Authored by Richard Rosso via RealInvestmentAdvice.com,

“The emergence of money manager capitalism means that the financing of the capital development of the economy has taken a back seat to the quest for short-run total returns.” – Circa 1992.

Wall Street has forgotten the great financial crisis.

A sense of relief has settled firmly on the legendary asphalt artery between Trinity and the FDR Drive.

Looks like they got away with another one.

Nobody else will, so let me say it (at least mean it): Thank you, Mr. & Mrs. Taxpayer.

Again. Sincerely. Thank you. Now, let’s get on with blowing your wealth out of the water again, just as portfolios have made it back to even. Older, a bit pudgier, more forehead than before.

Oh wait, that’s me.

As the Great Recession gets pulled into the mist, obfuscated by the misleading but comforting math of market return averages and a bull that has rarely stumbled, Wall Street is more defiant than ever to broadcast:

“See? We told you so! The markets always rebound in time!”

Time. That precious commodity you’d pay more than you’re worth, for.

The concept of time holds little relevance to Wall Street. After all, its life expectancy may be considered perpetual. Eight years, seventeen years, whatever time it takes to recover from a poor cycle is irrelevant and may be celebrated. A human life is different. We die. We can’t be so flippant over lost time.

You know all too well about how painful it is to recover from losses.

Understandable why it makes sense that Main Street, or why Americans vividly recall the Great Recession. They’re older and unless in the top 1%, not much richer. They’re also skeptical of the so-called economic recovery as inflation-adjusted median incomes have remained stagnant for close to a decade. Read: The Illusion of Declining Debt-To-Income Ratios.

Sentier Research an organization that focuses on income and demographics publishes monthly updates on household incomes. Their numbers tend to be direr than Lance Roberts’ on the topic. According to Sentier, May 2017’s median household income is roughly 1% above the median of $58,711 set back in January 2000.

The reason I rehash painful memories and current reality, is to conjure a name we haven’t heard since 2007. It’s an attempt to ground myself. Ground you, too.

Meanwhile in the fantasy-land horror ride otherwise known as a central banker’s noggin…

It feels opportune for me; as I write, the head of the Federal Reserve Janet Yellen at a recent event in London, espoused just what the media wanted to hear. Get this: She’s confident that a run on the banking system won’t happen “as long as she lives.” Read: Yes, Ms. Yellen…. There Will Be Another Financial Crisis.

You see, Ms. Yellen’s frame of reference, that of Neoclassical economic texts studied within hallowed walls – where financial crisis, or any shock, with the word “GREAT” attached to it like Depression or Recession, are dismissed as anomalies. Her accepted theories explain away the power of the shadow banking system to take the so-called regulated financial system down with it.

In her naïve corner of economic study, alleged exogenous events are minimized as episodes that may occur, give or take, every 4,000 years. Unfortunately, the result is an unwarranted sense of complacency that ironically, leads to instability the rest of society ultimately pays for.

How else can a Fed chair whose words are taken so seriously expound in public that another financial crisis was not likely in our lifetime? In my lifetime, we’ve experienced multiple so-called outlier events. Unless she’s planning to check out soon, I’m not sure how confident Yellen can be in her statement.

One fact is obvious; the Fed has put to bed that whole financial crisis thing, too.

A reason that justifies the resurrection of this economist’s theories.

You may have missed references to him a decade ago; it’s opportune to revive all the man stood for as iconoclastic economist Hyman P. Minsky in his body of work, was an advocate for Main Street. Not Wall Street.

Explains why he’s rarely discussed these days. Perhaps his name is whispered throughout hallowed academic halls where nobody on Wall Street or yearning to be employed by the Street, can hear.

If anything, I’m regrettably assured his theories are relegated to a brief paragraph in widely-read university economic textbooks under “harebrained theories” or “economists who suffer unjustified paranoia.”

What I am confident of is many professionals in the financial industry and big box financial pundit puppets who publish irresponsible forecasts are thankful Minsky’s framework on risk expansion and subsequent collapse, has vanished from purview.

Now, in the midst of a market cycle of low hum – sluggish growth, benign interest rates, flat-lined volatility, and a period of robust animal spirits, I’m beginning to feel his presence emerge from the calm, once again. At least in my head.

After a decade of complacency as the world remains awash in central bank liquidity, Dr. Minsky and his financial instability hypothesis have faded to distant memory. In 2007, Paul McCulley then Managing Director of behemoth money management firm PIMCO, coined a genius term Minsky Moment to eloquently describe the domino effect of irresponsible risk expansion followed by financial system disruption sparked by a collapse of reckless debt, in this case subprime mortgage liabilities.

Minsky understood how rational profit-seeking activities always held potential over time, especially through calm or boom periods, to ostensibly morph into speculative Ponzi-type activities. The longer the macro-environment allowed such behavior void of repercussion, the greater the spread of the most dangerous of risks.

Unlike neoclassical economists’ belief in the core doctrine that market forces are naturally stabilizing, Minsky’s view was that market forces, human behaviors, were far from efficient or rational. Boom or stable cycles eventually culminated in destabilizing outcomes.

The longer the riskier behavior persisted without repercussion, the greater the imminent collapse. In other words, he believed in ebb and flow or cycles. Shocking. I know.

He outlined three financing tiers that progressed from hedged (where income flows adequately cover all interest and principal payments), to speculative where interest payments are met, but not principal, to the final most dangerous stage – Ponzi, where receipts are insufficient to cover even interest payments. The hope is at this stage, that underlying assets will appreciate sufficiently to cover liabilities.

The subprime mortgage crisis was indeed a Ponzi where the infective narrative “house values always appreciate,” allowed for irresponsible risk taking. Once foreclosures started to climb, or the spark ignited to disprove the housing appreciation story, the entire system we falsely trusted, began to falter.

The cancer of risk collapse spread rapidly through the arteries of the shadow financial underbelly of the economy and surfaced to affect every industry housing touched. The so-called regulated financial system was not spared damage either with the collapse of tenured institutions like Lehman Brothers.

Since the crisis, there have been multiple short-term regulatory patches put in place to fortify the financial industry. For the most part, these regulations are the same inadequate hammers for larger, stronger nails.

As he was a proponent of a pliable system of reform which could be altered based on the innovative risk humans create, Minsky would have been disappointed to know that the interconnected global shadow banking web continues to expand, Federal Reserve policies have created a great misallocation of financial resources, price discovery of risk assets is basically non-existent and the segment of the population or Main Street that was a concern for him, suffers great wealth inequality and wage disparity.

Several catalysts exist today that may remind investors of Minsky. Readers should remain vigilant and keep the following concerns in mind as they invest and manage their personal wealth.

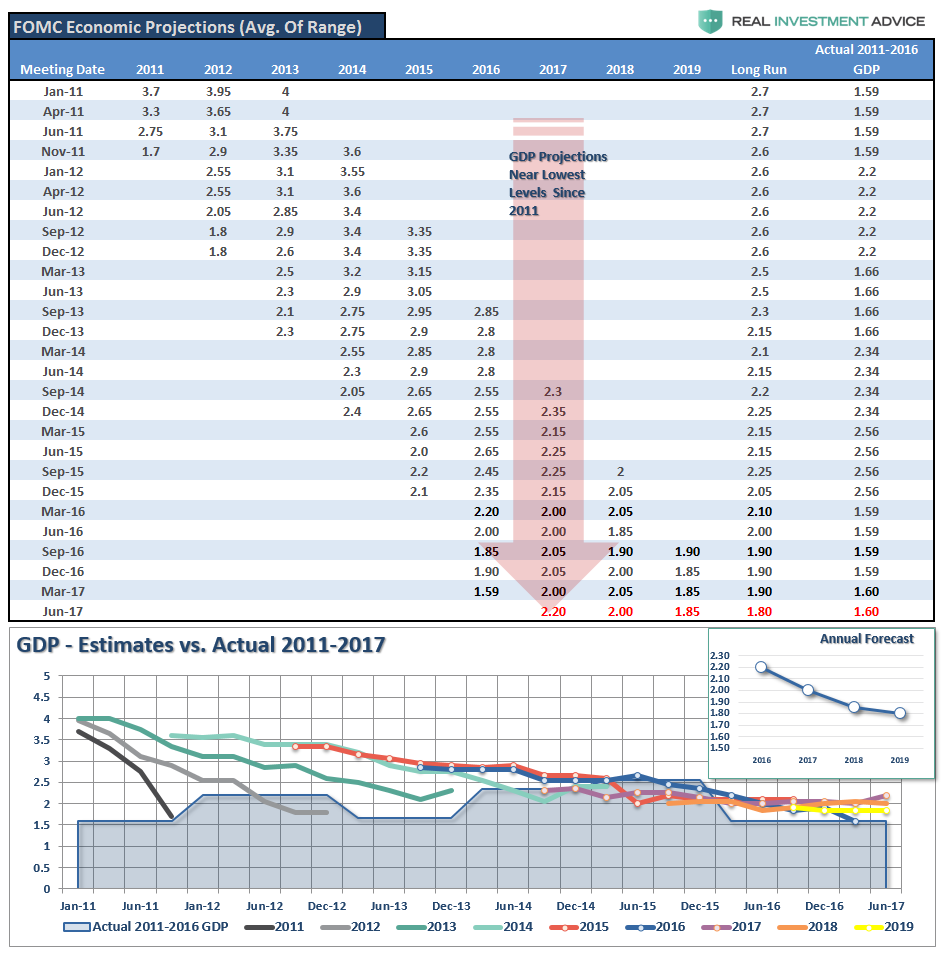

The Federal Reserve has appeared to gravitate from data dependent to data ignorant.

Economic data remains sub-par. Inflation has fallen below the Fed’s target of two percent, yet they appear in their statements, determined to continue hiking short-term rates.

In theory, a rate-tightening cycle is designed to take the edge off, tap the brake on accelerating economic growth. So, with GDP running below the long-term average of three percent and the personal consumption expenditures or PCE Index, the Fed’s preferred measure of inflation slipping to 1.4% year-over-year in May, the lowest in six months, a question begs asking. Read: The Fed just got another big reminder of why it should stop raising interest rates.

Yellen, what are you putting a brake on?

Based on the analysis below, the Fed has no reason to continue rate hikes this year. However, they seem hell-bent to ignore the data. Why?

The Fed may be on an unofficial mission to curb stock market speculation. Several Fed officials including Vice-Chairman Stanley Fischer and San Francisco Fed President John Williams have voiced their concerns over lofty stock market valuations.

Regardless, of the Fed’s agenda to forge ahead with rate hikes, it’s crucial to remember that low interest rates have been the primary accelerant for stock market appreciation, not earnings growth; rising rates along the yield curve eventually puts a damper on the economy and sets up a prime catalyst for market correction. If the Fed moves too quickly or inflation heats up to warrant swifter action, then a Minsky Moment may be closer than pundits believe.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/05/Low-Rate-Justify-Valuations-051617.png[/image]

In a majority of instances, a period of rising rates is not conducive to higher stock prices.

The ethereal nature of confidence vs. the facts of hard data.

Facts inevitably win.

There’s been an undeniable jolt in economic optimism after the presidential election that has spilled over to stock prices. The challenge lies in combating the continued lackluster reality of actual economic performance. The U.S. economy still appears to be chugging along at roughly two percent. A sluggish pattern that hasn’t changed in years.

Eventually, the market will be compelled to narrow the chasm between hope for the future and current hard lines of reality. Either corporate earnings and GDP will exhibit a marked pickup in growth to validate market levels, or prices will moderate to meet the reality of the current environment.

History shows it’s not uncommon for markets to overcompensate, leap ahead, especially in the face of fiscal promises like tax cuts, deregulation and infrastructure spending, all which appear to be slow in progressing.

Nobody knows how much time the market is going to allow the President to fulfill his agenda. The deeper the divide between hope and reality becomes, the greater chance of Minsky to graduate to the forefront of hot buzzwords around the squawking circles of financial media.

The complacency of professionals, investors and big-box retail financial talking heads has finally arrived, but how long will it last?

Two recent episodes stand out for me.

It’s not all about numbers – I heed anecdotal evidence as contrarian, a qualitative indication of change in narrative. Unless you believe humans aren’t emotional and markets are rational, that is. It’s a nice sentiment to consider market forces as naturally stabilizing and motivated completely by math.

Minsky believed that market forces were exactly opposite. He considered the ‘real world’ unstable; markets had a tendency to keep stretching parameters of risk which required flexible, changing regulatory actions to keep the greater risks from spreading to Main Street.

In the awkward head tilt of conversations overheard on escalators and elevators, I discover jewels in the jabber. Through hundreds of e-mails we receive from readers and investors; from surveys that I don’t consider empirical but important, there are trends we detect.

There’s no doubt a sense of calm is reaching fever pitch. There is an air of stability which may breed instability (if I’m wearing my Minsky cap).

Dreyfus conducted a survey recently and discovered that 61 percent of investors 55+ indicated they have not or will not reevaluate their investment approach in today’s investment environment of low interest rates, low market volatility and uneven economic growth. Overall, six in ten investors without a financial advisor are most likely to put off their plans to address the current market environment.

Now, I’m not certain as to why investors, especially those closer to retirement, are so indifferent about this topic, however, I draw several conclusions.

Recency bias. Let’s face it. Novice investors and financial professionals have never witnessed a correction let alone a bear market. Nor is this sheltered group advised or taught to understand that market winds shift, cycles change. If the only thing you know (and it’s worked), is ‘buy the dips’ then every derail is a buying opportunity. Until it isn’t. Complacency feeds on this mentality.

Loss aversion. For those 55+ in the study who haven’t re-evaluated, it’s plausible they are mired in a Great Recession mindset. Possibly, these investors sold (probably close or at the 2009 bottom), never to return to an allocation they believe requires assessment, as it’s primarily in cash and fixed income. Regardless of the composition of an investment allocation, no matter how conservative, portfolios require periodic attention and re-adjustment.

Overconfidence. It’s possible that low volatility in markets and a massive shift from active to passive investments has blossomed overconfidence and complacency as the financial industry and the media continue to position passive as the latest, greatest panacea for every investment malady. Puzzlingly, investors link passive to safe; a misconception I address almost daily. There’s no such connection between the concepts of ‘safe’ and ‘stocks.’ None.

Last week we received an e-mail from a newsletter reader who indicated that his big-box financial partner explained that barring any geopolitical risk, the stock market would be higher by the end of the year. Bold statement to say the least.

I’m not certain how any financial professional has the crystal balls to know how the market is going to close out the year. I guess this advisor could be correct. Or maybe he or she is behind on a quarterly sales quota. Not sure.

This is only one example of communication we receive along a similar theme.

I know as we get closer to market tops or late stage cycles, I read and hear sloppy statements of overconfidence with increased frequency from financial professionals and occasionally, central bank leadership. Stories are created and spread to authenticate a continued march higher for stocks.

I’m not saying a Minsky Moment is right around the corner. In part, it’s too disconcerting for me to think about how global central banks, stretched to the outer limits of creative monetary theories, don’t have enough firepower to right the ship again. The deep-seeded dysfunction of fiscal authorities across the globe doesn’t make me feel warm and fuzzy, either.

However, resurrecting an alternative economic viewpoint at a time of heightened complacency seems the right thing to do. If anything, Minsky’s work may spark curiosity, discussion, and questions.

I hope to encourage readers and investors to consider his message, assess financial risk in their own households and adjust accordingly.