Submitted by Lance Roberts via RealInvestmentAdvice.com,

For the third time in four weeks, the market was closed on Monday due to a holiday. Not only is this week shortened by a holiday, it is also coinciding with the annual Billionaire’s convention in Davos, Switzerland and the Presidential inauguration on Friday. Increased volatility over the next couple of days will certainly not be surprising.

In this past weekend’s missive, I discussed a variety of “extremes” being registered in many areas of the market and particularly in prices. To wit:

“I have often compared market prices to the equivalent of “stretching a rubber band.” Prices can only deviate so far from the long-term trend line before a mean reverting event eventually takes place. Much like a “rubber band,” prices can only be stretched so far before having to be relaxed to provide the ability to be stretched again.

The chart below shows the long-term trend in prices as compared to its underlying growth trend. The vertical dashed lines show the points where extreme overbought, extended conditions combined with extreme deviations in prices led to a mean-reverting event.”

“This is shown a bit clearer below which compares the deviation of the S&P 500 from the long-term growth trend. Currently, while only slightly below the peak of the 2000 “dot.com” bubble, the deviation is at levels that have ALWAYS coincided with a negative mean reverting event or very poor, and highly volatile, forward returns.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Deviations-Trend-011317.png[/image]

I know…I know. As soon as I wrote that I could almost hear the cries of the “perma-bull” crowd exclaiming “how many times have we heard that before.”

They would be right. The problem with the majority of analysis, in my opinion, is the mismatch between long-term analysis and short-term time frames. The problem with long-term price analysis is the failure to predict short-term price changes. However, short-term analysis leads to psychological wear where analysts have spotted “Head and Shoulder” formations, “Hindenberg Omens,” and “Puppy Monkey Baby“ patterns that have failed to predict a market change.

Of course, like “crying wolf,” when these short-term patterns and long-term prognostications fail to immediately validate themselves, they are summarily dismissed as being wrong, or just “mumbo jumbo,” which often leads to unwanted outcomes.

The primary problem is the “duration mismatch” between most technical analysis, which is typically very short-term (minute, hourly, daily), and the outlook for investors which is in years.

As a portfolio manager, what is important for me is the understand the longer-term “TREND” of market prices. By looking at weekly and monthly data, the trend of prices is revealed allowing for a better match between portfolio goals and related market risks.

During “bull markets,” prices are in a steady advance with corrections to the longer-term bullish trend presenting buying opportunities. When prices become extended from the trend, such deviations provide opportunities to take profits and rebalance portfolios.

Conversely, during “bear markets,” prices are in a steady decline with corrections to the longer-term bearish trend presenting selling, hedging, and shorting opportunities. When prices become extended away from the bearish trend, such deviations should be used to take profits in short positions and portfolio hedges.

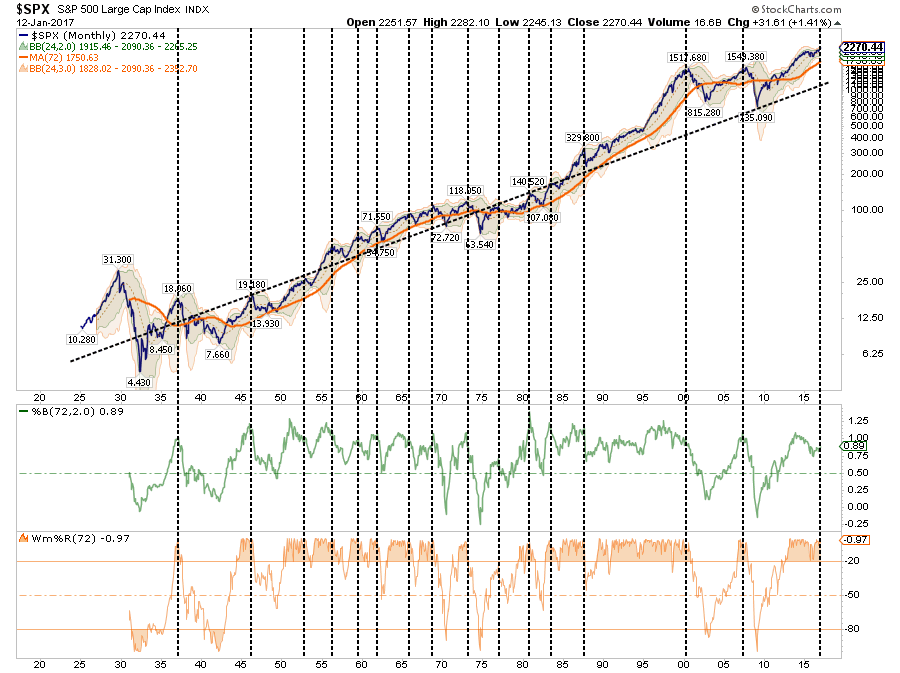

This idea is shown in the chart below.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Bull-Bear-TrendChange-011617.png[/image]

By using a 72-week moving average, the longer-term trend of prices is more clearly revealed. As stated, corrections to the longer-term trend during bull markets were buying opportunities, whereas during bear markets they were selling/shorting opportunities.

VERY IMPORTANTLY – note that at the peak of the previous two markets the change from a bullish to a bearish trend was denoted by the following price action:

- A break of the long-term moving average

- A rally back to the long-term moving

- A failure and a move lower in price than the most recent bottom.

While this occurred at the beginning of 2016, it was quickly reversed following rapid intervention by global Central Banks quickly intervening with a flood of liquidity. The markets have now resumed their bullish trend currently but are pushing the limits of historical advances as noted this past weekend.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Advances-010917.png[/image]

The Psychology Of Loss

The problem ultimately comes down to psychology.

Last year, I wrote an article about the fallacies of “buy and hold” investing which received a good bit of push back from the community of advisors who tout that the only way to invest is to buy low-cost ETF’s and hold them long-term. As I penned:

“Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/01/Math-Of-Loss-10pct-Compound-011916.png[/image]

The “power of compounding” ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required.

In reality, chasing returns is much less important to your long-term investment success than most believe.”

Emotions and investment decisions are very poor bedfellows. Unfortunately, the majority of investors make emotional decisions because, in reality, very FEW actually have a well-thought-out investment plan including the advisors they work with. Retail investors generally buy an off-the-shelf portfolio allocation model that is heavily weighted in equities under the illusion that over a long enough period of time they will somehow make money. Unfortunately, history has been a brutal teacher about the value of risk management.

Take a look at the chart below.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-VIX-200DMA-Extensions-011617.png[/image]

The current extension of the market above the 200-dma, combined with extremely low volatility readings and overbought conditions, have not been kind to investors over the last couple of years.

This overbullish, overextended market is also evidenced on a MONTHLY basis with prices currently pushing a rare 3-standard deviation extensions above the 3-year moving average.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Monthly-BollingerBands-011617.png[/image]

Sure, this time could certainly be different. There is just a really high probability it will not be.

But such observations rarely deter individuals in the short-term as our emotionally driven “fear of missing out” and the now ingrained belief the “Fed won’t let the market fail,” blinds us to a multitude of psychological traps. These “traps” are the biggest reason for underperformance by investors who participate in the financial markets over time.

- Loss Aversion – The fear of loss leads to a withdrawal of capital at the worst possible time. Also known as “panic selling.”

- Narrow Framing – Making decisions about on part of the portfolio without considering the effects on the total.

- Anchoring – The process of remaining focused on what happened previously and not adapting to a changing market.

- Mental Accounting – Separating performance of investments mentally to justify success and failure.

- Lack of Diversification – Believing a portfolio is diversified when in fact it is a highly correlated pool of assets.

- Herding– Following what everyone else is doing. Leads to “buy high/sell low.”

- Regret – Not performing a necessary action due to the regret of a previous failure.

- Media Response – The media has a bias to optimism to sell products from advertisers and attract view/readership.

- Optimism – Overly optimistic assumptions tend to lead to rather dramatic reversions when met with reality.

The biggest of these problems for individuals is the “herding effect” and “loss aversion.”

These two behaviors tend to function together compounding the issues of investor mistakes over time. As markets are rising, individuals are lead to believe that the current price trend will continue to last for an indefinite period. The longer the rising trend last, the more ingrained the belief becomes until the last of “holdouts” finally “buys in” as the financial markets evolve into a “euphoric state.”

As the markets decline, there is a slow realization that “this decline” is something more than a “buy the dip” opportunity. As losses mount, the anxiety of loss begins to mount until individuals seek to “avert further loss” by selling. As shown in the chart below, this behavioral trend runs counter-intuitive to the “buy low/sell high” investment rule.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/10/Investor-Psychology-100k-103016.png[/image]

Despite all of the arm waving and pounding on the table by advisors touting long-term average returns, time-in-the-market, etc., the psychological impact of loss is all too real. While “buy and hold” investing has its appeal during bullish trending markets, the “impact of loss” on individuals is a far greater emotional pull. This is why investors tend to do everything backwards by “buying high” (greed) and “selling low” (fear).

This is why managing “risk” always “wins” over the long-term by reducing the emotional pull to “do something” at precisely the wrong time. The reality of loss tends to be more than most can stomach and sentiments of “time in the market” will go mostly unheeded. This is, of course, why many of the coveted millennial investors have already rejected much of the Wall Street rhetoric after watching the devastation that wrecked their parents over the last 15 years.

You can do better.