Submitted by Jesse Felder via TheFelderReport.com,

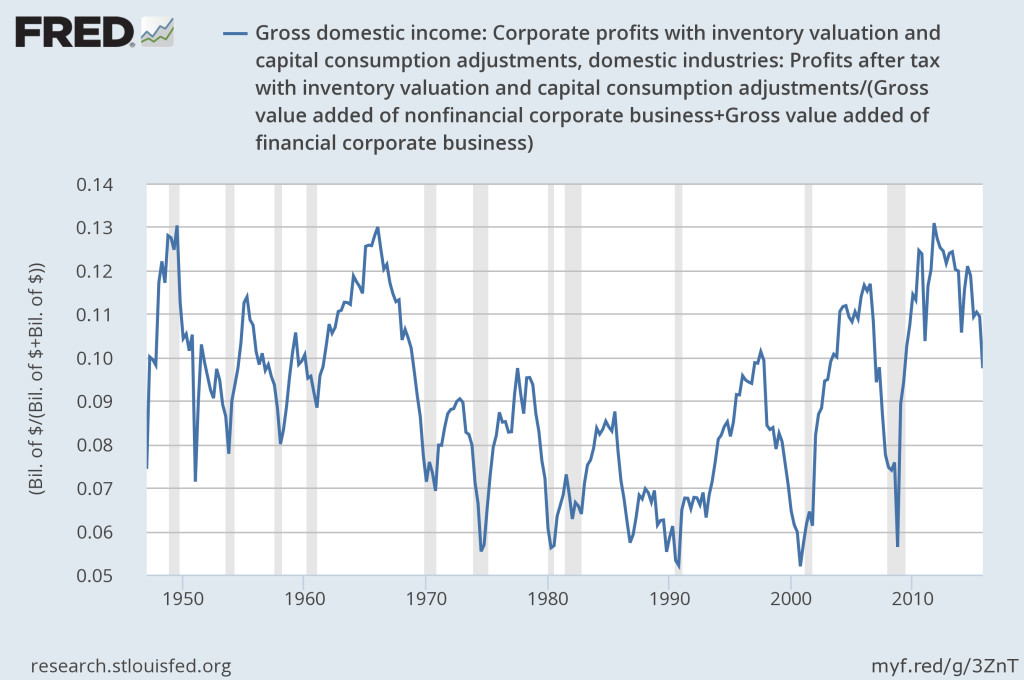

Over the past few years I’ve written a fair amount about the record-high levels of corporate profit margins. I’ve been focused on this topic because corporate earnings are one of the most popular ways to value equities thus the sustainability of record-high profit margins should be an issue of great concern to investors. If profit margins revert to historical averages, earnings-based valuation measures investors are using to justify investment in equities today could quickly go against them making stocks appear much more expensive than they do currently. And this process may now be underway.

To the point of mean reversion in profit margins, in the past I have referenced the words of a pair of investment legends. Jeremy Grantham has called profit margins, “the most mean-reverting series in finance.” And back in 1999, Warren Buffett explained why:

In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems—and in my view a major reslicing of the pie just isn’t going to happen.

Both of these two gentlemen clearly believe, and very strongly, that corporate profit margins have an equilibrium. They can rise above or fall below that equilibrium but the very nature of capitalism, along with its social contract, will force an inevitable reversion to the mean.

I believe there are three major factors behind the recent bubble in corporate profit margins.

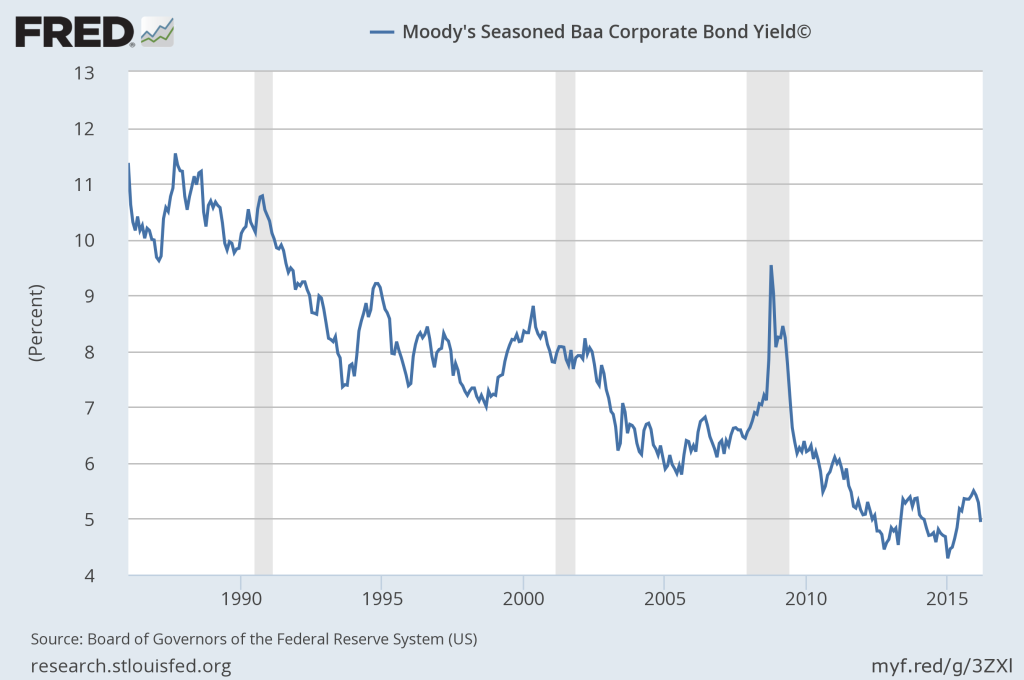

First, and most obvious, is the simple trend in interest rates over the past 35 years or so. As rates have fallen to lows not seen in many generations, debt has become much less costly, especially when you also consider that corporate spreads on top of these ultra-low rates have also fallen to ultra-low levels.

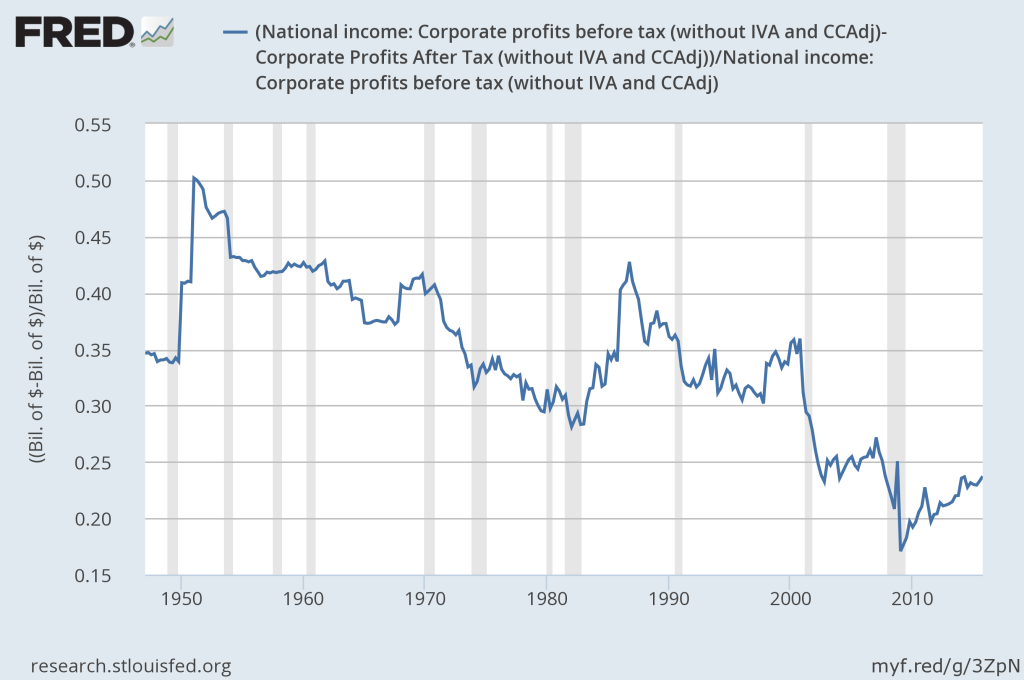

Second, corporate taxes as a percent of income have been falling for a long time, as well. Recently, this may be due in large part to the growth of tax avoidance strategies, mainly those involving relocating corporate headquarters to tax havens.

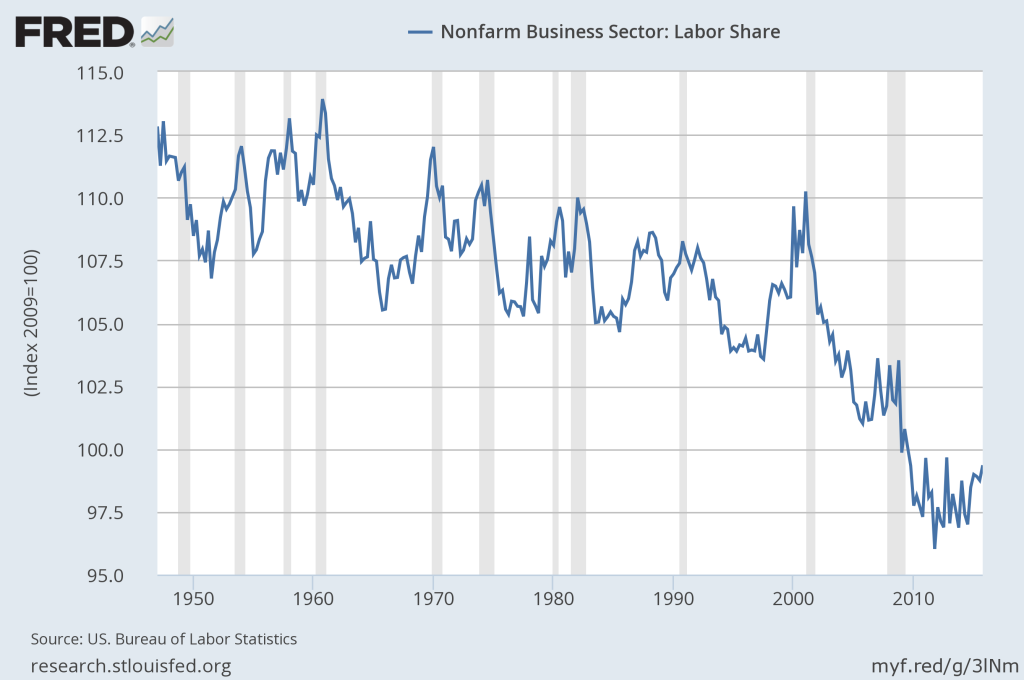

Third, labor costs have also been falling for quite some time. Much of this may be due to the trend toward automation and, perhaps far more so, the offshoring of labor over the past several decades. This falling corporate cost is very apparent in the labor share of income numbers that many have discussed recently, including Paul Tudor Jones.

These three secular trends have provided a tailwind for profit margins for a long time now. However, they may be reaching, or have already reached, their full potential and begun reverting. In terms of interest rates, the Fed Funds rate has essentially been stuck at zero for seven years now. Corporate spreads hit rock bottom almost two years ago and have been reversing course ever since. Furthermore, after a long period of deregulation in the banking industry that saw lending standards loosen considerably, it appears that regulation is making a sustained comeback and the effect will likely be just the opposite.

Politically, corporations are finding it increasingly difficult to defend their use of tax avoidance schemes. Politicians have been squawking about this for a long time but it now appears as if they are ready to actually do something about it. More and more companies are reporting growing political risk in this regard as new legislation is being introduced in a variety of countries to combat it.

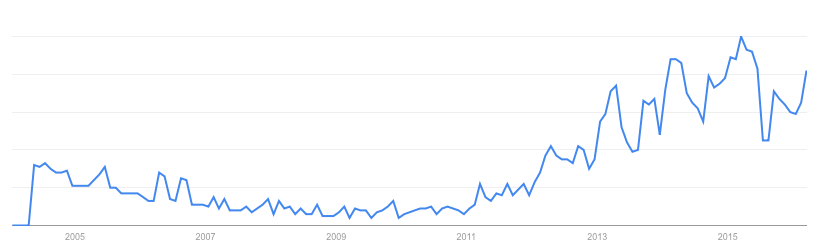

Finally, the trend toward offshoring looks to be in the process of reversing as overseas labor costs rise and companies focus more and more on the potential quality and branding benefits of, “reshoring.” Google trends shows a surge in the popularity of this search term in recent years.

So I agree with Grantham and Buffett that profit margins are very likely to continue to revert to their historical mean, driven by the natural forces of capitalism, and its social contract. And this will most likely be seen in either the rising cost of debt, taxes or labor, or perhaps all three.

In the short-term, history suggests the current profits recession very likely will lead to an economic recession accompanied by a bear market. In fact, profit margin peaks regularly lead major stock market peaks and profit margins peaked this cycle about four years ago already. In addition, the recent fall in earnings and profit margins is already beginning to damage those earnings-based valuation measures. The S&P 500 now trades at its highest price-to-earnings ratio since the bull market began even as the index remains well off its recent price highs. And profit margins still could have a long way to fall before even reaching their average level since 1950.

Longer-term, if these new secular trends working against profit margins are to remain in place, earnings growth will be much harder to come by for corporate America than it has been over the past few decades. And there are plenty of signs it is already becoming very difficult for them. Corporate cash flow has essentially been flat for the past five years. At the same time, more and more companies recently have resorted to financial engineering via buybacks, non-GAAP reporting and even outright fraud. My guess is this is all in an attempt to make up for broadly slowing organic profit growth due the these secular tailwinds shifting to headwinds.

Should these shifts actually turn out to be longer-term secular trends, they pose a great risk to equities in both the short-term and the long-term. Falling profit margins and rising valuations (as earnings fall) make for a pretty bearish one-two punch for the stock market. I can’t imagine investors being very eager to pay higher valuations for companies growing more slowly. That equation usually works in reverse. And there’s no reason I can see to expect these challenges to corporate profit margins to let up any time soon.