Authored by Lance Roberts via RealInvestmentAdvice.com,

Last week, I noted:

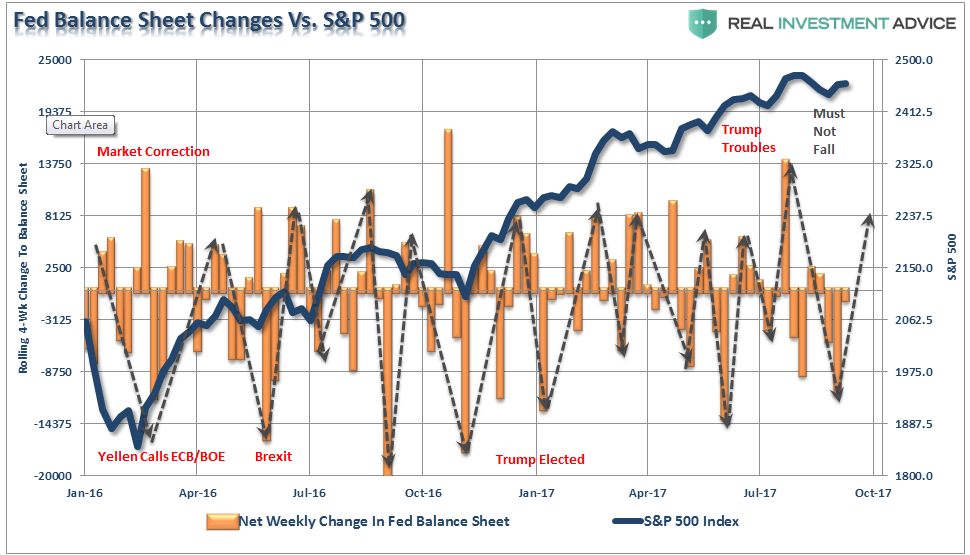

“I have a sneaky suspicion that when I update the Fed Balance Sheet reinvestment analysis next week, shown below, we are going to find a substantial, well-timed, reinvestment by the Central Bank. Wanna bet?”

Well, here is the updated chart of the 4-week net change to the Fed’s balance sheet. As you can see, reinvestments have, once again, returned to the market in a very “timely” fashion. Of course, since the Fed claims they are not trying to, nor are they influenced by, the markets, this is purely coincidental. (#SarcasmAlert)

The good news this week is that the market maintained last week’s advance despite the one-day tantrum earlier this week. Interestingly, since the election, the market has ratcheted higher in slightly more than 3% increments with each move higher followed by a drawn-out consolidation process that runs primarily along the 50-75 dma. The last sell-off tested, and held, the 100-dma but stayed within the confines of the consolidation process. The 2400 level on the S&P 500 remains the clear “warning level” for investors currently.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/SP500-Chart1-090817.png[/image]

But this short-term bullish backdrop is offset by intermediate-term bearish underpinnings as shown by the next two charts. With an intermediate-term momentum sell-signal in place, combined with overbought conditions, continues to suggest further gains from this point will likely remain limited and more volatile to obtain. That statement DOES NOT preclude the markets reaching new highs, it just suggests that downside corrective risks outweigh the potential currently for further gains.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/SP500-Chart3-090817.png[/image]

The bigger concern continues to be the internal deterioration of the markets as the number of stocks on bullish “buy signals” and the number of stocks above their 200-dma continue to deteriorate. Again, this is more supportive of a continued correctionary process versus a reversal and strong push higher in asset prices.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/SP500-Internals-Chart2-090817.png[/image]

Importantly, as I will discuss momentarily, there are technical similarities suggesting we could be closer to the next major market reversal than not. While the markets are currently on a longer-term “buy signal,” as shown at the bottom of the chart below, the current signal is similar to what was seen in the run up to the peak of the “dot.com” bubble.

Notice that in 1998, the “buy signal” was reversed temporarily by a sharp sell-off in the market due to the collapse of “Long-Term Capital Management.” A test of the “bullish” trend held and the markets reversed as the “dot.com” bubble ensued. The next “sell signal” denoted the beginning of the market topping process and prices followed soon thereafter.

With a large deviation from the bullish trend, combined with a long-term signal at very high levels, the next reversal that violates the bullish trend will very likely signal the beginning of a more protracted bear market.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/SP500-Chart4-090817.png[/image]

The warning signs are stack up on a technical basis suggesting the “risk” is becoming more elevated. While the bullish trend remains intact, keeping portfolios allocated toward equity risk currently, we are more focused on rebalancing and hedging risk in portfolios currently.

We agree with Howard Marks who recently stated:

“It’s time for caution, not a full-scale exodus.“

Yet.

As for what to do right now, we are pursuing the same strategy he discusses in his latest missive:

“Thus I would mostly do the things I always have done and accept that returns will be lower than they traditionally have been. While doing the usual, I would increase the caution with which I do it, even at the cost of a reduction in expected return. And I would emphasize “alpha markets” where hard work and skill might add to returns, since there are no “beta markets” that offer generous returns today.

‘Move forward, but with caution.'”

Signs, Signs, Everywhere A Sign

You don’t have to look very hard to see a rising number of signs that suggest the “Trump Trade” has come to its inevitable conclusion.

Following the election, this past November the financial markets rallied sharply on the hopes of major policy reforms and legislative agenda coming out of Washington.

Eleven months later, the markets are still waiting as the Administration has remained primarily embroiled in Washington politics with a divisive, Republican controlled, House and Senate. While there are still “hopes” the Administration will pass through tax reform, the failure to “rally the troops” to repeal the Affordable Care Act leaves permanent tax cuts an unlikely outcome. That hopeful outcome was further exacerbated with the deal cut between President Trump and leading Democrats to lift the debt ceiling and fund the Government through December. That “deal” has effectively nullified any leverage the Republicans had to strong-arm a deal on taxes later this year.

The markets are figuring it out as well.

If you want to know where the economy is headed over the next few months, you don’t have to look much further than interest rates. Since interest rates are ultimately driven by the demand for credit, and that demand is driven by economic growth, their historical correlation is no surprise.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Rates-GDP-090817-2.png[/image]

But like I said, if you want to know where GDP is going to be in the months ahead, keep a close watch on rates. I suspect, before year-end, we will see rates below 2.0%.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Rates-GDP-090817.png[/image]

As a reminder, this is why we have remained rampant bond bulls since 2013 despite the continuing calls for the end of the “bond bull market.” The 3-D’s (Demographics, Deflation & Debt) ensure that rates will remain low, and go lower, in the years to come. Think Japan.

But I digress.

Like rates, inflation is also closely tied to the direction and trend of economic strength. While the Fed continues to hope for a return of inflationary pressures, the real strength of the underlying economy suggests something quite different.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Inflation-GDP-090817.png[/image]

Again, following the election inflationary pressures surged on “hopes” of the “second coming” of the economy. Those hopes are now fading, and economic growth along with it.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Inflation-GDP-090817-2.png[/image]

But there is no better sign to watch than that of the US Dollar. The dollar is the representation of the world’s belief in the strength of the U.S. economy. A stronger economy attracts capital and investment which drives the dollar higher and further boosts economic growth. The opposite also applies.

The recent decline in the dollar, which is likely to continue, suggests that economic growth will weaken in the months ahead.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/USD-GDP-090817.png[/image]

While it is not hard to see, or understand, the correlation between these individual “signs” and the direction of the economy, we can see it even more clearly by building a simple composite. The composite below is the dollar, interest rates, and inflation as compared to nominal GDP.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Economic-Composite-GDP-1-090917.png[/image]

Currently, the composite index has turned down rather sharply and we should expect economic growth, to track along with it in the coming months.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/09/Economic-Composite-GDP-2-090917.png[/image]

All of these signs are worth watching closely. A weaker economy leads to weaker earnings growth and estimates are already under rather severe downward pressure. Given the overvaluation of the market, and hopes of legislative agenda beginning to fade, there is a significant risk to outlooks for the market in the months ahead.

The last few times the dollar, rates, and inflation fell following a previous advance, the outcome for investors was not all that great.

However, as I said above, we are indeed moving forward, but with caution.

“Here’s your sign.” – Bill Engvall