Submitted by Lance Roberts via RealInvestmentAdvice.com,

In this past weekend’s newsletter, I discussed the end of the mutual fund redemption period. (Charts updated through yesterday’s close.)

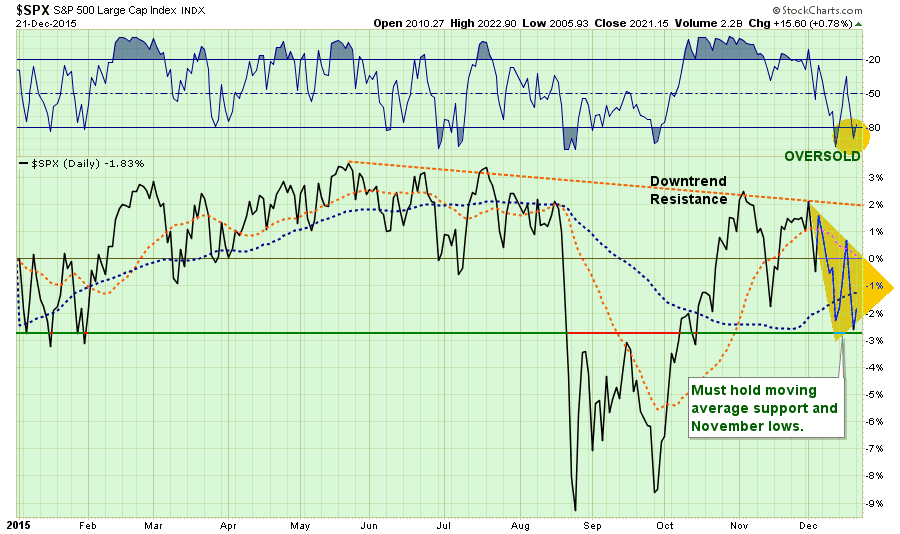

“Friday’s sell-off, combined with options expirations, pushed the markets back to short-term oversold conditions and at previous support.”

(Note: After a second attempt at the downtrend resistance the market has built an accelerated downtrend. If the market is unable to reverse this decline in short-order, the odds of a more substantial correction increase.)

“For the year, the markets continue to post negative returns, which is a low probability event historically for 5th years of decades.

However, as I laid out at the beginning of November, with markets now oversold, option rolls and redemptions complete, this should clear the way for a rally into the end of the year. Such a rally will likely not be huge, but enough to re-balance portfolios heading into 2016.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/SP500-MarketUpdate-122215-2.png[/image]

“I have reiterated over the last several weeks, that such a rally, driven primarily by window-dressing by mutual funds for year-end reporting, is in line with previous expectations.”

It’s Now Or Never For Santa

With the market now back to oversold conditions and redemptions complete, it is now or never for the traditional “Santa Rally.”

If we go back to 1990, the month of December has had average returns of 2.02% with positive returns 81% of the time. Over the past 100 years, those numbers fall slightly to a 1.39% average return with positive returns 73% of the time. Statistically speaking, the odds are high that the market will muster a rally over the next couple of weeks.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/December-Stats-122215.png[/image]

However, given the volatility of the recent decline, any rally that does ensue will likely fail at the current downtrend resistance. As I discussed in detail recently, the underlying dynamics of the market are substantially weak and, on a longer-term basis, are more akin to market peaks than the beginning of new bull market advances.

While the short-term trends are indeed still bullishly-biased, the longer-term analysis (monthly) reveals a more dangerous picture emerging. As shown below, the market is currently exhibiting all the same traits as the previous two bull-market peaks. Price momentum is deteriorating, participation waning, and price advances stalling.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/SP500-MarketUpdate-122215-4.png[/image]

Notice that both the short and long-term moving average indicators are registering sell-signals for the first time since early 2008. However, it was several months later before the monthly moving average cross-over occurred. For many, by then, it was far too late to react.

While this time could certainly be different, there are many similarities that suggest it won’t be.

- Federal Reserve tightening monetary policy and extracting liquidity from the markets.

- Economic data weakening

- Profit margins deteriorating

- Valuations elevated

- Leadership waning

- Breadth narrowing

- Junk bond yields spiking

You get the idea. These issues, and many others, all point to a very late stage market cycle that potentially ending.

Optional Warning

Dana Lyons recently posted an interesting note on recent bearish extremes. To wit:

“Friday’s readings marked the first time ever with more than 3 put options for every call option. Today’s reading came in even more extreme at 3.3 puts for every 1 call. A look at the chart over the last 16 years illustrates truly how extreme these readings are.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/Dana-Lyons-OEX-Puts-122215.jpg[/image]

“What is so significant about those extremes in OEX open interest put/call readings? They were almost all accurate in forewarning of struggles in the stock market. In late 1999 and mid-2007, the extreme readings preceded cyclical market tops. In mid-2011, the extreme occurred prior to the sharp summer decline. And while readings in June 2003 and late 2014 did not precede major weakness, the stock market did stagnate for several months following. Perhaps only an occurrence in January 2012 proved to be a complete bust as a warning sign.

Then, there’s 2015. After 15 readings above 2.0 in 15 years, there have been no fewer than 166 readings that high so far in 2015. What gives? Either it truly is “different this time”…or this is an unprecedented red flag waving in front of us.”

Let’s “rewind the tape” for a moment and look at the highlighted portion of Dana’s commentary graphically.

The chart below is a MONTHLY chart of the S&P 500 index.

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/12/SP500-MarketUpdate-122215-5.png[/image]

1999 – High put readings lead to a market top as price momentum deteriorated, valuations were elevated and extreme market “bullishness” prevailed. Market issues monthly SELL signal in early 2000.

2003 – High readings of put options “bullish” as suppressed prices, low valuations and high market negativity set up the next bull market. Market issues monthly BUY signal in early 2003.

2007 – Valuations once again elevated, market sentiment extremely bullish and Fed tightening monetary policy expecting “Goldilocks” economy. Market issues monthly SELL signal in late 2007 as high put option readings warn of a market peak.

2012 – High readings of put options fail to signal market peak as underlying conditions not supportive. Valuations were not elevated, market sentiment was not at extremes and monetary policy was extremely accommodative as Federal Reserve pushed liquidity into the financial markets. The market was on a monthly BUY signal.

2014 – While high readings of put options did not precede a major market peak, the did foretell of the October swoon as the Federal Reserve closed out their third Quantitative easing program. However, plenty of promises of further financial support from other Central Banks and Fed officials kept markets afloat and negated the short-term readings. The market remained on a monthly BUY signal suggesting “bull” market still intact.

2015 – With the market once again on a monthly SELL signal, the record high levels of put option readings combined with high valuations, deteriorating price momentum and weakening market breadth all suggest a market forming a peak rather than starting the next bull market.

This is particularly the case now that the Fed has begun extracting liquidity from the markets and tightening monetary policy further.

However, as Dana notes:

“With OEX volume as depressed as it is now, the bearish connotations of an elevated reading in the OEX open interest put/call ratio are perhaps mitigated to a degree. Even so, when we see readings so far stretched beyond even former extreme levels, we still think it’s worthwhile to take notice.“

He is probably right.

My feeling is that if Santa does come to Wall Street, it is probably a good opportunity to get a little more defensive heading into a year that has historically lower odds of being a winner.

As an investor, you should remember that making money in the market is only one-half of the job. Keeping it is the other.

“We can not direct the wind, but we can adjust the sail.” – Anonymous