Submitted by Lance Roberts via RealInvestmentAdvice.com,

The Fed’s Got A Problem

The most recent employment report sent the financial market pundits abuzz claiming that the economy was on solid footing with no recession in sight. The problem, for anyone willing to actually look at the data, was the underlying data was mostly disappointing.

While the BLS trumpeted 242,000 new jobs in February, wages declined 0.1% and the average workweek fell by 0.2 hours along with aggregate hours worked falling a hefty 0.4%. Furthermore, part-time work soared in February while full-time job growth was mediocre.

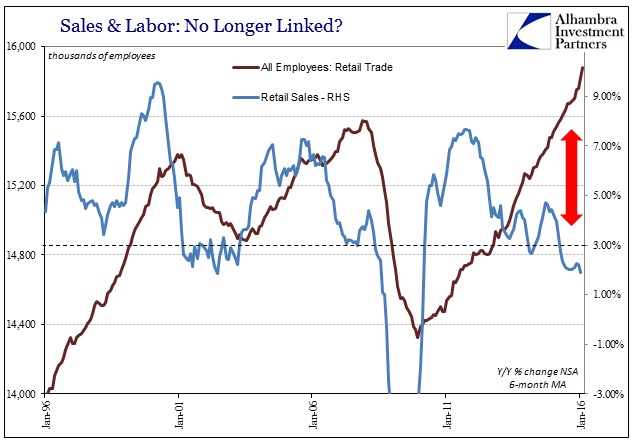

But even stranger was that out of the 242,000 jobs, retailing saw a massive jump of 55,000 jobs. This is in a month when stores are not hiring a lot of part-time work to deal with a shopping season. Jeffrey Snider at Alhambra Partners picked up on this by pointing out the differential between actual retail sales and “hiring.”

“Starting April 2015, overall retail sales (again, including auto sales) fell below 3% on a 6-month average basis (meaning more than a one-month drop in growth rate) – and have remained closer to 2% than even 3%. In past cycles, that has meant initiation of contraction in retail trade employment and widespread recession. Not this time, however, as the BLS gives us a remarkable +313k gain (including February 2016) over the last 11 months. That equates to an astounding 28.5k per month.”

Pretty amazing. This is even more confounding when you look at the NFIB’s Small Business Survey which shows real retail sales and expectations of sales both on the decline.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/NFIB-Retail-Sales-030916.png[/image]

But it is not just in “retail trade” that employment gains are an issue but rather throughout the entirety of the report. The obfuscation of the data is coming from the mathematical “seasonal adjustments” along with the “birth/death” adjustment which are adding jobs that aren’t actually there.

Think about it this way. If the unemployment rate were truly 4.9%, and jobs were actually being created at the fast clip since the 90’s, then labor force participation rates, along with wage growth, should be at similar levels. Right? Uhm....

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/Employment-Population-16-54-030916.png[/image]

Of course, the reason that labor force participation rates remain so low is that job creation has failed to exceed the growth rate of the working-age population. With the population growing faster than employment, the number of unemployed living in the shadows continues to swell.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/Employment-Population-NetChange-030916.png[/image]

Of course, herein lies the problem for the Federal Reserve, who remains intent on further rate hikes this year, which could lead to a major policy error. The Fed’s own Labor Market Conditions Index, which has now declined into contraction, also suggests that something is very wrong with the employment data over the last several months.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/LMCI-FedFunds-030916.png[/image]

If the employment gains were indeed as strong as the Fed, and the BLS, currently suggest; the labor force participation rate should be rising strongly. This has been the case during every other period in history where employment growth increased. Since the financial crisis, despite employment gains, the labor force participation rate has continued to fall.

This suggests that at some point in the future, we will likely see negative revisions to the employment data showing weaker growth than currently thought.

The issue for the Fed is by fully committing to hiking interest rates, and promoting the economic recovery meme, changing direction now would lead to a loss of confidence and a more dramatic swoon in the financial markets. Such an event would create the very recession they are trying to avoid.

Oil – This Ain’t 2009

I live in Houston where oil is literally the life-blood of the economy. My wife works in the oil field related sales, my friends work for oil companies as well as my clients who are working and saving for their retirement. I would love nothing more than oil prices to go much higher as it would make my life immeasurably simpler.

Over the last couple of weeks, the rally in oil has gotten the financial media and analysts all stirred up with predictions the “bottom in oil is in” and “$70/bbl oil is on its way by summer.” These views are based on the assumption that the decline in oil prices today is much like what we saw during the “dot.com bust” and during the “financial crisis.”

It’s not.

This morning Liz Ann Sonders from Schwab sent out the following tweet:

This misses the main problem with oil which is not going to be resolved anytime soon. The chart below shows the current supply of oil versus demand. Given that prices over the long-term are a reflection of the supply/demand dynamic, the current problem is quite apparent.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/OIl-Supply-Demand-030916.png[/image]

This supply/demand imbalance is not going to be resolved my a mild stabilization in supply but rather a rapid decline in production. However, such a swift decline can not feasibly occur due to the need by oil companies to generate income to continue operations, make debt payments, and generate a profit, albeit at much lower levels, for shareholders. As shown in the chart above, the oversupply of oil was eventually reversed but over a very long period of time.

When the supply/demand imbalance became inverted it paved the way for massive oil price rallies in 2005 and 2009 (highlighted circles in the chart below) as “peak oil” became the prevailing fear.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/Oil-Price-1980-Present-030916.png[/image]

With oil supplies once again exceeding demand, particularly in a weak global economy, oil companies will once again have to balance reducing supply against maintaining operations and profitability. Therefore, we are once again in position for a long, slow, decline in supply which will lead to sustained lower trading ranges for oil prices. Consequently, this will lead to lower reported profit margins for energy companies for the foreseeable future.

The point here is simple: “This ain’t 2009.”

Yes, there will terrific trading opportunities for energy-related companies in the future. But first we need to work through the shake out of marginal companies that will file for bankruptcy, consolidation of weaker but stable players and reversions of pipelines back into parent companies. These actions will likely keep action volatile in the sector for a while and there will be significant money lost on speculative bets that go bust.

None of this is a bad thing, it is just the consequence of excess being reverted to a healthier and strong state.

If only Central Bankers understood the same.

The NFIB’s Un-optimistic View

While the media continues to jump on every government skewed statistic to spin into a positive headline, a recent survey of “boots on the ground” companies suggest something else is going on in the economy.

The National Federation of Independent Business recently released their latest survey of small businesses for February. The results were less than optimistic as shown by the sharp decline in their overall outlook over the last couple of months.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/NFIB-Optimism-Index-030916.png[/image]

As Bill Dunkleberg, Chief Economist for the NFIB, stated:

“Monthly management of monetary policy using data subject to substantial revision is inconsistent with the acknowledged lags in policy and not supportive of real growth which requires more policy consistency. Financial markets, of course, thrive on the variability such policies produce and support a zero-interest-rate policy (ZIRP).

Meanwhile, compared to 2009, consumer interest income is down cumulatively over $3 trillion dollars, an unhappy side effect of Fed policies. Low interest rates are great if they occur in an economy that presents investment opportunities. This happens when the economy is exhibiting solid growth which it has not done in this expansion. The 1983 expansion averaged 650,000 new jobs each quarter compared to 450,000 in this expansion with a labor force 30 percent larger.

NFIB data indicate slow growth in the first quarter following the 1 percent growth rate for the fourth quarter of 2015. The GDPNow forecast from the Atlanta Fed is about 2 percent and the NFIB data basically agree. Owners are very pessimistic about business conditions in the coming months and spending and hiring plans have softened.”

Despite the always optimistic view of the media and Wall Street, businesses that ACTUALLY OPERATE in the economy have a much different view. Not surprisingly, the correlation between NFIB expectations and economic growth are fairly correlated which suggest that the economy is likely weaker than headlines suggest.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/NFIB-Expections-GDP-030916.png[/image]

As shown above, the decline in actual and planned sales would also suggest weaker hiring. Not surprisingly, the number of firms increasing employment last quarter also declined which again brings into question the accuracy of recent employment reports.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/03/NFIB-Expectations-Employment-030916.png[/image]

Of course, if things were as good economically as we are told by Wall Street and the mainstream media, would the ECB really be needing to drop further into negative interest rate territory and boost QE?

Just some things to think about.