Submitted by Wolf Richter via WolfStreet.com,

This wasn’t part of the rosy scenario.

The Merchandise World Trade Monitor by the CPB Netherlands Bureau for Economic Policy Analysis, a division of the Ministry of Economic Affairs, tracks global imports and exports in two measures: by volume and by unit price in US dollars. And the just released data for January was a doozie beneath the lackluster surface.

The World Trade Monitor for January, as measured in seasonally adjusted volume, declined 0.4% from December and was up a measly 1.1% from January a year ago. While the sub-index for import volumes rose 3% from a year ago, export volumes fell 0.7%. This sort of “growth,” languishing between slightly negative and slightly positive has been the rule last year.

The report added this about trade momentum:

Regional outcomes were mixed. Both import and export momentum became more negative in the United States. Both became more positive in the Euro Area. Import momentum in emerging Asia rose further, whereas export momentum in emerging Asia has been negative for four consecutive months.

This is also what the world’s largest container carrier, Maersk Lines, and others forecast for 2016: a growth rate of about zero to 1% in terms of volume. So not exactly an endorsement of a booming global economy.

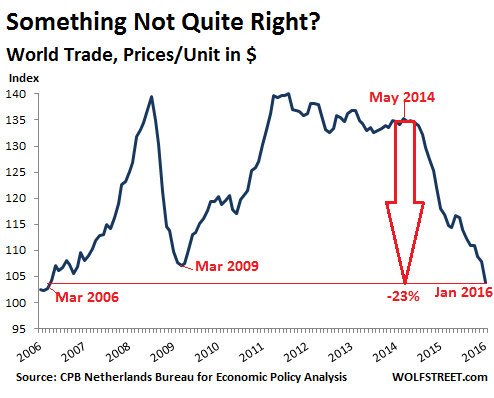

But here’s the doozie: In terms of prices per unit expressed in US dollars, world trade dropped 3.8% in January from December and is down 12.1% from January a year ago, continuing a rout that started in June 2014. Not that the index was all that strong at the time, after having cascaded lower from its peak in May 2011.

If June 2014 sounds familiar as a recent high point, it’s because a lot of indices started heading south after that, including the price of oil, revenues of S&P 500 companies, total business revenues in the US…. That’s when the Fed was in the middle of tapering QE out of existence and folks realized that it would be gone soon. That’s when the dollar began to strengthen against other key currencies. Shortly after that, inventories of all kinds in the US began to bloat.

Starting from that propitious month, the unit price index of world trade has plunged 23%. It’s now lower than it had been at the trough of the Financial Crisis. It hit the lowest level since March 2006:

This chart puts in perspective what Nils Andersen, the CEO of Danish conglomerate AP Møller-Maersk, which owns Maersk Lines, had said last month in an interview following the company’s dreary earnings report and guidance: “It is worse than in 2008.” [Read… “Worse than 2008”: World’s Largest Container Carrier on the Slowdown in Global Trade.]

But why the difference between the stagnation scenario in world trade in terms of volume and the total collapse of the index that measures world trade in unit prices in US dollars?

The volume measure is a reflection of a languishing global economy. It says that global trade may be sick, but it’s not collapsing. It’s worse than it was in 2011. This sort of thing was never part of the rosy scenario. But now it’s here.

The unit price measure in US dollars is a reflection of two forces, occurring simultaneously: the collapsed prices of the commodities complex, ranging from oil to corn; and the strength of the US dollar, or rather the weakness of certain other currencies, particularly the euro. It didn’t help that since last summer, the Chinese yuan has swooned against the dollar as well. So exports and imports from and to China, measured in dollars, have crashed further than when measured in yuan.

And these forces coagulated at a time of lackluster global demand despite, or because of, seven years of QE, zero-interest-rate policies, and now negative-interest-rate policies. It forms another indictment of central bank policies that have failed to stimulate demand though they have succeeded wonderfully in stimulating asset prices, malinvestment, and overcapacity.

World trade in goods is just one factor in the global economy. Now the global financial sector is getting hit too as the artful QE bonanza is bumping into real-world limits. And for global investment banking revenues, a key income source for “systemically important” banks, it has been one heck of a terrible first quarter. Read… The Big Unwind Hits Investment Banking