Submitted by Lance Roberts via RealInvestmentAdvice.com,

Recently, my article on weak economic underpinnings led to an interesting exchange, via Twitter, with Steve Chapman regarding debt and the impact on economic growth.

The question is: Does rising debt cause slow growth or does slow growth cause debt to rise? https://t.co/CLDQnoyUBu

— Steve Chapman (@SteveChapman13) February 12, 2016

This question has been a point of contentious debate over the last several years as debt levels in the U.S. have soared higher.

According to Keynesian theory, some microeconomic-level actions, if taken collectively by a large proportion of individuals and firms, can lead to inefficient aggregate macroeconomic outcomes, where the economy operates below its potential output and growth rate (i.e. a recession).

Keynes contended that “a general glut would occur when aggregate demand for goods was insufficient, leading to an economic downturn resulting in losses of potential output due to unnecessarily high unemployment, which results from the defensive (or reactive) decisions of the producers.” In other words, when there is a lack of demand from consumers due to high unemployment, the contraction in demand would force producers to take defensive actions to reduce output.

In such a situation, Keynesian economics states that government policies could be used to increase aggregate demand, thus increasing economic activity and reducing unemployment and deflation. Investment by government injects income, which results in more spending in the general economy, which in turn stimulates more production and investment involving still more income and spending and so forth. The initial stimulation starts a cascade of events, whose total increase in economic activity is a multiple of the original investment.

Keynes’ was correct in his theory. In order for government deficit spending to be effective, the “payback” from investments being made through debt must yield a higher rate of return than the debt used to fund it.

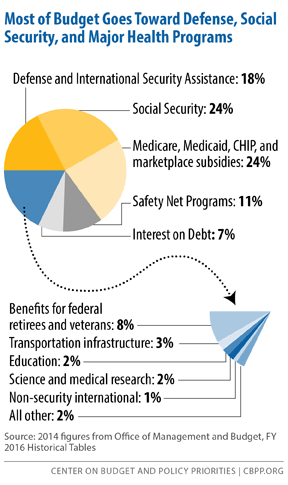

The problem is that government spending has shifted away from productive investments that create jobs (infrastructure and development) to primarily social welfare and debt service which has a negative rate of return. According to the Center On Budget & Policy Priorities nearly 75% of every tax dollar goes to non-productive spending.

Here is the real kicker, though. In 2014, the Federal Government spent $3.5 Trillion which was equivalent to 20% of the nation’s entire GDP. Of that total spending, $3.15 Trillion was financed by Federal revenues and $485 billion was financed through debt. In other words, it took almost all of the revenue received by the Government just to cover social welfare and service interest on the debt. In the financial markets, when you borrow from others to pay obligations you can’t afford it is known as a “Ponzi-scheme.”

Debt Is The Cause, Not The Cure

Debt, if used for productive investments, can be a solution to stimulating economic growth in the short-term. However, in the U.S., debt has been squandered on increase in social welfare programs and debt service which has an effective negative return on investment. Therefore, the larger the balance of debt becomes, the more economically destructive it is by diverting an ever growing amount of dollars away from productive investments to service payments.

The relevance of debt growth versus economic growth is all too evident as shown below. Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. With economic growth rates now at the lowest levels on record, the growth in debt continues to divert more tax dollars away from productive investments into the service of debt and social welfare.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-GDP-Presdient-022216.png[/image]

It now requires $3.71 of debt to create $1 of economic growth.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-GDP-Growth-022216.png[/image]

In fact, the economic deficit has never been greater. For the 30-year period from 1952 to 1982, the economic surplus fostered a rising economic growth rate which averaged roughly 8% during that period. Today, with the economy growing at an average rate of just 2%, the economic deficit has never been greater.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-Economic-Deficit-022216.png[/image]

But it isn’t just Federal debt that is the problem. It is all debt.

When it comes to households, which are responsible for roughly 2/3rds of economic growth through personal consumption expenditures, debt was used to sustain a standard of living well beyond what income and wage growth could support. This worked out as long as the ability to leverage indebtedness was an option. The problem is that eventually, the debt reaches a level where the level of debt service erodes the ability to consume at levels great enough to foster stronger economic growth.

In reality, the economic growth of the U.S. has been declining rapidly over the past 35 years supported only by a massive push into deficit spending by households.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-Total-GDP-022216.png[/image]

What was the difference between pre-1980 and post-1980?

From 1950-1980, the economy grew at an annualized rate of 7.70%. This was accomplished with a total credit market debt to GDP ratio of less 150%. The CRITICAL factor to note is that economic growth was trending higher during this span going from roughly 5% to a peak of nearly 15%. There were a couple of reasons for this. First, lower levels of debt allowed for personal savings to remain robust which fueled productive investment in the economy. Secondly, the economy was focused primarily on production and manufacturing which has a high multiplier effect on the economy. This feat of growth also occurred in the face of steadily rising interest rates which peaked with economic expansion in 1980.

The obvious problem is the ongoing decline in economic growth over the past 35 years has kept the average American struggling to maintain their standard of living. As wage growth stagnates or declines, consumers are forced to turn to credit to fill the gap in maintaining their current standard of living. However, as more leverage is taken on, the more dollars are diverted from consumption to debt service thereby weighing on stronger rates of economic growth.

Austrians Might Have It Right

The massive indulgence in debt, what the Austrians refer to as a “credit induced boom”, has now reached its inevitable conclusion. The unsustainable credit-sourced boom, which leads to artificially stimulated borrowing, seeks out diminishing investment opportunities. Ultimately these diminished investment opportunities lead to widespread mal-investments. Not surprisingly, we clearly saw it play out “real-time” in everything from sub-prime mortgages to derivative instruments which was only for the purpose of milking the system of every potential penny regardless of the apparent underlying risk.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-Austrian-Theory-022216.png[/image]

When credit creation can no longer be sustained the markets must begin to clear the excesses before the cycle can begin again. It is only then, and must be allowed to happen, can resources be reallocated back towards more efficient uses. This is why all the efforts of Keynesian policies to stimulate growth in the economy have ultimately failed. Those fiscal and monetary policies, from TARP and QE to tax cuts, only delay the clearing process. Ultimately, that delay only potentially worsens the inevitable clearing process.

That clearing process is going to be very substantial. The economy is currently requiring roughly $4 of debt to create $1 of economic growth. A reversion to a structurally manageable level of debt would involve a nearly $30 Trillion reduction of total credit market debt from current levels.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-Structurally-Maintainable-Level-022216.png[/image]

The economic drag from such a reduction would be a devastating process which is why Central Banks worldwide are terrified of such a reversion. In fact, the last time such a reversion occurred the period was known as the “Great Depression.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Debt-GDP-Annual-022216.png[/image]

This is one of the primary reasons why economic growth will continue to run at lower levels going into the future. We will witness an economy plagued by more frequent recessionary spats, lower equity market returns and a stagflationary environment as wages remain suppressed while costs of living rise.

Correlation or causation? You decide.