Submitted by Lance Roberts via RealInvestmentAdvice.com,

It’s the Fed’s fault.

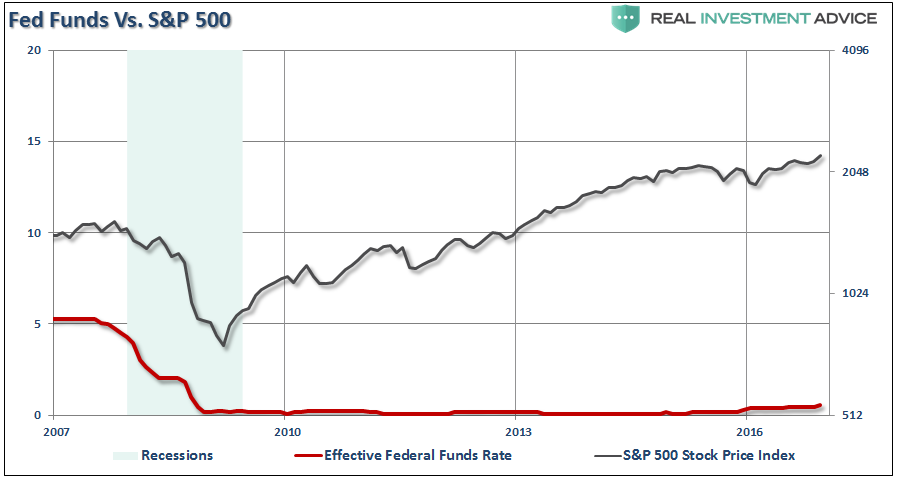

Over the past several years, the Federal Reserve has forced interest rates lower in an all-out assault on “cash.”

The theory was simple. Make returns on “cash” so low it is forced out of savings account and into risk assets.

It worked.

But here is the problem.

While the ongoing interventions by the Federal Reserve have certainly boosted asset prices higher, the only real accomplishment has been a widening of the wealth gap between the top 10% of individuals that have dollars invested in the financial markets and everyone else. This was shown by the Fed’s most recent consumer survey.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/Fed-Survey-Median-ValueofAssets-Quintile-052916.png[/image]

With the average American still living well beyond their means, the reality is that economic growth will remain mired at lower levels as savings continue to be diverted from productive investment into debt service. This skew in wealth, between the top 10% and bottom 90%, has distorted much of the economic data which suggests savings rates and incomes are rising across the broad spectrum of the economy. The reality, as shown by repeated studies and surveys, is an inability for many individuals to meet even small emergencies, must less being anywhere close to having sufficient assets to support a healthy retirement. To wit:

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/1-3-NoSavings-011517.jpg[/image]

Take a look at that graphic carefully.

- 33% of Americans have $0 saved for retirement.

- 56% only have $0-$10,000

- 66% have less than one-year of median income saved.

- 74% have less than $100,000 saved for retirement.

With 3/4th’s of America dependent upon an already overburdened social security system in retirement, the “consumption function,” on which roughly 70% of the economy is dependent, is being grossly overestimated.

The Risk Of Holding Cash

As I noted in this past weekend’s missive, the level of cash being held by individual investors currently is near record lows.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/AAII-CashAllocation-011517.png[/image]

Of course, Wall Street, analysts and the media have been all complicit in the “war on cash.”

The argument against holding cash is simply this:

“Since there is “no yield on cash,” you MUST invest in the stock market otherwise you are losing money due to inflation and opportunity costs.”

This is a true statement ONLY IF you hold cash for an EXTREMELY long period. However, holding cash as a “hedge” against market volatility during periods of elevated uncertainty is a different matter entirely.

It is relatively unimportant the markets are making new highs. The reality is that new highs only represent about 5% of the market’s action while the other 95% of the advance was making up previous losses. “Getting back to even” is not a long-term investing strategy.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Time-To-Recovery-011517.png[/image]

In a market environment that is extremely overvalued, the projection of long-term forward returns is exceedingly low. I have discussed this previously, but this cannot be overstated enough. This, of course, does not mean that markets just trade sideways, but in rather large swings between exhilarating rises and spirit-crushing declines. This is an extremely important concept in understanding the “real value of cash.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-PE-FutureReturns-011317-1.png[/image]

The chart below shows the inflation-adjusted return of $100 invested in the S&P 500 (capital appreciation only using data provided by Dr. Robert Shiller). The chart also shows Dr. Shiller’s CAPE ratio. However, I have capped the CAPE ratio at 23x earnings which has historically been the peak of secular bull markets in the past. Lastly, I calculated a simple cash/stock switching model which buys stocks at a CAPE ratio of 6x or less and moves back to cash at a ratio of 23x.

I have adjusted the value of holding cash for the annual inflation rate which is why during the sharp rise in inflation in the 1970’s there is a downward slope in the value of cash. However, while the value of cash is adjusted for purchasing power in terms of acquiring goods or services in the future, the impact of inflation on cash as an asset with respect to reinvestment may be different since asset prices are negatively impacted by spiking inflation. In such an event, cash gains purchasing power parity in the future if assets prices fall more than inflation rises.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/01/SP500-Real-ValueOfCash-011517.png[/image]

While no individual could effectively manage money this way, the importance of “cash” as an asset class is revealed. While cash did lose relative purchasing power, due to inflation, the benefits of having capital to invest at lower valuations produced substantial outperformance over waiting for previously destroyed investment capital to recover.

While we can debate over methodologies, allocations, etc., the point here is that “time frames” are crucial in the discussion of cash as an asset class. If an individual is “literally” burying cash in their backyard, then the discussion of the loss of purchasing power is appropriate.

However, if cash is a “tactical” holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.

Much of the mainstream media will quickly disagree with the concept of holding cash and tout long-term returns as the reason to just remain invested in both good times and bad. The problem is it is YOUR money at risk. Furthermore, most individuals lack the “time” necessary to truly capture 30 to 60-year return averages.

8-Reasons To Hold Cash

I’ve been managing money in some form coming up on 30-years. I learned a long time ago that while a “rising tide lifts all boats,” eventually the “tide recedes.” I made one simple adjustment to my portfolio management over the years which has served me well. When risks begin to outweigh the potential for reward, I raise cash.

The great thing about holding extra cash is that if I’m wrong, simply make the proper adjustments to increase the risk in my portfolios. However, if I am right, I protect investment capital from destruction and spend far less time “getting back to even” and spend more time working towards my long-term investment goals.

Here are my reasons having cash is important.

1) We are not investors, we are speculators. We are buying pieces of paper at one price with an endeavor to eventually sell them at a higher price. This is speculation at its purest form. Therefore, when probabilities outweigh the possibilities, I raise cash.

2) 80% of stocks move in the direction of the market. In other words, if the market is moving in a downtrend, it doesn’t matter how good the company is as most likely it will decline with the overall market.

3) The best traders understand the value of cash. From Jesse Livermore to Gerald Loeb they all believed one thing – “Buy low and Sell High.” If you “Sell High” then you have raised cash. According to Harvard Business Review, since 1886, the US economy has been in a recession or depression 61% of the time. I realize that the stock market does not equal the economy, but they are somewhat related.

4) Roughly 90% of what we’re taught about the stock market is flat out wrong: dollar-cost averaging, buy and hold, buy cheap stocks, always be in the market. The last point has certainly been proven wrong because we have seen two declines of over -50%…just in the past two decades! Keep in mind, it takes a +100% gain to recover a -50% decline.

5) 80% of individual traders lose money over ANY 10-year period. Why? Investor psychology, emotional biases, lack of capital, etc. Repeated studies by Dalbar prove this over and over again.

6) Raising cash is often a better hedge than shorting. While shorting the market, or a position, to hedge risk in a portfolio is reasonable, it also simply transfers the “risk of being wrong” from one side of the ledge to the other. Cash protects capital. Period. When a new trend, either bullish or bearish, is evident then appropriate investments can be made. In a “bull trend” you should only be neutral or long and in a “bear trend” only neutral or short. When the trend is not evident – cash is the best solution.

7) You can’t “buy low” if you don’t have anything to “buy with.” While the media chastises individuals for holding cash, it should be somewhat evident that by not “selling rich” you do not have the capital with which to “buy cheap.”

8) Cash protects against forced liquidations. One of the biggest problems for Americans currently, according to repeated surveys, is a lack of cash to meet emergencies. Having a cash cushion allows for working with life’s nasty little curves it throws at us from time to time without being forced to liquidate investments at the most inopportune times. Layoffs, employment changes, etc. which are economically driven tend to occur with downturns which coincide with market losses. Having cash allows you to weather the storms.

Importantly, I am not talking about being 100% in cash. I am suggesting that holding higher levels of cash during periods of uncertainty provides both stability and opportunity.

With the fundamental and economic backdrop becoming much more hostile toward investors in the intermediate term, understanding the value of cash as a “hedge” against loss becomes much more important.

As John Hussman noted in one of his past missives:

“The overall economic and financial landscape, then, is one where obscene valuations imply zero or negative S&P 500 total returns for more than a decade — an outcome that is largely baked-in-the-cake regardless of shorter term economic or speculative factors. Presently, market internals remain unfavorable as well. Coming off of recent overvalued, overbought, overbullish extremes, this has historically opened a clear vulnerability of the market to air-pockets, free-falls and crashes.”

As stated above, near zero returns do not imply that each year will have a zero rate of return. However, as a quick review of the past 15 years shows, markets can trade in very wide ranges leaving those who “rode it out” little to show for their emotional wear.

Given the length of the current market advance, deteriorating internals, high valuations, and weak economic backdrop; reviewing cash as an asset class in your allocation may make some sense. Chasing yield at any cost has typically not ended well for most.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is another reason they are so adamant that you remain invested all the time.