Authored by Lance Roberts via RealInvestmentAdvice.com,

Every day, the A-listers, those known around the world as household-name financial media royalty, are making public statements that if taken on the surface as actionable advice, are going to lead to unpleasant financial surprises.

Not for them. For you.

As authorities, no matter what they bloviate about on radio, television and in print, their words are taken as unadulterated truth. Perhaps it’s because they believe they’re bulletproof against criticism or a half-truth is just as helpful as the complete story.

So, is all the advice they provide, incorrect? No. Much is acceptable to follow. Where they run into trouble (or where you will experience long-term disappointment), is the mysterious math of stock market returns behind those media sound bites. What is communicated about investing and what is experienced by most investors are consistently disparate outcomes.

Recently, Suze Orman the superstar financial planner outlined for CNBC, her observations on the new reality of retirement. Let’s break down where she got it correct and the information you need to know to adjust your expectations.

Read: Suze Orman says this is the ‘New Retirement Age’ – And it Might Make you Cringe.

Let’s break it down:

“70 is the new retirement age.”

I’d say Ms. Orman is close. Very close.

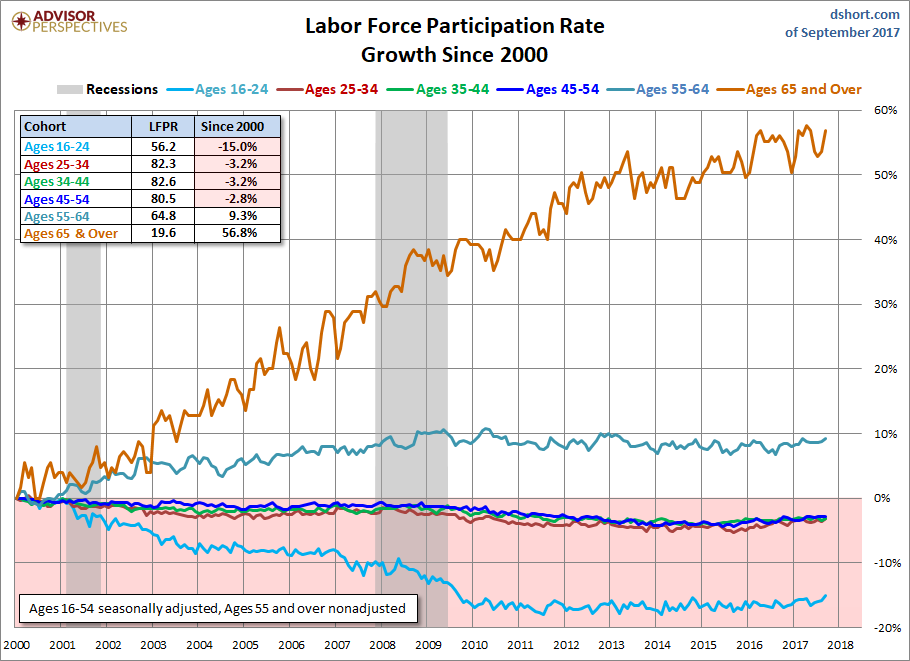

Per market statistician Doug Short:

“Since January 2000, the participation rate for all the elderly has soared by 55.9 percent and for elderly women by 74.3 percent.”

There are several valid reasons for people to work longer or return to the workforce. Obviously, the primary reason for working longer is the need for cash flow as a majority of Americans are inadequately prepared for retirement.

Research conducted this year from The National Institute on Retirement Security finds that 76% of Americans are concerned about their ability to achieve a secure retirement.

A 2016 survey by Transamerica Center for Retirement Studies finds that baby boomers or those born between 1946-1964 have median retirement savings of $147,000.

So yea, Suze Orman is on to something valid here.

Sure, there are retirees who return to the workforce to remain socially and mentally engaged. Primarily, it’s to pay the bills.

Healthcare costs add up, Ms. Orman notes.

Give that financial planner a prize. Another effective electronic bit of wisdom. Fidelity Investments estimates for a couple retiring today, $275,000 should cover healthcare costs in retirement. A 6% jump over 2016.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/11/Rosso-Retirement-Savings.png[/image]

The Employee Benefit Research Institute at www.ebri.org, in their long-running Retirement Confidence Survey, outlines how retirees dramatically underestimate their healthcare expenses in retirement (47% found their healthcare expenses somewhat and much higher!).

“Having a comfortable retirement is all about using compound interest, Orman sad at Miami’s eMerge conference in June: “You invest money and your money makes money, and the money you made with the money that you had makes money, and everything compounds.”

Well, this commentary is a bit “iffy,” as compounding only works when there is NO CHANCE of principal loss. It’s a linear wealth-building perspective that no longer has the same effectiveness considering two devastating stock market collapses which inflicted long-term damage on household wealth.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/07/SP500-Time-To-Breakeven-1990-070217.png[/image]

When it comes to compounding, investors should never suffer torturous time to breakeven. Compound interest works if the rate of interest is consistent, not variable. You wouldn’t know it from stocks, especially this year, but from what I know, stocks are indeed a variable, and occasionally, volatile asset class.

So sorry, Suze. This bit of knowledge? Strike out. Not everything compounds.

“Orman explained that if a 25-year-old puts $100 into a Roth IRA each month, they could have $1 million by retirement.”

This statement perplexes me. While I wholeheartedly agree with a monthly investing or saving discipline spouted here, especially into a Roth IRA where earnings grow tax-deferred and withdrawn tax-free at retirement, I had a dilemma making her retirement numbers work.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/11/Orman-SP500-DCA-Retirement-102817.png[/image]

As outlined in the chart above, on an inflation-adjusted basis, achieving a million-buck balance in 40 years by dollar-cost averaging $100 a month, requires a surreal 11.25% annual return. In the real world (not the superstar pundit realm), a blind follower of Suze’s advice would experience a whopping retirement funding gap of $695,254.68.

I don’t know about you, to me this is a Grand Canyon expectation vs. reality-sized unwelcomed surprise.

On a positive note, investing on a disciplined basis for 40 years still results in a retirement account balance most Americans nearing retirement would envy. However, it’s far from a million as touted so effervescently by Ms. Orman.

Overall, I give Suze Orman a C+ for her media-pundit ponderings this time around. She performed better than others whose words of wisdom I parse.

Financial star-power across the board fizzles out when it comes to sharing long-term stock performance reality and debunking the fictional warm and fuzzy story of compounding. It’s like they’re all afraid to share the truth about market cycles, the math of loss and how compounding does not apply adequately to variable assets.

When it comes to shortfalls in reaching goals established in a financial plan, it’s not those smiling faces on the financial wall of fame that are accountable to you. If they’re wrong, it seems the public has short memories and willing to give them a pass. Must be nice.

“Hey, they must be right, they’re the pundits! The problem must be me!”

No, the problem isn’t you unless of course, you’re a blind follower of the taffy-truth pulling of financial media superstars.

If you’re a reader of Real Investment Advice, then I find comfort in knowing you’re never a blind follower; your perspectives are grounded in reality.