Submitted by Lance Roberts via RealInvestmentAdvice.com,

Earnings Worse Than You Think

Just like the hit series “House Of Cards,” Wall Street earnings season has become rife with manipulation, deceit and obfuscation that could rival the dark corners of Washington, D.C.

What is most fascinating is that so many individuals invest hard earned capital based on these manipulated numbers. The failure to understand the “quality” of earnings, rather than the “quantity,” has always led to disappointing outcomes at some point in the future.

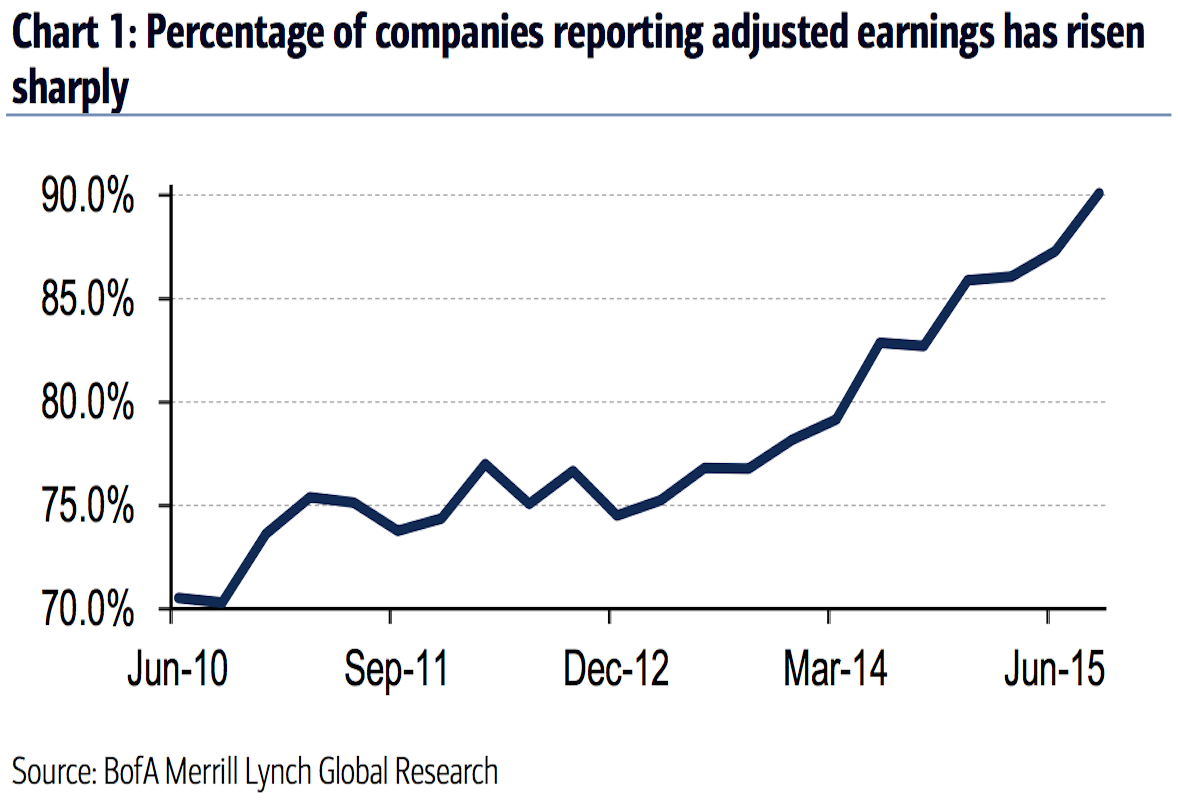

According to analysts at Bank of America Merrill Lynch, the percentage of companies reporting adjusted earnings has increased sharply over the past 18 months or so. Today, almost 90% of companies now report earnings on an adjusted basis.

Back in the 80’s and early 90’s companies used to report GAAP earnings in their quarterly releases. If an investor dug through the report they would find “adjusted” and “proforma” earnings buried in the back. Today, it is GAAP earnings which are buried in the back hoping investors will miss the ugly truth.

These “adjusted or Pro-forma earnings” exclude items that a company deems “special, one-time or extraordinary.” The problem is that these “special, one-time” items appear “every” quarter leaving investors with a muddier picture of what companies are really making.

As BofAML states:

“We are increasingly concerned with the number of companies (non-commodity) reporting earnings on an adjusted basis versus those that are stressing GAAP accounting, and find the divergence a consequence of less earnings power.

Consider that when US GDP growth was averaging 3% (the 5 quarters September 2013 through September 2014) on average 80% of US HY companies reported earnings on an adjusted basis. Since September 2014, however, with US GDP averaging just 1.9%, over 87% of companies have reported on an adjusted basis. Perhaps even more telling, between the end of 2010 and 2013, the percentage of companies reporting adjusted EBITDA was relatively constant and since 2013, the number has been on a steady rise.

We are increasingly concerned with this trend, as on an unadjusted basis non-commodity earnings growth has been negative 2 of the last 4 quarters, representing the worst 4 quarter average earnings growth in a non-recessionary period since late 2000.”

This accounting manipulation to win the “beat the earnings” game each quarter is important to corporate executives whose major source of wealth is stock-based compensation. As confirmed in a WSJ article:

“If you believe a recent academic study, one out of five [20%] U.S. finance chiefs have been scrambling to fiddle with their companies’ earnings.

Not Enron-style, fraudulent fiddles, mind you. More like clever—and legal—exploitations of accounting standards that ‘manage earnings to misrepresent [the company’s] economic performance,’ according to the study’s authors, Ilia Dichev and Shiva Rajgopal of Emory University and John Graham of Duke University. Lightly searing the books rather than cooking them, if you like.”

This should not come as a major surprise as it is a rather “open secret.” Companies manipulate bottom line earnings by utilizing “cookie-jar” reserves, heavy use of accruals, and other accounting instruments to flatter earnings.

“The tricks are well-known: A difficult quarter can be made easier by releasing reserves set aside for a rainy day or recognizing revenues before sales are made, while a good quarter is often the time to hide a big ‘restructuring charge’ that would otherwise stand out like a sore thumb.

What is more surprising though is CFOs’ belief that these practices leave a significant mark on companies’ reported profits and losses. When asked about the magnitude of the earnings misrepresentation, the study’s respondents said it was around 10% of earnings per share.“

Why is this important? Because, while manipulating earnings may work in the short-term, eventually, cost cutting, wage suppression, earnings manipulations, share-buybacks, etc. reach their effective limit. When that limit is reached, companies can no longer hide the weakness in their actual operating revenues. That point has likely been reached.

From the WSJ:

“There’s a big difference between companies’ advertised performance in 2015 and how they actually did.

How big? With most calendar-year results now in, FactSet estimates companies in the S&P 500 earned 0.4% more per share in 2015 than the year before. That marks the weakest growth since 2009. But this is based on so-called pro forma figures, results provided by companies that exclude certain items such as restructuring charges or stock-based compensation.

Look to results reported under generally accepted accounting principles (GAAP) and S&P earnings per share fell by 12.7%, according to S&P Dow Jones Indices. That is the sharpest decline since the financial crisis year of 2008. Plus, the reported earnings were 25% lower than the pro forma figures—the widest difference since 2008 when companies took a record amount of charges.

?The implication: Even after a brutal start to 2016, stocks may still be more expensive than they seem. Even worse, investors may be paying for earnings and growth that aren’t anywhere near what they think. The result could be that share prices have even further to fall before they entice true value investors.

The difference shows up starkly when looking at price/earnings ratios. On a pro forma basis, the S&P trades at less than 17 times 2015 earnings. But that shoots up to over 21 times under GAAP.“

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/SP-500-Earnings-WorseThanRealized-022416.png[/image]

History is pretty clear. As long as earnings are deteriorating, you don’t want to be invested in stocks.

Fantasy Vs. Reality

What is most interesting, is that despite the ongoing earnings recession, Wall Street firms continue to predict an onward and upward push of profitability into the foreseeable future. As shown in the estimates below from Goldman Sachs, there is NO consideration for the impact of economic recession over the next several years.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/GS-Profits-SP500-Targets-022316.jpg[/image]

Of course, this was the same prediction made in 1999 and in 2006 until the eventual and inevitable “reversion to the mean” occurred.

Eric Parnell recently penned an excellent piece in this regard entitled “Fantasy vs. Reality:”

“The perpetual optimism of the corporate earnings forecast is remarkable. And while its well understood that things almost never turn out as good as we might anticipate, it is notable how widely divergent these earnings forecasts are from the actual outcomes that ultimately come to pass. Beware the analysis pinning its conclusions on the forward price-to-earnings ratio on the S&P 500 Index or any of its constituents for that matter, for it may lead to conclusions that are ultimately built on sand.

Clearly, relying on corporate earnings forecasts for the basis of investment decision making should be done at an investors own risk. Forecasts start out as wildly optimistic, with greater hopes the longer the time horizon. Which leads to a final point worth mentioning. Standard & Poor’s recently released a first look at the earnings forecasts for 2017. And if past experience is any guide, it may be indicating trouble on the horizon for the coming year. For instead of the robust +20% earnings forecasts throughout 2017, we instead see a notable fade as the year progresses. Perhaps these forecasts will improve with the passage of time.

But if forecasters are this unenthusiastic about a point that is so far away in the future, what will the reality look like once we finally arrive?”

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/02/Corporate-Profits-Growth-2017-022416.jpg[/image]

Unfortunately, considering that historically analysts future forecasts are 33% higher on average than reality turns out to be, the case for a deeper “bear market” is gaining traction.

EBITDA Is BullS***

I have written in the past about the fallacy of using EBITDA (Earnings Before Interest Taxes Depreciation and Amortization) due to the ability to fudge/manipulate the number. To wit:

[image]https://realinvestmentadvice.com/wp-content/uploads/2015/06/images_1dailyxchange_misc_Cooking-The-Books.PNG[/image]

“As shown in the table, it is not surprising to see that 93% of the respondents pointed to “influence on stock price” and “outside pressure” as the reason for manipulating earnings figures. For fundamental investors this manipulation of earnings skews valuation analysis particularly with respect to P/E’s, EV/EBITDA, PEG, etc.”

Ramy Elitzur, via The Account Art Of War, recently expounded on the problems of using EBITDA.

“Being a CPA and having an MBA, in my arrogance I thought that I am well beyond such materials. I stood corrected, whatever I thought I knew about accounting was turned on its head. One of the things that I thought that I knew well was the importance of income-based metrics such as EBITDA and that cash flow information is not as important. It turned out that common garden variety metrics, such as EBITDA, could be hazardous to your health.”

The article is worth reading and chocked full of good information, however, here are the four-crucial points:

- EBITDA is not a good surrogate for cash flow analysis because it assumes that all revenues are collected immediately and all expenses are paid immediately, leading, as I illustrated above, to a false sense of liquidity.

- Superficial common garden-variety accounting ratios will fail to detect signs of liquidity problems.

- Direct cash flow statements provide a much deeper insight than the indirect cash flow statements as to what happened in operating cash flows. Note that the vast majority (well over 90%) of public companies use the indirect format.

- EBITDA just like net income is very sensitive to accounting manipulations.

The last point is the most critical. As discussed above, the tricks to manipulate earnings are well-known which inflates the results to a significant degree making an investment appear “cheaper” than it actually is.

As Charlie Munger once said:

“I think that every time you see the word EBITDA, you should substitute the word ‘bullshit’ earnings.”

Just some things to think about.