Submitted by Lance Roberts via RealInvestmentAdvice.com,

Tax Cut Rainbows

Can we slow down for just a minute and let a little bit of logic prevail. The exuberance by Wall Street over the election of Trump, which is ironic because these were the same guys saying his election would crash the market, has gotten a little heated. In particular, is the repeated impact of tax cuts on earnings over the next year as recently reiterated by Bob Pisani:

“Even before the election, analysts were anticipating a roughly 9 percent increase in earnings for the S&P 500, from roughly $118 in 2016 to $131 in 2017. But I noted back on Dec. 1 that Thomson Reuters estimated that every 1 percentage point reduction in the corporate tax rate could “hypothetically” add $1.31 to 2017 earnings. So with a full 20 percentage point reduction in the tax rate (from 35 percent to 15 percent), that’s $1.31 x 20 = $26.20.

That implies an increase in earnings of close to 20 percent, or $157. Of course, this is a hypothetical and because most corporations do not pay the top rate, we won’t get this kind of boost. No matter: Even a modest boost to, say, $140, would bring the S&P to 2400 at the current 17 multiple, nearly 7 percent above where it is now.”

There is a raft of issues with this analysis which investors have taken to heart since Reuters first trotted this idea a little over a month ago.

First, as noted by the Government Accountability Office, the average tax rate paid by U.S. corporations is not 35% but closer to 12.5%.

“Large, profitable U.S. corporations paid an average effective federal tax rate of 12.6% in 2010, the Government Accountability Office said Monday.

The federal corporate tax rate stands at 35%, and jumps to 39.2% when state rates are taken into account. But thanks to things like tax credits, exemptions and offshore tax havens, the actual tax burden of American companies is much lower.

Even when foreign, state and local taxes were taken into account, the companies paid only 16.9% of their worldwide income in taxes in 2010.”

Therefore, the reduction in the legislative tax rates to 15-20% is likely to be far less impactful to earnings growth than what is currently estimated by Reuters.

Secondly, the expectations of a $1.31 boost to earnings for each percentage point of reduction in tax rates is also a bit “squishy.”

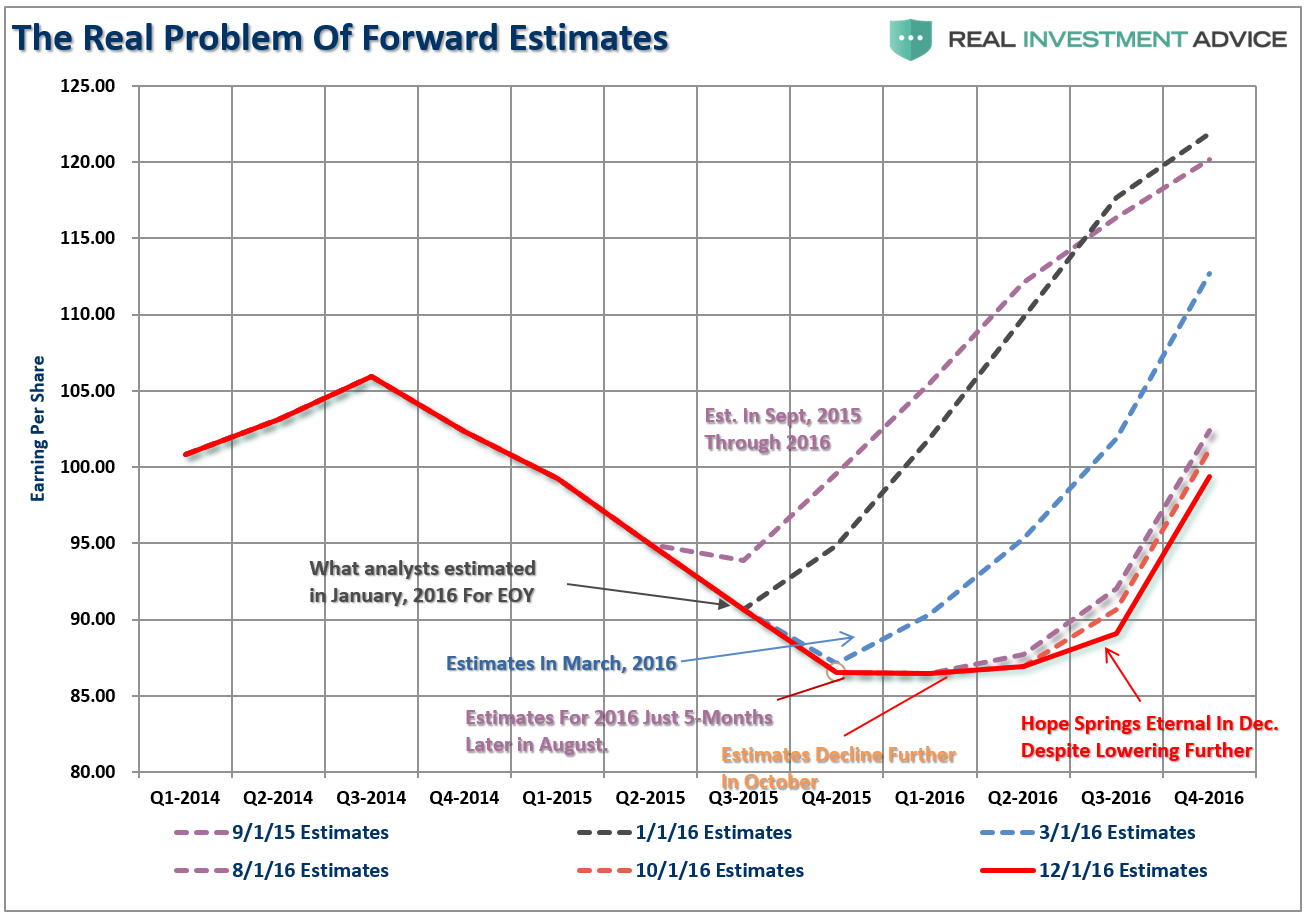

The premise is based on the currently expected earnings in 2017 of $131.00 for the entirety of the S&P 500. The $1.31 increase is simply 1% of $131.00 in total operating earnings. However, given the fact that earnings are consistently overestimated historically by roughly 33%, as shown in the chart below, and are grossly affected by “one-time” repeating write-offs, accounting gimmickry, and a variety of other issues, the assumption of effective impact of a tax rate change of 1% of face value of earnings is awfully presumptive.

Given the strong rise in the U.S. Dollar as of late, along with the incremental increase in borrowing costs from higher Treasury rates, it is quite likely the drag on earnings from the reduction in exports will offset much of the impact of any tax rate changes that come about. With the Federal Reserve once again chasing an “inflation monster,” much as they did in 1999, the tightening of monetary policy will also further offset much of the benefit of tax rate changes.

As we saw with the Bush tax cuts in 2001, and the repatriation holiday in 2004, the impacts from policy changes are more “psychological” short-term boosts which are quickly absorbed by economic realities.

Consumer Spending Puppies

Keeping the tax cut meme going for a minute, it is hoped tax reform for individuals, along with the recent surge in optimism, will lead to a sharp increase in consumer spending. Maybe it will.

It is also important to remember that “Revenue” is a function of consumption. Therefore, while lowering taxes is certainly beneficial to the bottom line of corporations, it is ultimately what happens at the “top line” where decisions are made to increase employment, increase production and make investments.

In other words, it remains a spending and debt problem.

“Given the lack of income growth and rising costs of living, it is unlikely that Americans are actually saving more. The reality is consumers are likely saving less and may even be pushing a negative savings rate.

I know suggesting such a thing is ridiculous. However, the BEA calculates the saving rate as the difference between incomes and outlays as measured by their own assumptions for interest rates on debt, inflationary pressures on a presumed basket of goods and services and taxes. What it does not measure is what individuals are actually putting into a bank saving or investment account. In other words, the savings rate is an estimate of what is ‘likely’ to be saved each month.

However, as we can surmise, the reality for the majority of American’s is quite the opposite as the daily costs of maintaining the current standard of living absorbs any excess cash flow. This is why I repeatedly wrote early on that falling oil prices would not boost consumption and it didn’t.”

As shown in the chart below, consumer credit has surged in recent months.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/PCE-Struggle-To-Maintain-Standard-Of-Living-010417.png[/image]

Here is another problem. While economists, media, and analysts wish to blame those “stingy consumers” for not buying more stuff, the reality is the majority of American consumers have likely reached the limits of their ability to consume. This decline in economic growth over the past 30 years has kept the average American struggling to maintain their standard of living.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/Debt-Wages-010417.png[/image]

As shown above, consumer credit as a percentage of total personal consumption expenditures has risen from an average of 20% prior to 1980 to almost 30% today. As wage growth continues to stagnate, the dependency on credit to foster further consumption will continue to rise. Unfortunately, as I discussed previously, this is not a good thing as it relates to economic growth in the future.

“The massive indulgence in debt, what the Austrians refer to as a “credit induced boom,” has likely reached its inevitable conclusion. The unsustainable credit-sourced boom, which led to artificially stimulated borrowing, has continued to seek out ever diminishing investment opportunities.”

While lower tax rates will certainly boost bottom line earnings, particularly as share buybacks increase from increased retention, as noted there are huge differences between the economic and debt related backdrops between today and the early 80’s.

The true burden on taxpayers is government spending, because the debt requires future interest payments out of future taxes. As debt levels, and subsequently deficits, increase, economic growth is burdened by the diversion of revenue from productive investments into debt service.

This is the same problem that many households in America face today. Many families are struggling to meet the service requirements of the debt they have accumulated over the last couple of decades with the income that is available to them. They can only increase that income marginally by taking on second jobs. However, the biggest ability to service the debt at home is to reduce spending in other areas.

While lowering corporate tax rates will certainly help businesses potentially increase their bottom line earnings, there is a high probability that it will not “trickle down” to middle-class America.

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/12/wealth-distribution10-15.jpg[/image]

Hopefully Hopeful

While I am certainly hopeful for meaningful changes in tax reform, deregulation and a move back towards a middle-right political agenda, from an investment standpoint there are many economic challenges that are not policy driven.

- Demographics

- Structural employment shifts

- Technological innovations

- Globalization

- Financialization

- Global debt

“In the latest report from the Institute for International Finance released on Wednesday, total debt as of Q3 2016 once again rose sharply, increasing by $11 trillion in the first 9 months of the year, hitting a new all-time high of $217 trillion. As a result, late in 2016, global debt levels are now roughly 325% of the world’s gross domestic product.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/Global-debt.jpg[/image]

All of these challenges, and particularly the debt, will continue to weigh on economic growth, wages and standards of living into the foreseeable future. As a result, incremental tax and policy changes will have a more muted effect on the economy as well.

This was also noted by the Fed in their most recent release of the December meeting minutes:

“However, the staff noted that the impact of easier fiscal policy was ‘substantially counterbalanced by the restraint from the higher assumed paths for longer-term interest rates and the foreign exchange value of the dollar.’ The offset from tighter financial conditions may also explain why median forecasts for GDP growth were little changed in participants’ Summary of Economic Projections (SEP).”

It is not just tighter monetary policy weighing on fiscal policy changes but the economic challenges as well. As my partner Michael Lebowitz recently pointed out – “this ain’t the 1980’s.”

“Many investors are suddenly comparing Trump’s economic policy proposals to those of Ronald Reagan. For those that deem that bullish, we remind you that the economic environment and potential growth of 1982 was vastly different than it is today.“

[image]https://realinvestmentadvice.com/wp-content/uploads/2016/11/1982-today.png[/image]

This also isn’t 2009 where economic activity and consumption is extremely depressed which gives tax cuts, incentives and regulatory reforms have a much bigger impact on economic and earnings growth.

As Michael concludes:

“As investors, we must understand the popular narrative and respect it as it is a formidable short-term force driving the market. That said, we also must understand whether there is logic and truth behind the narrative. In the late 1990’s, investors bought into the new economy narrative. By 2002, the market reminded them that the narrative was born of greed, not reality. Similarly, in the early to mid-2000’s real estate investors were lead to believe that real-estate prices never decline.

The bottom line is that one should respect the narrative and its ability to propel the market higher.“

Will “Trumponomics” change the course of the U.S. economy? I certainly hope so as any improvement that filters down to the bottom 80% of the country will be beneficial.

However, as investors, we must understand the difference between a “narrative-driven” advance and one driven by strengthening fundamentals. The first is short-term and leads to bad outcomes. The other isn’t, and doesn’t.

Just some things I am thinking about.