Submitted by 720Global's Michael Lebowitz via RealInvestmentAdvice.com,

In “Passive Negligence”, we highlighted how investors, on the margin, have been shifting from an active investment style to a more passive approach by favoring index and sector ETFs and mutual funds over individual holdings. We raised a concern that, in this mad dash towards the latest fad, many investors are falling prey to complacency by failing to properly analyze the underlying companies in which they are ultimately investing.

Since Donald Trump won the election, the Russell 2000 (R2K) has been the darling of the market, increasing approximately 15%. There are many narratives that support investing in small cap stocks, as represented by the R2K, and some even have credence. That said, investors should look beyond these narratives and analyze the index’s current valuation and its underlying holdings to better judge if the R2K is a good investment.

This article was written in conjunction with J. Brett Freeze, CFA from Global Technical Analysis.

The Russell 2000

Passive investors looking to diversify their equity holdings frequently hold a number of ETFs and mutual funds that blindly follow an index or sector. Many investment professionals employ a similar approach called “closet indexing”. In other words, they own a portfolio of different equity indices and some specific sectors as a decoy to their clients. They want the appearance of providing real value by generating alpha through security selection and not simply buying the “market”. Typically such strategies, over time, provide market-like returns and little diversification.

The R2K, in the words of Wikipedia, is “by far the most common benchmark for mutual funds that identify themselves as small cap”. Therefore, the R2K is a favorite among “closet indexers” looking to diversify their portfolios with small-cap holdings.

Like many broad-based indices, the R2K is composed of a diverse group of companies from varying industries. Currently, technology, services, healthcare and financials account for approximately 75% of the market capitalization of the index.

The following aggregate analysis of the R2K decomposes the index into nine industry classifications as well as a small catch-all category for unclassified companies. The current index constituents were held constant over the 13 year period that we reviewed. In other words, the data analyzed assumes the companies currently in the R2K, were in it for the last 13 years. This method allows for a more consistent evaluation of the index as it is currently composed. Note that 34 of the index constituents were excluded from this analysis as no data was available. The data used in this analysis is courtesy of www.gurufocus.com.

Net Income

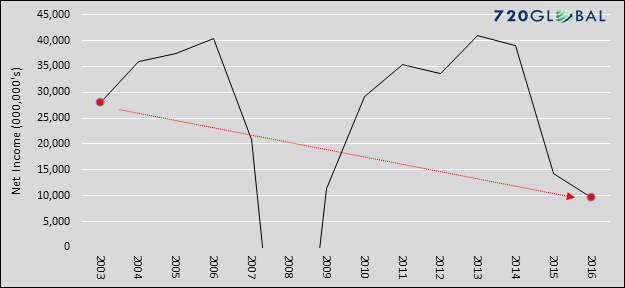

Over the last five years, the R2K’s aggregate annual net income has shrunk from $33.6 billion to $9.7 billion, a 73% decline. That compares with nominal GDP growth of +18% and a 1% decline in S&P 500 earnings growth over the same period. Of the nine industries and the catch-all category that comprise the R2K, only four have experienced income growth over the last five years. Even more interesting is that 83% of the R2K’s earnings growth over the last five years is from one sector, financials. Exclude financial companies from the index, aggregate earnings have been negative in each of the last two years. The chart below highlights the declining trend in R2K earnings since 2003, which marks the start of the market’s recovery from the Technology crash.

R2K earnings, as highlighted above, have declined at an annualized rate of 7.81% despite the 4.15% annualized earnings growth of financial companies.

Market Capitalization

Market Capitalization, also known as market cap, is the aggregate value of the equity shares underlying the index at a specific point in time. Currently, the R2K’s market cap stands at $2.311 trillion. Financial companies comprise the largest share at 25.4%, followed by technology (17.5%) and services (16.8%). Over the last five years, as shown in the graph below, the market cap of the R2K has nearly doubled, rising 91% despite declining earnings over the same period.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/12/income-market-cap-graph.png[/image]

As the R2K’s market cap steadily increases and earnings fail to follow, the valuation of the index naturally richens. In particular, note the last two years in which the market cap increased despite a sharp decline in earnings. Currently, the ratio of market cap to net income is at an astronomical 237x, significantly above the post-2003 average of 33x. Holding earnings constant and regressing the index back to its post-2003 mean, market cap to earnings ratio would produce an 86% decline in the R2K. Even in an optimistic scenario, where earnings rebound to the high water mark of $40.90 billion set in 2013, the R2K would need to decline by 42% from its current level to produce a market cap to earnings ratio of 33x.

As a point of comparison, the widely reported P/E ratio of 46 for the R2K appears to be much lower than our value (237x). Unlike, the market benchmark S&P 500, the reported Russell P/E ratio excludes companies with negative earnings. Our analysis appropriately includes both positive and negative earnings.

What is the Russell?

Thus far, we have shown the paltry earnings growth of the R2K and the unsubstantiated rise in its market cap. To try to make more sense of this conflict we return to a point made earlier: financial companies have provided 83% of all the earnings in the R2K over the last five years. From a fundamental perspective, an investor in the R2K has relied almost entirely upon earnings from financial companies, but has retained exposure to three-quarters of the index which have produced negligible aggregate earnings. In other words, investors are paying a steep premium for what amounts to earnings exposure from financial stocks.

The KBW bank index is a popular benchmark for the performance of domestic regional banks. Unlike the major national banks, such as J.P. Morgan and Bank of America, these banks are smaller in size, have less global exposure, and do a majority of their business in specific regions of the country. The largest banks in the index are household names such as KeyCorp, M&T Bank and BB&T Corporation. Some of the lesser-known banks are Berkshire Hills Bancorp, Hanmi Financial Corporation, and Cardinal Financial Corporation. Nearly 65% of the stocks in the KBW index are included in the R2K index.

Passive investors could have extracted a large portion of the fundamental benefits of owning the R2K by purchasing the KBW index. In substituting KBW for R2K, they would have retained similar exposure to financials while avoiding a portfolio of additional stocks trading at extreme valuations. The financial stocks within the R2K currently have a market cap to income ratio of 22.2, well below the 237.4 ratio of the entire index.

The table below compares the results of R2K and KBW. We used popular ETF’s to replicate investor performance of the two indices – IWM (R2K) and KRE (KBW).

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/12/table.png[/image]

KBW outperformed the R2K on an annualized return basis over the last two and five year periods and provided better risk-adjusted returns.

Having identified a meaningful anomaly, the next question is how can an investor or portfolio manager capitalize on it? For those who already own the R2K and are comfortable with market valuations, the recommendation would be to replace the R2K with a combination of the S&P 500, Wilshire 5000 and the KBW banking index. The Wilshire 5000 also provides some small cap exposure, but at comparatively reasonable valuations. For those looking to exploit what seems like a mispricing of the R2K, we recommend a paired trade approach whereby one shorts the R2K and goes long the KBW and the S&P 500.

Summary

Much of the recent post-election price appreciation in the R2K has been based on the performance of financial stocks. The KBW index, again solely a financial stock portfolio, is up approximately 25% since the election, compared with 15% for the broader R2K. The recent appreciation in financials is apparently a response to the new administration’s planned policies that are generally viewed as beneficial for the financial sector. Given the regulatory oppression of the past eight years, this may very well be a sound reason to own bank stocks. However, the R2K index is trading at grossly elevated levels. Owning the index for anything other than pure speculative trading is ridiculous. Owning the index for its bank exposure is insane.

Active investment may not be in style, but that is certainly no reason to ignore sound analytical rigor and proper logic in making prudent investment allocation decisions.

* * *

Just for a little more color on how insane this move has been... here are speculative longs in Russell 2000 futures...

h/t Loic S.