Nearly 7 years ago, shortly after Mark-to-Market was indefinitely suspended, and Mark-to-Unicorn as we first dubbed it was revealed, we described an odd accounting peculiarity which in the coming years would take the financial world by storm: the so-called "Fair Value Option", and its practical offshoot, the Credit/Debt Value Adjustment (CVA or DVA).

Here was our quick and dirty explanation from April 2009:

"The issue at hand is the "Fair Value Option", which under US GAAP essentially allows the booking of a pre-tax profit when a bank's debt trades lower in the open market. This benefits banks that opt-in for FVO instead of other accounting approaches such as amortized cost, or historic cost.

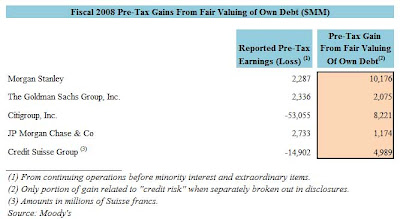

And so readers can get a perspective of just how large an accounting "benefit" the FV Option is to financials, observe the table below which compares 2008 bank Net Income with the Pre-Tax Gain from Fair-Valuing of Own Debt."

In other words, if a given bank's market price of debt was tumbling, or inversely, spread on its CDS (and thus Default Risk), was soaring, the bank had the full blessing of accounting to push up its bottom line thanks to DVA "adjustments" (which assumed it would gain on repurchasing of its crashing bonds... assuming of course that it cared about repurchasing its crashing bonds instead of, say, avoiding bankruptcy).

Alternatively, the same bank would be punished and its pre-tax profit would decline when the value of its bonds would rise.

To us, and many others, this was merely the latest accounting gimmickry paradox: it meant that the worse a bank was perceived by the open market through the sale of its publicly-traded debt securities, the more "profits" it could generate, ultimately peaking with the bank filing for bankruptcy at which point its pre-tax profit would be maximum. Too bad that at that point the bank would be, well, bankrupt.

Still, for all intents and purposes, the rule was instrumental in permitting banks to cushion their earnings during times of peak stress, by masking the worst possible loss they would have to report, something which came in very handy in 2008 and again during the first European near-death encounter in 2011.

Today, we are delighted to report that DVA is no more, because as Bloomberg reports, this "fair value option" has been eliminated by the U.S. body that sets bookkeeping standards.

The debt valuation adjustment, or DVA, will no longer be included in net income, according to revisions to the fair-value measurement standard published by the Financial Accounting Standards Board Tuesday. Firms can now report changes in the value of their debt as part of “other comprehensive income,” which isn’t part of the bottom line that analysts and investors watch most closely.

The DVA rule increased net income when a bank’s bonds tanked, on the theory that the firm could buy back its bonds at a lower price and benefit from the decline in value. In practice, a financial institution in trouble, such as Lehman Brothers Holdings Inc. in 2008, is typically unable to buy back bonds because it can’t get fresh financing.

As Bloomberg adds, "most of the biggest U.S. banks already separately report earnings figures each quarter that exclude the impact of DVA" however the parallel disclosure made bank filings even more incomprehensible than usual.

While the revised standard goes into effect in 2017, "the largest banks in the past have implemented some accounting changes ahead of schedule to satisfy analysts and investors keen to see the new standard in practice."

What this means in practice is that instead of Bank of America's 10-Q being 243-pages (as in its most later quarter for example), it will now be, we hope, on average one entire page shorter.