Authored by Lance Roberts via RealInvestmentAdvice.com,

With the passage of the Tax Cut And Jobs Act on Wednesday, I wanted to address a few of the questions and misinformation currently circulating about the impact of tax cuts on the U.S. economy.

Over the last couple of months, I have been repeatedly asked why I am not “enthusiastic” about the “greatest tax reform” since the Reagan era.

First, let me be clear, I like getting a “tax cut.” Under the new plan, and because I own several small businesses structured as limited liability corporations (LLC’s), I will potentially see a reduction in the amount of taxes I will pay next year.

What I am opposed to, as a “fiscal conservative,” is the ongoing expansion of our debts and deficits which are an inherent drag on the future prosperity of the country.

For the last 8-years, Republicans have repeatedly blamed the previous Administration for doubling the national debt and further expanding dependency on the welfare and entitlement system. When the Republican-controlled Senate and House had the opportunity to live up to their promise of reducing spending and being more fiscally responsible, their first piece of major legislative action will add another $10 Trillion in debt over the next 10-years, increase the deficit to more than $1 Trillion, and double the size of an existing welfare program through increasing child tax credits.

As the Committee for a Responsible Federal Budget just wrote:

“This is the wrong legislation at the wrong time. Before the country enacted tax cuts in 2001, debt was at modest levels and we were forecasting nearly $6 trillion in budget surpluses over the following decade. Today, debt is at post-WWII record levels, and we’re on course to add $10 trillion to the debt over the next decade even before these tax cuts. Unquestionably, this legislation would make a bad fiscal situation worse. And it opens the door to further debt-financed legislation this year and in the future.

In combination with other year-end legislation, this tax bill could cause the return of trillion-dollar deficits as soon as next fiscal year; and it could lead debt to exceed the size of the economy within a decade. Meanwhile, it will leave us with little fiscal space to address future emergencies and priorities.

No one predicted that after the 2001 tax cuts we would have experienced the largest terrorist attack in our nation’s history, fought two wars, been hit by several major hurricanes, and ultimately fallen into a deep recession and financial crisis. Even if no similar events occur, our debt is rising unsustainably. Certainly, this tax cut makes us less equipped to deal with the next disaster, war, or recession.

I remain hopeful that this tax bill can help to improve economic growth. But likely the largest effects will be from a one-time economic sugar high; and when we come down from it, America will enter uncharted fiscal waters.”

But let’s look at some of the common “beliefs” about tax cuts and the subsequent economic realities.

Tax cuts will benefit the middle class and not the wealthy.

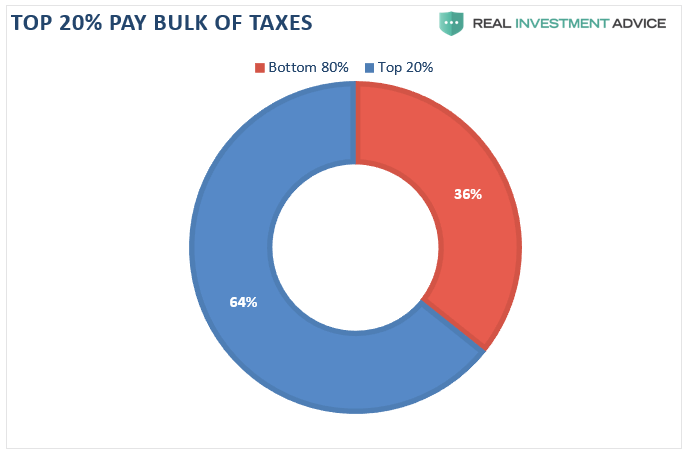

It is hard to make the argument the middle class will massively benefit from modest tax cuts when the bottom 80% of the population currently only pay

Furthermore, out of the total revenue collected by the government from income taxes, only 48.8% of that revenue comes from individual income taxes.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Taxes-FedRevenue-By-Source-050617.png[/image]

So, if tax cuts to the middle class are going to unleash a torrent of economic growth, the current tax reform act will do little to significantly increase the incomes of the bottom 80% of the population. As I noted previously:

“The picture gets worse when you look at just INDIVIDUAL tax liabilities. The bottom 80% currently pay only about 18% of individual taxes with top 20% paying the rest. Furthermore, the bottom 40% currently have a NEGATIVE tax liability, and with the new tax plan cutting many of the deductions currently available for those in the bottom 40%, it could be the difference between a tax refund and actually paying taxes.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/Tax-Liability-Individuals-Quintile-History-100317.png[/image]

“Of course, those in the top 20% of income earners are likely already consuming at a level with which they are satisfied. Therefore, a tax cut which delivers a few extra dollars to their bottom line, will likely have a negligible impact on their current levels of consumption.

The problem, as I have detailed previously, is that the vast majority of Americans are living paycheck to paycheck. According to CNN, almost six out of every ten Americans do not have enough money saved to even cover a $500 emergency expense.”

The reality is that a large number of American’s will experience little or no change to their current tax liability. As shown by the chart below from JP Morgan, the tax-cuts will primarily benefit the upper-middle income brackets and self-employed individuals. However, since the Affordable Care Act was not repealed, whatever savings are achieved through tax reform will likely be consumed by higher health care costs.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/TCJA-recipients.jpg[/image]

Tax cuts to corporations will lead to more jobs and higher wages.

This one is much more simple. The data clearly shows there is historically NO evidence that lower tax rates on the corporate side are passed through to individuals in the form of higher wages or more jobs.

The idea that companies will begin to increase employment is likely overestimated. With the long-run trend of employment growth declining, not to mention we are very late in the current economic cycle, tax cuts are unlikely to sharply increase employment rates.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/11/Taxes-Employment-110517.png[/image]

Importantly, despite record lows in unemployment, the job growth in the U.S. has not even kept up with the pace of population growth.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Employment-Population-Growth-110817.png[/image]

The same is true for the myth that tax cuts lead to higher wages. Again, as with economic growth, there is no evidence that cutting taxes increases wage growth for average Americans.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/11/Taxes-Wages-1105.png[/image]

More importantly, despite record levels of corporate profits, the following charts show you just how “generous” corporations have been with those massive coffers.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Wages-Profits-Ratio-112817.png[/image]

The one thing they have been very generous with is buying back outstanding shares to further boost bottom line EPS to offset weak revenue growth.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/SP500-ReportedEarnings-Buybacks-010317.png[/image]

Tax cuts will pay for themselves through stronger growth.

Unfortunately, again, there is no supportive evidence that lower tax rates, on either corporate or individual levels, have led to stronger economic growth over time. The chart compares the highest tax rate levels to 5-year average GDP growth. Since Reagan passed tax reform, average economic growth rates have only gone in one direction.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/10/Tax-Rates-GDP-Growth-5-YearAvg-110317.png[/image]

Furthermore, the fiscal “multiplier effect” of tax cuts is extremely small compared with other more important contributors to economic growth. In other words, the individuals, and households, who benefit the most from tax reform are also the ones with the lowest propensities to spend.

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/JPM-fiscal-multipliers.jpg[/image]

Summary

As I have been stating in several articles recently, those counting on massive, sustained economic growth to ensure the bill doesn’t add to the debt will very likely be disappointed. Not one credible analysis of the legislation shows the tax plan will pay for itself, or anywhere close to it. As the CFRB concluded:

“Most believe the bill will increase the growth rate by an average of 0.1 percentage points per year or less over the next decade, and that growth will fade as high levels of debt begin to hamper economic performance. So far, no estimate that accounts for the economic impact of higher debt has found the bill would raise the growth rate by more than 0.1 percentage points per year. Rather, estimates of the growth boost range from 0.03 to 0.09 points per year – not even a quarter of the 0.4-point target.

For example, the Penn Wharton Budget Model (PWBM) – which employs a model similar to those used by the Joint Committee on Taxation (JCT) – has found different versions of the TCJA would improve growth by between 0.03 and 0.09 percentage points per year. Likewise, the Tax Policy Center (TPC) estimates the House bill would increase average annual growth by 0.03 points over the budget window, largely due to a short-term increase in output that dissipates over time.”

[image]https://realinvestmentadvice.com/wp-content/uploads/2017/12/Impact-Of-Tax-Cuts.png[/image]

“Increasing growth by 0.4 percentage points on a sustained basis might sound doable, but such an increase actually means raising projected growth rates by more than one-fifth and is unlikely to occur because of tax reform alone.”

While well-designed tax reforms can certainly provide for better economic growth, those tax cuts must also be combined with responsible spending in Washington. That has yet to be the case as policy-makers continue to opt for “continuing resolutions” that grow expenditures by 8% per year rather than doing the hard work of passing a budget.

The growing demographic problem, combined with expanding dependence on social welfare programs, will ensure that “spending reform” remains vacant in Washington.

While policymakers had the opportunity to pass true, pro-growth, tax reform and show they were serious about our nations fiscal future, they instead opted to remain in deficit denial failing to stand up for future generations.