Authored by 720Global's Michael Liebowitz via RealInvestmentAdvice.com,

“Before long, we will all begin to find out the extent to which Brexit is a gentle stroll along a smooth path to a land of cake and consumption.” – Mark Carney, Bank of England Governor

In 1939, the British Government, through the Ministry of Information, produced a series of morale-boosting posters which were hung in public places throughout the British Isles. Faced with German air raids and the imminent threat of invasion, the slogans were aimed at helping the British public brave the testing times that lay ahead. The most enduring of these slogans simply read:

“Keep Calm and Carry On.”

Ironically, it was the only one of the series that was never actually displayed in public as it was reserved for a German invasion that never transpired. Today, the British Government may wish to summon a fresh propaganda strategy to address a new threat on the horizon, that of the eventuality of Brexit.

The Kingdom Divided

The United Kingdom (UK) is in the process of negotiating out of all policies that, since 1972, formally tied it to the economic dynamics of the broader western European community. Since the unthinkable Brexit vote passage in June 2016, the unthinkable has now become the undoable. The negotiations, policy discussions, logistical considerations and legal wrangling are becoming increasingly problematic as they affect every industry in the UK from trade and finance to hazardous materials, produce, air travel and even Formula 1 racing.

The worst case scenario of a disorderly or “hard” Brexit, whereby no deal is reached by the March 2019 deadline, is the most extreme for investors along the spectrum of potential outcomes. A deadlock, which is unfortunately the most likely scenario, would result in tariffs on trade between the UK and the European Union (EU). Such an outcome would result in a rapid deterioration of British economic prospects, job losses and the migration of talent and businesses out of the country. Even before the path of Brexit is known, a number of large companies with UK operations, including Barclays Bank, Diageo, Goldman Sachs, and Microsoft, are discussing plans to move or are already actively moving personnel out of Britain. Although less pronounced, the impact of a “hard” Brexit on the EU would not be positive either.

The least damaging Brexit outcome minimizes costs and disruption to business and takes the form of agreement around many of the key issues, most notably the principle of the freedom of movement of labor. The current progression of events and negotiations suggests such an agreement is unlikely. The outcome of negotiations between the UK and the EU will be determined by politics, with the UK seeking to protect its interests while the EU and its 27 member states negotiate to protect their own.

To highlight the complexities involved, the challenges associated with reaching agreements, and why a hard Brexit seems most likely, consider the following:

- Offering an early indication of the challenges ahead, German Prime Minister Angela Merkel stated that she wants the “divorce arrangement” to be agreed on before terms of the future relationship are negotiated. The UK has expressed a desire for these negotiations to run concurrently

- A withdrawal agreement (once achieved) would need to be ratified by the UK

- A withdrawal agreement would have to be approved by the European Parliament

- A withdrawal agreement would have to be approved by 20 of the 27 member states

- The 20 approving states must make up at least 65% of the population of the EU or an ex-UK population of 290 million people

- If the deal on the future relationship impacts policy areas for which specific EU member states are primarily responsible, then the agreement would have to be approved by all the national parliaments of the 27 member states

The summary above shows that the unprecedented amount of coordination and negotiation required within the 27 member states and between the EU Commission, the EU Council and the EU Parliament, to say nothing of the UK.

The “do nothing and see what happens” stance taken by the British and the EU would likely deliver a unique brand of instability but one for which there is a precedent.

The last time we observed an economic event unfold in this way, investment firm Lehman Brothers disappeared along with several trillion dollars of global net worth. Although the Lehman bankruptcy was much more abrupt and less predictable, a hard Brexit seems likely to similarly roil global markets. The “no deal” exit option, which is the path currently being followed, threatens to upend the intricate and endlessly interconnected system of global financial arbitrage. Markets are complacent and seem to have resigned themselves to the conclusion that since no consequences have yet emerged, then they are not likely.

Lehman Goes Down

In late 2007 and early 2008, as U.S. national housing prices were falling, it was becoming evident that the financial sector was in serious trouble. By March of 2008, Bear Stearns was sold to JP Morgan for $2 per share in a Fed-arranged transaction to stave off bankruptcy. Bear Stearns stock traded at $28/share two days before the transaction and as high as $172 per share in January 2007. Even as evidence of problems grew throughout the summer of 2008, investors remained complacent. After the Bear Stearns failure, the S&P 500 rallied by over 14% through mid-May and was still up over 3% by the end of August following the government seizure of Fannie Mae and Freddie Mac. While investors were paying little attention, the solvency of many large financial entities was becoming more questionable. Having been denied a Federal Reserve backstop, Lehman failed on September 15, 2008 and an important link in the global financial system suddenly disappeared. The consequences would ultimately prove to be severe.

On September 16, 2008, the first trading day after Lehman Brothers filed for bankruptcy, the S&P 500 index closed at 1192. On September 25, just 10-days later, it closed 1.43% higher at 1209. The market, in short time, would eventually collapse and bottom at 666 in six short months. Investors’ inability to see the bankruptcy coming followed by an inability to recognize the consequences of Lehman’s failure seems eerily familiar as it relates to the current status of Brexit negotiations.

If all efforts to navigate through Brexit requirements are as complicated and difficult as currently portrayed, then what are we to expect regarding adverse consequences when the day of reckoning arrives? Is it unfair to suspect that the disruptions are likely to be severe or potentially even historic? After all, we are not talking about the proper dissolution of an imprudently leveraged financial institution; this is a G10 country! The parallel we are trying to draw here is not one of bankruptcy, it is one of disruptions.

As it relates to Brexit, Dr. Andreas Dombret, member of the executive board of the Deutsche Bundesbank, said this in a February 2017 speech to the Bank of International Settlements –

“So while economic policy will of course be an important topic during negotiations, we should not count on economic sanity being the main guiding principle. And that means we also have to factor in the possibility that the UK will leave the bloc in 2019 without an exit package, let alone the sweeping trade accord it is seeking. The fact that this scenario would most probably hurt economic activity considerably on both sides of the Channel will not necessarily prevent it from happening.”

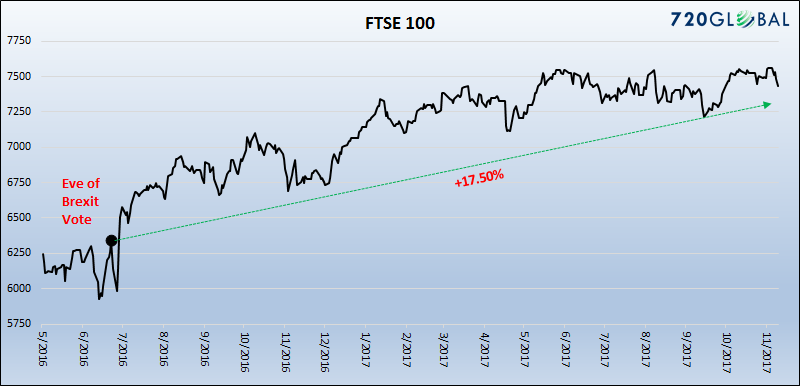

Rhyming

On June 23, 2016, the day before the Brexit vote, the FTSE 100 closed at 6338. After a few hours of turbulence following the surprising results, the FTSE recovered and by the end of that month was up 2.6%. Today, the index is up 17.5% from the pre-Brexit close. The escalating risks of a hard exit from the EU clearly are not priced into the risky equity markets of Great Britain.

Data Courtesy: Bloomberg

Conversely, what has not recovered is the currency of the United Kingdom (chart below). The British Pound Sterling (GBP) closed at 1.4877 per U.S. dollar on June 23, 2016, and dropped by 15 points (-10%) to 1.33 by the end of the month following the Brexit vote. Over the past several months the pound has fallen to as low as 1.20 but more recently it has recovered to 1.33 on higher inflation readings and hawkish monetary policy language from Bank of England (BoE) governor Mark Carney. Despite following through on his recent threats to hike interest rates, the pound has begun to again trend lower.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/11/2-gbp.png[/image]

Data Courtesy: Bloomberg

Carney has voiced concern over Brexit-induced inflation by saying that if global integration in recent decades suppressed price growth then the reduced openness to foreign markets and workers due to Brexit should result in higher inflation. This creates a potential problem for the BoE as a disorderly exit from the EU hurts the economy while at the same time inducing inflation. Such a stagflation dynamic would impair the BoE’s ability to engage in meaningful monetary stimulus of the sort global financial markets have become accustomed since the financial crisis. If the central bankers lose control of inflation, QE becomes worthless.

Some astute observers of the currency markets and BoE pronouncements argue that Carney’s threat of rate hikes are aimed at halting the deterioration of value in the pound and preventing a total collapse of the currency. That theory is speculative but plausible when analyzing the chart. Either way, whether the pound’s general weakness is driven by inflation concerns or the rising risks associated with a hard Brexit, the implications are stark.

What is equally evident, as shown below, is the laissez-faire attitude of the FTSE as opposed to the caution and reality being priced in by the currency markets. In Lehman’s case, the stock market was similarly complacent while the ten year Treasury yield dropped by nearly 2.00% from June 2007 to March 2008 (from a yield of 5.25% to 3.25%) on growing economic concerns and a flight-to-quality bid.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/11/3-combo.png[/image]

Data Courtesy: Bloomberg

A Familiar Problem

As discussed above, the Bank of England may find itself in a predicament where it is constrained from undertaking extreme measures due to inflation concerns or even being forced to tighten monetary policy despite an economic slowdown. Those actions would normally serve to support the pound. Further, if the prospect of a hard Brexit continues to take shape, capital flight out of the UK may overwhelm traditional factors. In efforts to prevent the disorderly movement of capital out of the country, the BoE may be required to hike interest rates substantially. Unlike the resistance of equity markets to bad news, the currency markets are more inclined, due to their size and much higher trading volume, to fairly reflect the dynamics of the economy and the central bank in a reasonable time frame.

Our perspective is not to presume a worst case scenario but to at least entertain and strategize for the range of possibilities. Equity markets, both in the UK and throughout the world, transfixed by the shell game of global central bankers’ interventionism, are clearly not properly assessing the probabilities and implications of a hard Brexit.

All things considered, the pound has rallied back to the high end of its post-Brexit range which seems to suggest the best outcome has been incorporated. If forced to act against inflation, the Bank of England will be hiking rates against a stagnant economy and a poor economic outlook. This may provide support for the pound in the short term but it will certainly hurt an already anemic economy in the midst of Brexit uncertainty.

Summary

Timing markets is a fool’s errand. Technical and fundamental analysis allows for an assessment of the asymmetry of risks and potential rewards, but the degree of central bank interventionism is not quantifiable. With that premise in mind, we can evaluate different asset classes and their adherence to fundamentals while allowing a margin of error for the possibility of monetary intervention. After all, if central banks print money to inflate asset prices to create a wealth effect, some other asset should reveal the negative effects of conjuring currency in a fiat regime – namely the currency itself. In the short term, it may appear as though rising asset prices create new wealth, but over time, the reality is that the currency adjustments off-set some or all of the asset inflation.

Investors should take the time, while it is available, to consider the gravity of the disruptions a hard Brexit portends and look beyond high flying UK stocks to the more telling movement of the British pound. Like with Lehman and the global financial system in 2008, stocks may initially be blind to the obvious. Although decidedly not under the threats present during World War II, the British Government and the EU lack the leadership of that day and will likely need more than central banker propaganda to weather the economic storm ahead.

Keep calm and carry on, indeed.