Authored by Kevin Muir via The Macro Tourist blog,

The New “Winners of the New World”

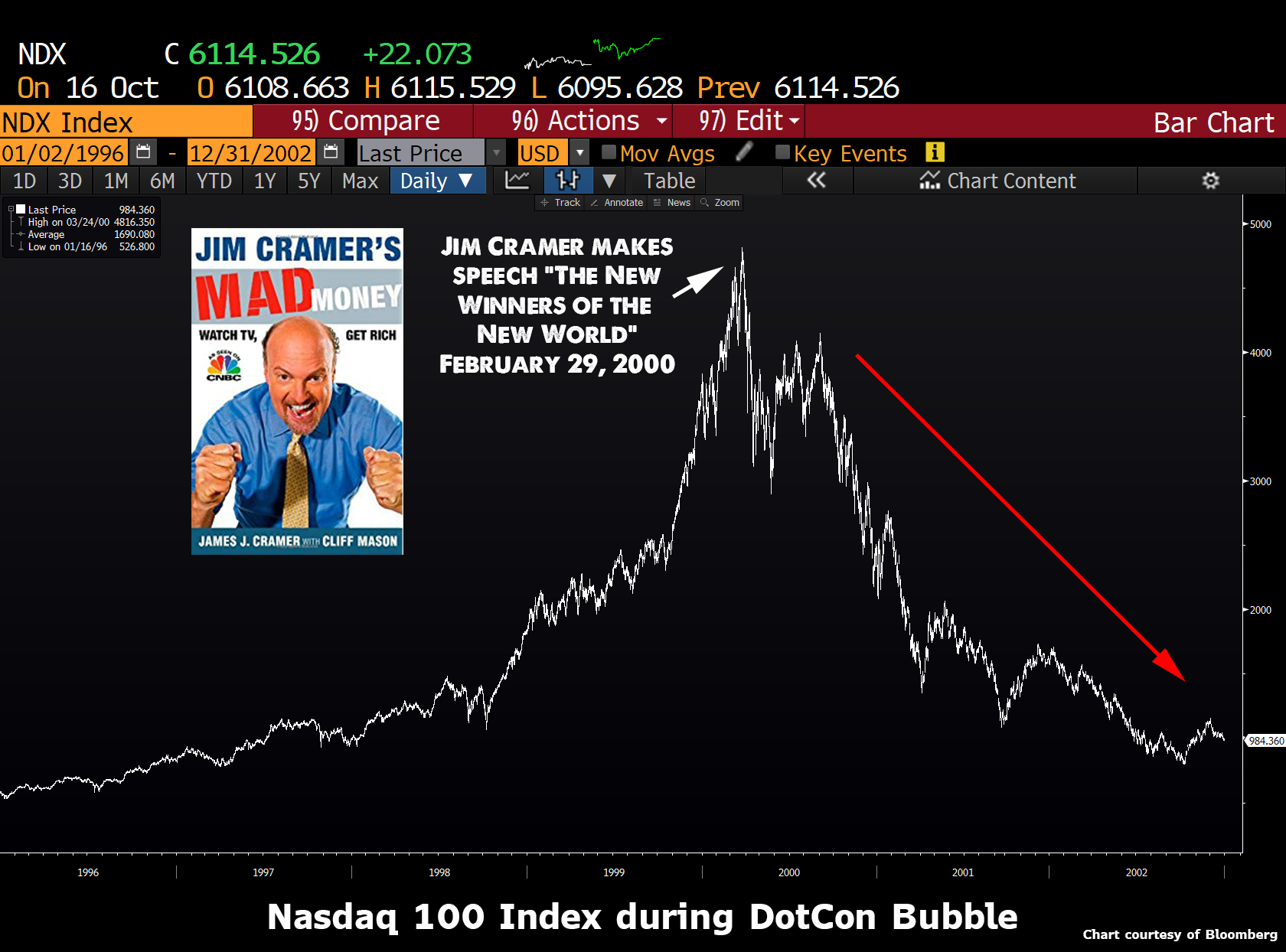

Do you remember Jim Cramer’s February 29th, 2000 speech, “Winners of the New World?

You want winners? You want me to put my Cramer Berkowitz hedge fund hat on and just discuss what my fund is buying today to try to make money tomorrow and the next day and the next? You want my top 10 stocks for who is going to make it in the New World? You know what? I am going to give them to you. Right here. Right now.

OK. Here goes. Write them down – no handouts here!: 724 Solutions ( SVNX), Ariba ( ARBA), Digital Island ( ISLD), Exodus ( EXDS), InfoSpace.com ( INSP), Inktomi ( INKT), Mercury Interactive ( MERQ), Sonera ( SNRA), VeriSign ( VRSN) and Veritas Software ( VRTS).

We are buying some of every one of these this morning as I give this speech. We buy them every day, particularly if they are down, which, no surprise given what they do, is very rare. And we will keep doing so until this period is over – and it is very far from ending. Heck, people are just learning these stories on Wall Street, and the more they come to learn, the more they love and own! Most of these companies don’t even have earnings per share, so we won’t have to be constrained by that methodology for quarters to come.

We try to own every one of them. Every single one. And if I had my druthers, I wouldn’t own any other stocks in the year 2000. Because these are the only ones worth owning right now in this extremely difficult, extremely narrow stock market. They are the only ones that are going higher consistently in good days and bad. I love every one of them, just as I loathe the rest of the stock universe.

How did this stock market get like this, to where the only people who can make a dime in it are the people who are interested in the most arcane subject, the moving of data from one space to another, via strange new machines and software? How did it get to the point where nothing else matters, most particularly the 90% of the stock market I have studied for the last 20 years? How did all of that knowledge become totally irrelevant and the only stocks that work are the stocks of companies that didn’t exist five years ago and came public in the last two or three years?

So, if you can’t own the retailers, and you can’t own transports, and you can’t own banks and brokers and financials and you can’t own commodity makers and you can’t own the newspapers, and you can’t own the machinery stocks, what can you own?

A-ha, that just leaves us with tech. That’s why we keep coming back to it. That’s why, despite the 80% increase in the Nasdaq last year, we are looking at another record year now. It is by that process of elimination that I have picked my top 10. And my next 10 and my next 10 after. Only those companies are worth owning. The rest?

You can have them.

It’s easy to laugh at Cramer today. His speech was only a couple of weeks away from the all-time high in the Nasdaq, and his 10 stocks were absolute disasters.

Yet, let me assure you - in the moment, the market was gobbling up his spiel with a zeal that is tough to describe. Cramer wasn’t some raving lunatic, but a prophet who epitomized the dotcom mania. Fading the wall of buying seemed like absolute lunacy. And for the next couples of decades, I never again saw that sort of “just get me in” panic. Until now…

Before you condemn me as some sort of perma-bear who doesn’t understand the current market, please take the time to read a couple of my pieces deriding all the bearish hedge fund managers - Betting against history, It’s too easy to write bearish pieces, or Billionaire Bears Club. I have long held the belief that a stock market melt-up was just as likely as crash.

But I have a problem. I hate being in the majority. It was easy for me to speak about the possibility of a stock market spike higher when everyone was bearish. Yet the trader in me cannot stand sticking with that position in the midst of an epic squeeze.

I don’t think the market will crash (although with every passing day the froth scares me more and more.) So I am not some doomsdayer predicting some catastrophic disaster. Yet I am a trader that knows markets look best at the top.

Back to Jim Cramer’s speech at the peak of the Nasdaq madness. Yesterday one of my favourite market pundits wrote a piece that was so eerily reminiscent of Cramer’s “the inevitability of dot com stocks to levitate to the moon” fame, I had to double check the author’s credits. I think Josh Brown from Reformed Broker fame is indisputably one of the good guys, and he has correctly remained steadfastly bullish in the midst of every hedge fund hyperventilation of the coming crash. Yet I respectfully have to take the other side of Josh’s Just Own the Damn Robots piece.

Take a moment to read Josh’s post. It’s compelling, well written, and makes you want to run out and write some big blue tickets.

In Kurt Vonnegut’s 1952 novel, Player Piano, we are introduced to a future in which only engineers and managers have gainful employment and meaningful lives. If you’re not one of the engineers and managers, then you’re in the army of nameless people fixing roads and bridges. You live in Homestead, far from the machines that do everything, and are treated throughout your life like a helpless baby. The world no longer has a use for you. Anything you can do a machine can do better, and you are reminded of this all day, every day by society and the single omnipotent industrial corporation that oversees it all.

He wrote this 65 years ago. It couldn’t have been more apropos to what we’re witnessing now than if had he written it this morning, right down to the nostalgia-selling demagogue who seizes the opportunity to foment rebellion amongst the displaced and disgruntled. When millions of people start seeing their purpose begin to erode and their dignity being stolen from them, the idea that there’s nothing left to lose starts to creep in.

In the book, the result is a violent rebellion against the machines. In the real world, we’ve resigned ourselves to investing in them instead.

We could be in the midst of the first fear-based investment bubble in American history, with the masses buying in not out of avarice, but from a mentality of abject terror. Robots, software and automation, owned by Capital, are notching new victories over Labor at an ever accelerating rate. It’s gone parabolic in recent years - every industry, every region of the country, and all over the world. It’s thrilling to be a part of if you’re an owner of the robots, the software and the automation. If you’re a part of the capital side of that equation. If you’re on the other side, however - the losing side - it’s a horror movie in slow motion.

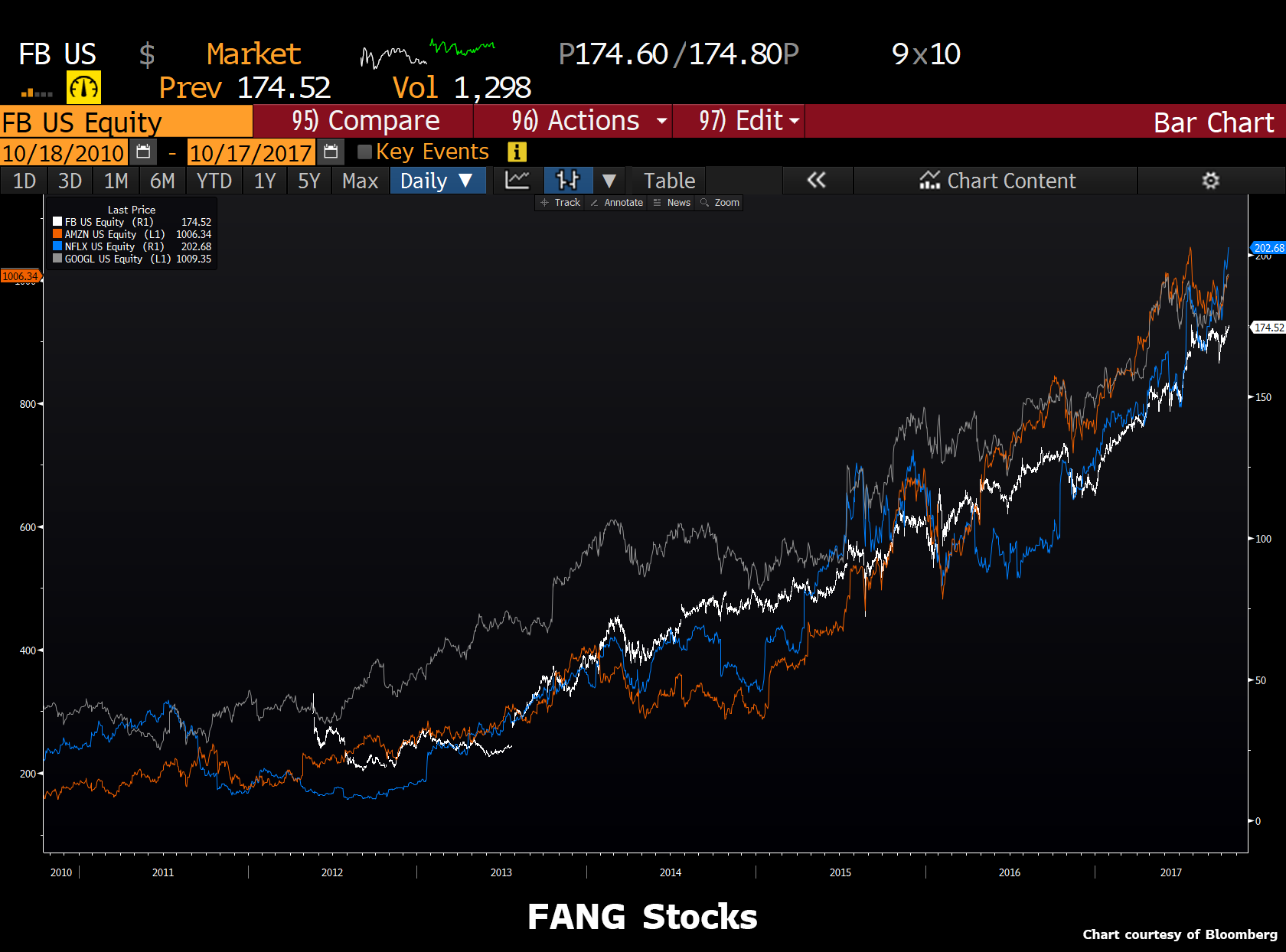

The only way out? Invest in your own destruction. In this context, the FANG stocks are not a gimmick or a fad, they’re a f***ing life raft. Market commentators rhetorically ask aloud what multiple should investors pay to own the technology giants. That’s the wrong question when people feel like they’re drowning.

What multiple would you pay to survive? Grab a raft.

This sort of “it doesn’t matter what you pay for an asset” is the type of thinking that prevails at tops. The idea of a new paradigm also permeates market participants’ thinking:

The disruptor’s credo, say it with me: Your profit margin is my opportunity. Put another way: Your profitable small business is basically a market failure. But only for now, because we’ve got investors, motherf***er.

Friend of a friend owns a small chain of grocery stores in New Jersey. A few years ago, when Amazon got into groceries, he changed his mind about investing in the growth of his own business. He started buying Amazon shares with his investment capital instead. He saw what happened to Circuit City and Tower Records, Borders and Barnes & Noble. So he bought some Amazon and then he bought some more.

This wasn’t retirement investing. This was something else. What should we call it? Disruption Insurance?

I don’t know. Anyway, long story short, Amazon is up over a thousand percent over the last ten years, and he don’t need the stores no more.

Of the people actively looking for jobs right now, 96% of them are currently employed, as of the latest labor report. This, of course, excludes tens of millions of working age folks who have stopped looking, are working off the books or who have otherwise just given up. A great deal of them come from industries or vocations that no longer exist. This is not a new phenomenon, it’s been going on since the beginning of time.

What is undeniable, however, is that the pace of this process has increased to breakneck speed. It also seems to be perennially advantaging those for whom advantage has already accrued. Winners keep winning. A momentum strategy, but for people. You would expect the folks on Wall Street to be celebrating all time record highs for asset prices. It’s the opposite - it’s making them miserable. Head counts and fund closures are this bull market’s accoutrements, not lavish parties and cocaine. It’s never been like this before.

For the last fifty years, we’ve invested for retirement. For the last two or three years, we might be investing for a whole other reason. What price is too high to pay for a company’s stock if the company spends every waking minute trying to replace you?

So what else is left to do? Just own the damn robots.

Owning an asset regardless of price is what created the dotcom bubble. It didn’t work then, and it won’t work now. Chasing momentum after an epic 5-year monster bull run, regardless of how compelling the narrative, is not my idea of smart investing. Let’s see - feverish froth, frantic “I will miss the new era” buying and New Yorker magazine covers that reek of “even my Grandmother is now aware of this trend” is not a great setup.

So although Josh’s words seem convincing, remember that Jim Cramer’s recommendations once seemed just as wise. Josh’s advice has been spot on for quite some time, but I wonder if he isn’t a little overconfident with this latest piece. I just can’t help but feel that this is the sort of stuff you see near the top.

* * *

Chinese stability operation

After my piece last week, More Ways to Get into Trouble, that speculated a stock market correction was not coming until after the Chinese Communist Party Congress concluded, a kind reader sent this picture from the Shenzhen Securities Exchange building.

According to my source, this banner was put up one week before the 19th national congress of the communist party of China. It reads - “Use every effort to protect the stability of stock market for 20 days.”

One more week to go. October 25th is the last day of the congress.

Even if you buy Josh Brown’s secular bull argument, think about hanging tough. I still contend you will get a better entry point in the next couple of months.

* * *

Saudi Aramco negotiations

Over the past year, I have watched as market pundits floated all sorts of theories about Saudi Arabia’s devious plans regarding the floating of the world’s largest IPO in their state-controlled energy company, Saudi Aramco. Some readers asked my opinion, and I was quick to admit, I didn’t have a clue. I was unsure what I was seeing. Was Saudi Arabia keeping the price of oil down ahead of the IPO, so they could raise it later? Or were they trying to goose it higher to sell their company at the best possible price today? Who knows? And although it was fun to speculate, the reality is that it was really a negotiating process whose progress was known only to the few market players that were setting the price.

But yesterday Reuters reported a new tidbit of information that changed the landscape.

Chinese state-owned oil companies PetroChina (0857.HK) and Sinopec (0386.HK) have written to Saudi Aramco in recent weeks to express an interest in a direct deal, industry sources told Reuters. The companies are part of a state-run consortium including China’s sovereign wealth fund, the sources say.

Saudi Arabia’s Crown Prince Mohammed bin Salman said last year the kingdom was considering listing about 5 percent of Aramco in 2018 in a deal that could raise $100 billion, if the company is valued at about $2 trillion as hoped.

“The Chinese want to secure oil supplies,” one of the industry sources said. “They are willing to take the whole 5 percent, or even more, alone.”

PetroChina and Sinopec declined to comment.

No shit PetroChina and Sinopec declined to comment, they are probably pissed as hell that this story leaked.

You know how I know that? I have seen this movie before. It’s a negotiating tactic as old as the hills.

Let me tell you about my first time seeing this play out. It was in the 1990’s and I was a young kid sitting on Canada’s largest equity institutional desk. Our bank has done a “bought deal” where we had committed to buy a large piece of stock from an issuer before knowing whether we would be able to place it with our clients. The company pasted us with the deal, and it quickly became obvious that we were hung. The issue didn’t sell at our price, and the next morning, the stock opened below our cost.

I watched as our head trader calmly monitored the price of the issue, but kept a stone face for everyone on the desk. I can’t remember how much we were offside. It was a big number. Not the hundreds of millions the Wall Street boys played with, but we were offside many tens. It stung, and even though I was young and naive, it didn’t take much to deduce from the worried whispers that this was going to hurt the paycheque.

Well, some banks would cave and take the loss, but not my shop. Not sure if it was dumb or brave (probably a little of both), but management sat with that position for a few weeks. During this time, the market rallied, but our stock did not budge as the whole street knew we were wearing this huge piece. Day by day we sat there watching other comparables rally hard, while our stock refused to get off the mat.

I distinctly remember the calmness of our head trader. It sure seemed hopeless, but he kept a smile on his face and did not seem even a quarter as worried as the other traders on the desk.

Then one day, it happened. I can still remember it as if it was yesterday. Most of our phone lines were direct lines to the traders that sat at our institutional clients’ desks. But we had a few “overhead” lines when others wanted to call in.

One of the traders picked up a blinking light, listened to the other end, and then cupped his hand to the mic before shouting out across the desk, “Paul, Beaverton Pension Plan PM wants to talk to you directly. What overhead number should I tell him?” (we don’t really have firms called Beaverton Pension Plan - we are hick, but we keep beavers on our money, not in our financial firm names.)

Our head trader grinned, and waited for the call to come in. After a few minutes of hushed conversation, he hung up the line and barked out instructions:

“Bobby, buy up everything on the board up to our issue price. Then bid for another 2 million out loud. For the rest of you, the issue is gone. Beaverton took the whole thing, and we come out a better buyer. We pay issue price for 3 million more.”

It was only later that I understood what happened. Beaverton had realized the stock was undervalued. It should have been rallying, but the worry about the overhang of supply had kept it down. Realizing that it was only a matter of time before market players started buying smaller amounts, Beverton decided to pro-actively take advantage of the situation.

They bid our head trader for the whole piece “all or nothing.” They had actually started trying to get him to break price, but when he held tough, they settled with buying it all.

All the other clients who had held off buying the stock because they “knew it wasn’t going up because of the huge slug of overhang”, suddenly found themselves needing to buy a cheap stock with no size offerings anywhere near the quote. It turned into a food fight with the stock instantly rocketing higher.

The truth of the matter was that most clients were pissed. They figured they had us by the short and curlies, and when we turned the table, they took it out by screaming that we screwed them. We would have preferred Beaverton to have shared the print, but the reality is that once the market realized the piece was cleaning up, everyone would have “me too’ed” the trade (they would have all given us orders to buy along with Beaverton. Canadian institutional clients are notorious “me too’ers”). If that had happened, then Beaverton would have gotten significantly less. They paid up, and they deserved the whole piece.

My suspicion is that the same dynamic is happening today with the Saudi Aramco deal. Recognizing that the pricing has reached a level that might be too low, the Chinese had indicated a willingness to skip the whole IPO process, and simply take the whole piece. They were trying to replicate Beaverton’s move.

Saudi Arabia has leaked the story to get the other buyers to pay up. But the truth of the matter is that this is dangerous game to play. If China walks away, the Saudis will be left with a much lower price.

I still don’t have a clue about the status of the negotiations. But rest assured, they are playing games. The negotiations will appear like they are going nowhere, and then suddenly it will all be over.