Published

1 hour ago

on

September 26, 2025

| 1,461 views

-->

By

Jenna Ross

Article & Editing

- Ryan Bellefontaine

Graphics & Design

- Zack Aboulazm

The following content is sponsored by Citizens Bank

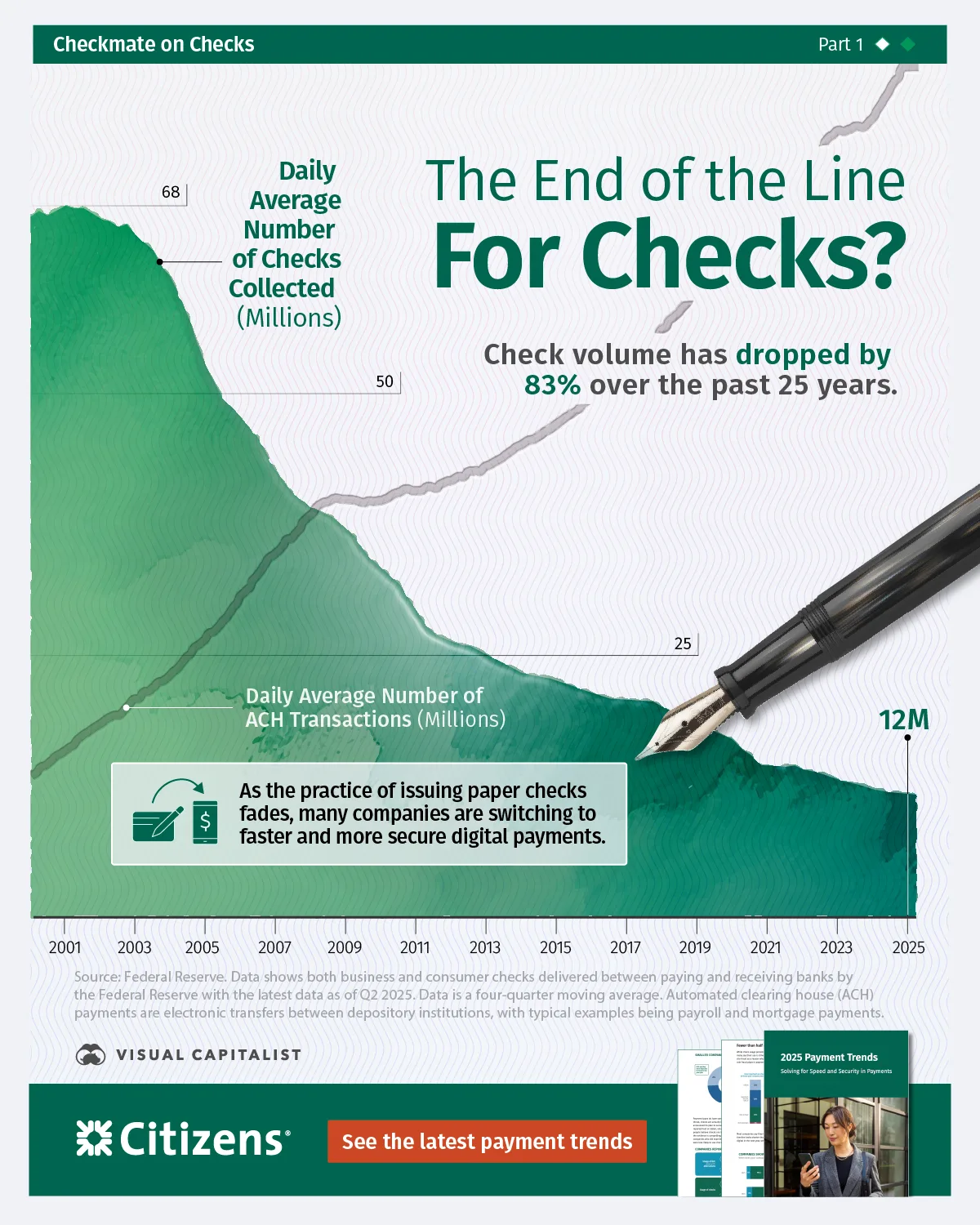

Charted: The End of the Line For Checks?

Key Takeaways

- Checks are in structural decline, while adoption of the Automated Clearing House (ACH) continues to accelerate.

- The acceleration of ACH continues as digital payment methods are faster and more secure.

Checks once anchored B2B payments. However, finance teams now prioritize speed, control, and data—and paper simply can’t keep pace.

This graphic, created in partnership with Citizens Bank, shows the long-run decline of checks and the rise of Automated Clearing House (ACH) volumes, using data from the Federal Reserve.

Checks in Decline

Over the past quarter-century, check usage trends have decreased, while daily ACH transactions have accelerated. As the gap widens, it’s clear companies are shifting to digital payments for the long term.

Here is a table that shows the decline in check volume from both business and consumer checks delivered between paying and receiving banks. The table also shows the growth in daily ACH transactions from Q1 2000 to Q2 2025.

| Year and Quarter | Average Daily Number of Checks (Millions) | Average Daily Number of Automated Clearing House (ACH) Transactions (Millions) |

|---|---|---|

| 2000:Q1 | 68 | 14 |

| 2000:Q2 | 68 | 14 |

| 2000:Q3 | 68 | 15 |

| 2000:Q4 | 68 | 15 |

| 2001:Q1 | 68 | 16 |

| 2001:Q2 | 68 | 16 |

| 2001:Q3 | 68 | 17 |

| 2001:Q4 | 67 | 18 |

| 2002:Q1 | 67 | 18 |

| 2002:Q2 | 67 | 19 |

| 2002:Q3 | 66 | 19 |

| 2002:Q4 | 66 | 20 |

| 2003:Q1 | 65 | 21 |

| 2003:Q2 | 65 | 21 |

| 2003:Q3 | 64 | 22 |

| 2003:Q4 | 62 | 22 |

| 2004:Q1 | 61 | 23 |

| 2004:Q2 | 59 | 24 |

| 2004:Q3 | 57 | 25 |

| 2004:Q4 | 55 | 26 |

| 2005:Q1 | 53 | 26 |

| 2005:Q2 | 51 | 27 |

| 2005:Q3 | 49 | 28 |

| 2005:Q4 | 49 | 29 |

| 2006:Q1 | 48 | 30 |

| 2006:Q2 | 47 | 32 |

| 2006:Q3 | 46 | 33 |

| 2006:Q4 | 44 | 34 |

| 2007:Q1 | 43 | 35 |

| 2007:Q2 | 42 | 35 |

| 2007:Q3 | 40 | 36 |

| 2007:Q4 | 40 | 37 |

| 2008:Q1 | 39 | 38 |

| 2008:Q2 | 39 | 39 |

| 2008:Q3 | 38 | 40 |

| 2008:Q4 | 38 | 40 |

| 2009:Q1 | 37 | 40 |

| 2009:Q2 | 36 | 40 |

| 2009:Q3 | 35 | 39 |

| 2009:Q4 | 34 | 40 |

| 2010:Q1 | 33 | 40 |

| 2010:Q2 | 33 | 40 |

| 2010:Q3 | 32 | 41 |

| 2010:Q4 | 31 | 41 |

| 2011:Q1 | 29 | 41 |

| 2011:Q2 | 28 | 41 |

| 2011:Q3 | 27 | 41 |

| 2011:Q4 | 27 | 41 |

| 2012:Q1 | 26 | 42 |

| 2012:Q2 | 26 | 42 |

| 2012:Q3 | 26 | 42 |

| 2012:Q4 | 26 | 43 |

| 2013:Q1 | 25 | 43 |

| 2013:Q2 | 25 | 43 |

| 2013:Q3 | 24 | 44 |

| 2013:Q4 | 24 | 44 |

| 2014:Q1 | 23 | 45 |

| 2014:Q2 | 23 | 45 |

| 2014:Q3 | 23 | 46 |

| 2014:Q4 | 23 | 46 |

| 2015:Q1 | 23 | 47 |

| 2015:Q2 | 22 | 48 |

| 2015:Q3 | 22 | 48 |

| 2015:Q4 | 22 | 49 |

| 2016:Q1 | 22 | 50 |

| 2016:Q2 | 21 | 50 |

| 2016:Q3 | 21 | 51 |

| 2016:Q4 | 21 | 52 |

| 2017:Q1 | 21 | 53 |

| 2017:Q2 | 21 | 53 |

| 2017:Q3 | 21 | 54 |

| 2017:Q4 | 21 | 55 |

| 2018:Q1 | 20 | 56 |

| 2018:Q2 | 20 | 57 |

| 2018:Q3 | 19 | 58 |

| 2018:Q4 | 19 | 59 |

| 2019:Q1 | 18 | 59 |

| 2019:Q2 | 18 | 60 |

| 2019:Q3 | 18 | 61 |

| 2019:Q4 | 17 | 62 |

| 2020:Q1 | 17 | 63 |

| 2020:Q2 | 16 | 63 |

| 2020:Q3 | 16 | 64 |

| 2020:Q4 | 15 | 65 |

| 2021:Q12 | 14 | 66 |

| 2021:Q2 | 15 | 68 |

| 2021:Q3 | 14 | 69 |

| 2021:Q4 | 15 | 71 |

| 2022:Q1 | 14 | 71 |

| 2022:Q2 | 14 | 72 |

| 2022:Q3 | 14 | 73 |

| 2022:Q4 | 13 | 74 |

| 2023:Q1 | 13 | 75 |

| 2023:Q2 | 13 | 75 |

| 2023:Q3 | 13 | 75 |

| 2023:Q4 | 13 | 75 |

| 2024:Q1 | 12 | 76 |

| 2024:Q2 | 12 | 77 |

| 2024:Q3 | 12 | 79 |

| 2024:Q4 | 12 | 80 |

| 2025:Q1 | 12 | 82 |

| 2025:Q2 | 12 | 82 |

Data shows both business and consumer checks delivered between paying and receiving banks by the Federal Reserve with the latest data as of Q2 2025. Data is a four-quarter moving average. Automated clearing house (ACH) payments are electronic transfers between depository institutions, with typical examples being payroll and mortgage payments.

Check volume is down roughly 83% over the past 25 years. Given this trajectory, many finance leaders are moving away from checks in favor of digital payments.

Meanwhile, daily ACH transactions have increased by 497% during the same period, demonstrating a sharper incline than the decline in check usage.

While every organization is different, the trend suggests that shifting recurring flows to ACH can deliver near-term benefits.

The Benefits of Digital Payment Methods

Digital payments—especially ACH—tend to move money faster and include clearer details that make invoice matching easier. In Citizens’ 2025 Payment Trends Survey, treasury leaders put speed and security near the top of their priorities.

Checks still play a role, but usage is shrinking: 47% of midsize businesses say they use checks today, down from 59% in 2024. Among firms that still use cash or checks, 33% plan to go all-digital within a year and another 42% within two to three years.

Given the direction of technology and artificial intelligence, many teams are gradually shifting routine payments toward digital options at a pace that fits their operations.

![]()

See the latest payment trends from Citizens Bank

Related Topics: #Finance #business #banks #Citizens Bank #checks #ach #automated clearing house

Click for Comments

var disqus_shortname = "visualcapitalist.disqus.com";

var disqus_title = "Charted: The End of the Line For Checks?";

var disqus_url = "https://www.visualcapitalist.com/sp/cb03-charted-the-end-of-the-line-for-checks/";

var disqus_identifier = "visualcapitalist.disqus.com-182561";

More from Citizens Bank

-

Technology7 months ago

AI Stocks: The Capital-Raising Surge

AI stocks captured investors’ interest in 2024, drawing a third of all VC funding. So, which companies are securing the biggest investments?

-

Financing9 months ago

Public vs. Privately-Held Companies: The Shifting Landscape

Over the last 25 years, the number of public companies has dropped while the number of privately-held companies has risen.

Subscribe

Please enable JavaScript in your browser to complete this form.Join 375,000+ email subscribers: *Sign Up