Authored by Sven Henrich via NorthmanTrader.com,

I feel compelled to keep documenting reality to raise awareness of the ever larger market dangers which keep lurking underneath the current bubble. Indeed I keep seeing a great void not only in awareness but also in price discovery that have propelled markets to current levels leaving investors and participants ever more lulled into a false sense of security by the current unprecedented phase of volatility compression.

Take these comments as part of an ongoing journey outlining building risk factors. You can read about additional updates/background in the Macro Corner, Market Analysis , NT Blog and the Market Analysis sections of the site..

Briefly to get everyone on the same page:

Two way price discovery, as a normal part of market functioning, has practically seized to exist. I’ve pointed out charts of this nature before, but I’ll use the quarterly $DJIA chart as an example to illustrate the point:

Several points to make here:

The $DJIA is on its 9th quarter of consecutive price appreciation. The last red candle was before the now almost $5 trillion in combined global central bank intervention since February 2016.

The $DJIA, as the $SPX, is now on its 4th consecutive quarter of not reconnecting with its quarterly 5 EMA. Such an extended disconnect has never occurred in the 100 year market history I reviewed. And believe me, I’ve looked:

The few examples of extended quarterly 5EMA disconnects I could find were associated with coming market pain.

Aside from global central bank intervention (also see Liquidity Wave) the other key contributing factor to the no 2 way price discovery equation is the unprecedented influx of passive ETF investing and plenty of data exists to illustrate this point:

What has happened? I consider it retail capitulation. For years hedge funds have underperformed central bank liquidity infested market waters yet retail investors keep seeing markets go up with no downside ever and no apparent associated risk with rising multiple expansion.

The end result: Investors are completely impervious to the building risk factors and the actual price/valuations of asset prices they indirectly own.

If there is no risk to holding stocks then who cares if the underlying asset will ever grow in its valuation? Who cares if the business models don’t match up the PEG ratios?

Price targets have now simply been rendered an exercise in FOMO expectations. Indeed Wells Fargo rightfully calls it another QE effect:

“It’s very similar to QE.” Harvey said Wednesday on CNBC’s “Trading Nation.” “With QE, you took a certain part of the Treasury market out of circulation. Now what you’re doing is you’re taking a good part of the equity market out of circulation, and you’re upsetting the supply and demand dynamics. There are fewer natural sellers.”

Wells Fargo’s new 2017 forecast calls for the S&P 500 to reach 2,636, which reflects about a 1.9 percent gain from current levels. The firm started the year with a 2,475 year-end target, which would have come in about 4 percent short if the year was to end now.

“We don’t see a lot of bad news in the short term, and so we feel it’s fairly justified,” said Harvey, who became in charge of the firm’s S&P 500 price target and earnings forecast in April. He acknowledges Wells Fargo’s initial forecast was “too conservative” and the year has been exceeding expectations.

According to Harvey, there’s still momentum in place for stocks to grind higher.

“No one wants to be the first one out of the pool. No one wants to de-risk at this point in time,” Harvey added. “You have this mindset of FOMO — fear of missing out.”

There. FOMO. I can’t disagree that this price extension or even further extension could happen. As long as there is no consequence to overpaying for assets and volatility remaining compressed with all corrective activity having been removed from markets what is to stop prices from advancing ever more?

The answer: The Great Void.

Let me explain.

Firstly let me go back to a chart I showed back in March when I discussed The Finale Wave:

Back then I said the following:

“This is actually a pretty good trend line for bulls as it keeps rising of course, hence the later price were to get to there the higher markets may extend. The bad news: If this trend line has market relevance (as it appears to looking at its history), then it suggests the following:

$SPX broke this trend line in 2008/2009. And despite vast global central bank intervention as well as building a global debt load to the tune of over $152 trillion, markets remain below this long term trend line. It’s still technically broken.”

This still applies to this day and here’s an updated view of the chart with the added context of the multi decade declining trend in the 10 year yield:

Why is this important: It could be argued that low yields remain the theory of everything over the past 30 years as we’ve moved from one bubble to next with central banks reacting each time by dropping interest rates to “save markets”.

Take the $DAX chart I showed the other day:

Same concept.

What’s the net effect of one way price discovery? Massive, historically unprecedented technical extensions that scream danger, incompatible with the complacent attitude of investors.

Let me show you some charts that need to be seen to believed. Frankly if ETF investors were to see these charts they may get a better sense as to where in historical context they are deciding to invest long in these markets.

Hence my quest to raise awareness and I use linear charts in some cases to really drive the point home. Linear charts make ZERO difference in regards to moving average disconnects or fibonacci retrace levels, but they can help illustrate the vastness of the void. Indeed log charts can breed a sense of complacency as often price does not appear anywhere near as extreme.

On this latter point let me give you 2 examples of two very successful companies using log charts:

$FB:

A very steady uptrend following trend lines very diligently with tags producing either rejections or bounces. The stock has had no real correction in almost 2 years. The fib levels outline the size of the corrective opportunity were markets to get shaken out of their current lull.

$GOOGL shows a similar picture:

An ever narrowing channel showing a void of any corrective activity of size.

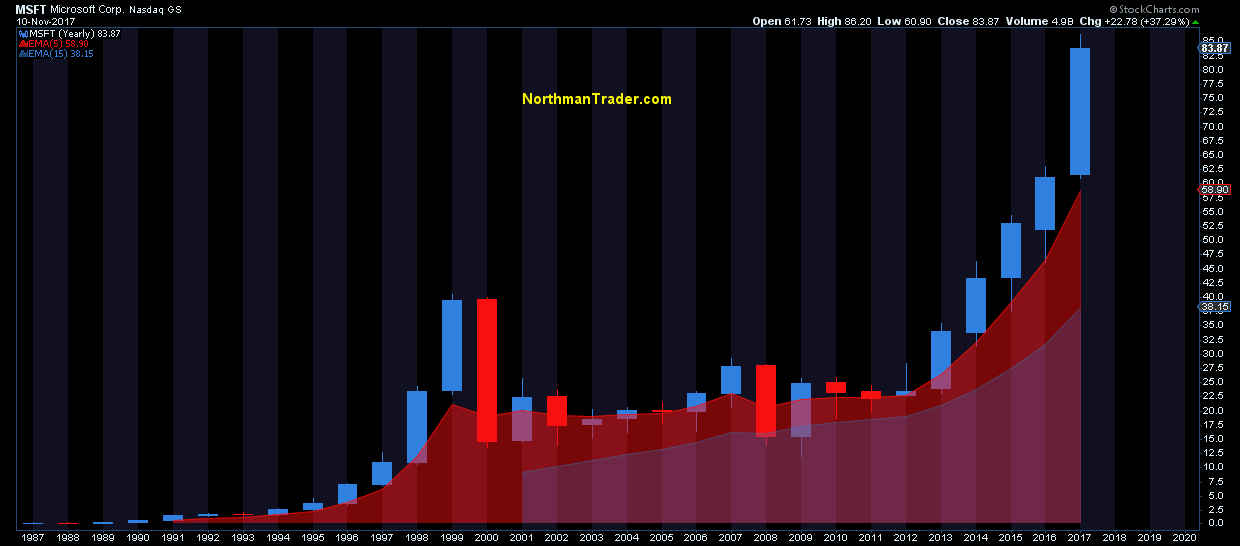

Now let’s get to the great awakening. I’m showing you a few examples of individual large cap stocks on yearly charts in relation to basic moving averages. Note the regular proximity to the annual 5 EMA in particular.

Now look at 2017. THIS is where investors are passively adding money to markets.

How do these things end? Can these things end? Look no further to $GE to give an imminent sense of risk:

Reconnects are coming. They always do and just because markets get stretched to extreme levels it does not mean reconnects are not coming.

These disconnects have been brought to you by one way price discovery. “No natural sellers” Wells Fargo calls it. That’s right. No sellers. Markets have buyers AND sellers. If there are no sellers you don’t have a market.

No sellers means no volatility. And the extremity of the volatility compression is highlighted in its inverted product the $XIV:

On the $VIX itself all regular spikes to the weekly 500MA have been eliminated 2017. For now.

History suggests that this state will not be able to sustain itself:

2017 has shown that extreme markets can become more extreme. There is nothing new about that. We’ve seen it famously in 2000.

Extreme markets do not imply future performance. But hey help inform risk/reward.

Whether we continue to extend price discovery in a one way fashion into year end I can’t say. What I can say with affirmation is that investors appear utter oblivious as to the historic and technical context in which they allocate cash to the long side.

One way price discovery, volatility compression and over 8 years of central bank intervention has paved the way to a general attitude that investors can’t lose money being long. Price will always come back. Not only in our life times, but these days every day as no downside ever last more than a few minutes. No natural sellers.

This will change.

And it’s critical for investors to keep an eye on possible signs of change, even subtle signs. I offered some not so subtle signs in Caution Slowdown. But macro signals can take a long time to play out in a market void of any apparent negative triggers.

Friday’s first $VIX close above 10 in 8 weeks may not amount to anything, but then it may also offer a subtle sign that change is perhaps closer than we think:

Yes the 200MA is now down to a pitiful 11.14, but the weekly close puts it above it. For the first time in a very long time.

Great Voids have a way of filling. Perhaps not in space, but here on earth they generally do. It’s just a matter of time. Remember: Tops are processes.