 500 Value indices.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/Callen-Periodic-Table-Returns-031616.png[/image]

What is important to notice is that the S&P 500, Emerging Markets and Bonds have all spent time being both the best performing and worst performing asset classes. Take Emerging Markets for example, by the time individuals realized how great the returns were last year, they were often pummeled with losses soon thereafter. Even bonds, on a price performance basis, have had strong and weak performance years.

However, from an investment perspective, buying valuation based stocks delivered consistent and more conservative returns. For true buy-and-hold investors, the stability of returns made it far easier to adhere to an investment strategy amidst ongoing market volatility. When coupled with fixed income, volatility was reduced further and forward returns increased as interest income and dividends buffered price volatility. S&P 500 Value stocks were never the best performing sector, nor were they ever the worst. But over the long-term, lower volatility, and fewer emotionally driven investment mistakes have been the backbone of investment success.

Just some things to think about.